Working capital: what it is and how to calculate it

Learn what working capital is, how to calculate it, and practical ways to manage it for your small business.

Written by Lena Hanna—Trusted CPA Guidance on Accounting and Tax. Read Lena's full bio

Published Friday 15 May 2026

Table of contents

Key takeaways

- Working capital is the difference between your current assets and current liabilities. It shows whether your business has enough short-term resources to cover its obligations over the next 12 months.

- A positive working capital balance means you can pay your bills, handle unexpected costs, and invest in growth. A negative balance signals potential cash problems that need attention.

- Calculating your working capital ratio (current assets divided by current liabilities) gives you a quick snapshot of financial health. Most small businesses should aim for a ratio between 1.2 and 2.0.

- You can improve working capital by managing inventory, speeding up customer payments, controlling expenses, and using accounting software to track your finances in real time.

What is working capital?

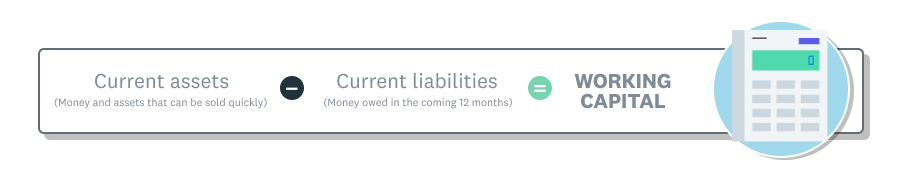

Working capital measures your business's short-term financial health. It's the money left over after subtracting what you owe (current liabilities) from what you own (current assets) over the next 12 months.

A positive number means your business can cover day-to-day expenses and still have room to grow. If your working capital is positive, you're in a strong position. If it's negative, it's time to look at where your money is going.

Current assets and liabilities

Current assets are resources your business owns that you can convert to cash within 12 months. Common examples include:

- Cash and bank account balances

- Accounts receivable (money customers owe you)

- Inventory and stock

- Prepaid expenses such as rent or insurance

- Short-term investments

Current liabilities are debts and obligations you need to pay within 12 months. These typically include:

- Accounts payable (money you owe suppliers)

- Short-term loans or lines of credit

- Taxes owed

- Wages and salaries due

- Accrued expenses

How to calculate working capital

The working capital formula is straightforward and uses numbers you can find on your balance sheet.

Working capital = current assets − current liabilities

If the result is positive, your business has more short-term resources than obligations. A negative result means your liabilities exceed your assets, which could signal cash flow trouble ahead.

A working capital formula example

Here's how a small florist shop might calculate working capital.

Say the shop has $100,000 in current assets, including cash, inventory, and accounts receivable. Its current liabilities, such as supplier invoices and a short-term loan, total $75,000.

$100,000 − $75,000 = $25,000

That $25,000 in working capital means the florist has a comfortable buffer to cover everyday expenses and handle any surprises.

Working capital vs working capital ratio

While working capital gives you a dollar amount, the working capital ratio (also called the current ratio) shows the relationship between your assets and liabilities as a proportion.

Working capital ratio = current assets ÷ current liabilities

Using the florist example above: $100,000 ÷ $75,000 = 1.33. A ratio above 1.0 means you have more assets than liabilities. Most lenders and financial advisors consider a ratio between 1.2 and 2.0 healthy for small businesses.

A ratio below 1.0 suggests your business may struggle to meet short-term obligations. A very high ratio (above 2.0) could mean you're not putting your assets to work efficiently.

The importance of working capital in business

Working capital affects nearly every part of how your business operates day to day. Here's why keeping it healthy matters.

- Operational stability: positive working capital means you can pay suppliers, cover payroll, and keep the lights on without scrambling for cash

- Market resilience: a financial cushion helps you weather slow seasons, economic downturns, or unexpected costs

- Growth potential: extra working capital gives you room to invest in new products, hire staff, or take on bigger projects

- Lender confidence: banks and investors look at working capital when deciding whether to approve loans or extend credit

Positive vs negative working capital

Positive working capital means your current assets exceed your current liabilities. It signals that your business can comfortably meet its short-term financial commitments while keeping cash available for opportunities.

Negative working capital means you owe more than you currently have on hand. While some industries (like grocery stores with fast inventory turnover) can operate this way temporarily, it's generally a warning sign for small businesses. It can lead to late payments, damaged supplier relationships, and difficulty covering payroll.

Working capital examples in different businesses

Working capital needs vary depending on your industry. The amount you need to keep your business running smoothly depends on factors like payment cycles, inventory requirements, and project timelines.

Working capital in construction and manufacturing

Construction and manufacturing businesses often need significant working capital because they buy materials and pay workers long before they receive payment for finished work.

For example, a construction company might have $600,000 in current assets (including materials, receivables, and cash) and $300,000 in current liabilities. That gives them $300,000 in working capital to bridge the gap between project expenses and client payments.

Working capital in service businesses

Service businesses like consulting firms, marketing agencies, and accounting practices typically carry less inventory. Their main working capital concerns are accounts receivable and managing the gap between delivering services and getting paid.

For service businesses, working capital often comes down to how quickly clients pay their invoices. Slow-paying clients can tie up cash and create short-term shortfalls even when the business is profitable.

Working capital in retail

Retail businesses need working capital to stock shelves and manage seasonal demand. A clothing store, for example, might invest heavily in inventory before the holiday season and rely on strong working capital to cover costs until sales pick up.

Retailers with fast inventory turnover can sometimes operate with lower working capital because products sell quickly and generate cash. However, managing the balance between too much and too little stock is critical.

What is net working capital?

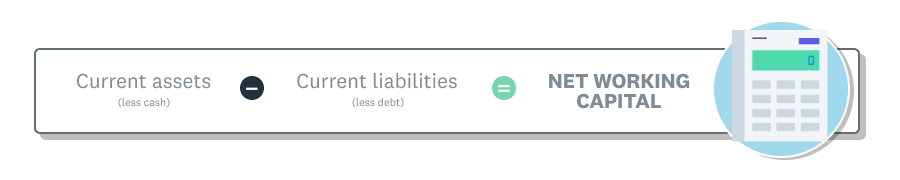

Net working capital is closely related to standard working capital, and the two terms are often used interchangeably. In practice, net working capital typically excludes cash and debt from the calculation, focusing on operating assets and liabilities only.

This narrower view helps you understand how efficiently your business operations generate and use short-term resources, without being affected by financing decisions or cash reserves.

The net working capital formula

Here's a simplified net working capital calculation using the florist example again.

Suppose the florist has $80,000 in operating current assets (accounts receivable, inventory, and prepaid expenses) and $65,000 in operating current liabilities (accounts payable and accrued expenses).

$80,000 − $65,000 = $15,000

That $15,000 in net working capital reflects the cash tied up in the florist's everyday operations, separate from any bank balances or loan repayments.

Working capital vs cash flow: what's the difference?

Working capital and cash flow are related but tell you different things about your finances. Understanding both gives you a more complete picture of your business's financial position.

Working capital is a snapshot at a single point in time. It tells you whether your current assets can cover your current liabilities right now. Cash flow, on the other hand, tracks the movement of money in and out of your business over a period of time.

You can have positive working capital but still face cash flow problems if your money is tied up in unpaid invoices or unsold inventory. Similarly, a business with tight working capital might have strong cash flow because money moves through quickly.

Using a short-term cash flow projection alongside your working capital figures can help you spot potential shortfalls before they become problems. Xero's cash flow tools let you see what's coming in and going out so you can plan ahead.

Working capital challenges and limitations

While working capital is a useful measure of financial health, it has some limitations you should keep in mind. Understanding these challenges helps you make better decisions about your finances.

- Changing asset values: inventory and receivables can fluctuate in value. Stock might become outdated or unsellable, and the working capital figure won't reflect that until you write it down.

- Timing issues: working capital is a snapshot, so it might look healthy on one day and tight the next. Seasonal businesses often see big swings depending on the time of year.

- Collection delays: accounts receivable shows up as an asset, but if customers are slow to pay, that money isn't actually available to cover your expenses.

- External disruptions: economic downturns, supply chain problems, or sudden changes in your market can shift your working capital position quickly and unpredictably.

- Forecasting difficulties: predicting future working capital needs is challenging for small businesses, especially when revenue is inconsistent or expenses are hard to predict.

- Inventory management: carrying too much stock ties up cash unnecessarily, while carrying too little can mean missed sales. Getting the balance right takes careful planning.

How to manage your working capital

Good working capital management means keeping enough cash available to run your business while putting your resources to work effectively. Here are practical steps you can take to stay on top of it.

Manage your inventory

Excess inventory ties up cash that could be used elsewhere in your business. Review your stock levels regularly and focus on keeping only what sells. Use data from your sales history to forecast demand and avoid over-ordering.

Check out the Xero guide on inventory management for more tips on getting your stock levels right. You can also use Xero's inventory features to track stock in real time.

Control your expenses

Review your spending regularly to find areas where you can cut costs or negotiate better terms. Even small savings on recurring expenses add up over time. Look at subscriptions, supplier contracts, and operational costs for opportunities.

For a deeper look at tracking and reducing costs, read the Xero guide on how to track business expenses.

Monitor your cash flow

Keep a close eye on the money coming in and going out of your business. Set up regular cash flow reviews so you can spot problems early and adjust your spending or collections strategy. Even profitable businesses can run into trouble if cash isn't arriving when it's needed.

Xero's guides on cash flow projection and managing finances and cash flow can help you build a system that works.

Invest in software tools to streamline your operations

Accounting software can save you time and give you a clearer view of your financial position. With real-time data on your income, expenses, and outstanding invoices, you can make faster, more informed decisions about your working capital.

Xero connects to your bank, automates invoicing, and generates financial reports that show exactly where your business stands. These features help you stay on top of your working capital without spending hours on manual data entry.

How financing can support working capital

Sometimes improving operations isn't enough to close a working capital gap, especially during periods of rapid growth or seasonal fluctuations. In those cases, external financing can help bridge the shortfall.

Before seeking financing, focus on improving your working capital through the operational strategies above. If you still need additional funds, here are some common options:

- Working capital loans: short-term loans designed to cover everyday business expenses. They're typically repaid within 12 months.

- Lines of credit: a flexible borrowing option that lets you draw funds as needed, up to a set limit. You only pay interest on what you use.

- Invoice financing: this lets you borrow against outstanding invoices so you can access cash before customers pay. It's useful when you have reliable clients who are slow to settle.

- Small Business Administration (SBA) resources: the SBA offers loan programs designed for small businesses. Visit sba.gov/funding-programs/loans to explore your options.

Financing should be a last resort after you've optimized your operations. Always consult a financial advisor before taking on new debt to make sure it's the right move for your situation.

Improve your working capital with Xero

Staying on top of your working capital is easier with the right tools. Xero's accounting software gives you a real-time view of your finances so you can make confident decisions about your business.

With Xero, you can:

- Track your cash position and outstanding invoices in near real time

- Automate invoicing and follow up on late payments

- Monitor expenses and spot trends before they become problems

- Generate financial reports that show your working capital at a glance

- Connect to your bank for automatic reconciliation

- Use short-term cash flow projections to plan ahead

FAQs on working capital

Here are answers to frequently asked questions about working capital.

What is working capital in simple words?

Working capital is the money your business has available to cover its short-term expenses. You calculate it by subtracting what you owe from what you own, using only assets and liabilities due within 12 months.

What are three examples of working capital?

Common examples of working capital components include cash in your bank account, money customers owe you (accounts receivable), and inventory you plan to sell. These are all current assets that contribute to your working capital when you subtract what you owe.

What is good working capital?

Good working capital means having enough current assets to comfortably cover your current liabilities while still leaving room for unexpected expenses or growth opportunities. The right amount varies by industry, but a positive balance is generally a healthy sign.

What is a good working capital ratio for small businesses?

Most financial advisors recommend a working capital ratio between 1.2 and 2.0 for small businesses. A ratio below 1.0 suggests you may have trouble paying short-term debts. A ratio above 2.0 might mean your assets aren't being used efficiently.

How can I improve my working capital ratio?

You can improve your working capital ratio by collecting payments from customers faster, reducing unnecessary inventory, negotiating longer payment terms with suppliers, and cutting non-essential expenses. Using accounting software to track these areas helps you stay proactive.

What happens if my working capital ratio is too low?

A low working capital ratio means you may not have enough resources to pay your bills on time. This can lead to late fees, damaged supplier relationships, and difficulty covering payroll. In serious cases, it could threaten your business's solvency.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Get one month free

Sign up to any Xero plan, and we will give you the first month free.