Small business financial management: a practical guide

Practical steps to manage your business finances, track cash flow, and grow profitably.

Written by Jotika Teli—Certified Public Accountant with 24 years of experience. Read Jotika's full bio

Published Friday 15 May 2026

Table of contents

Key takeaways

- Small business financial management means tracking income and expenses, planning ahead, and making informed decisions that keep your business healthy and growing.

- Separating personal and business finances protects you legally and makes tax time far simpler.

- Monitoring cash flow in real time and keeping 3 to 6 months of operating expenses in reserve can help you weather slow periods and unexpected costs.

- Setting aside 25 to 30% of net profit for taxes, plus 15.3% for self-employment tax if applicable, prevents surprises at tax time.

- Using accounting software to automate tracking, invoicing, and reporting saves time and gives you the visibility you need to make confident financial decisions.

What is small business financial management?

Small business financial management is the process of organizing, tracking, and planning your business's money so you can make smart decisions and stay profitable. It covers everything from monitoring daily income and expenses to long-term budgeting and forecasting.

Cash flow problems are one of the leading causes of small business failure. According to multiple studies, nearly 82% of businesses that fail cite cash flow issues as a contributing factor. Poor financial management, whether through a lack of planning, overspending, or failing to collect payments on time, puts even otherwise healthy businesses at risk.

Effective financial management involves several core activities:

- Tracking all income and expenses accurately

- Creating and maintaining a budget

- Forecasting future cash flow

- Reviewing financial statements regularly

- Planning for taxes and unexpected costs

Common pitfalls that derail small businesses include failing to plan beyond the next month, losing track of where money is going, not chasing overdue invoices, and setting revenue goals that aren't grounded in reality. The good news is that each of these problems is preventable with the right habits and tools in place.

Understand your financial statements

Financial statements are the foundation of informed decision-making. The two most important for day-to-day management are your balance sheet and your cash flow statement. Together, they tell you what your business is worth and whether you have enough cash to operate.

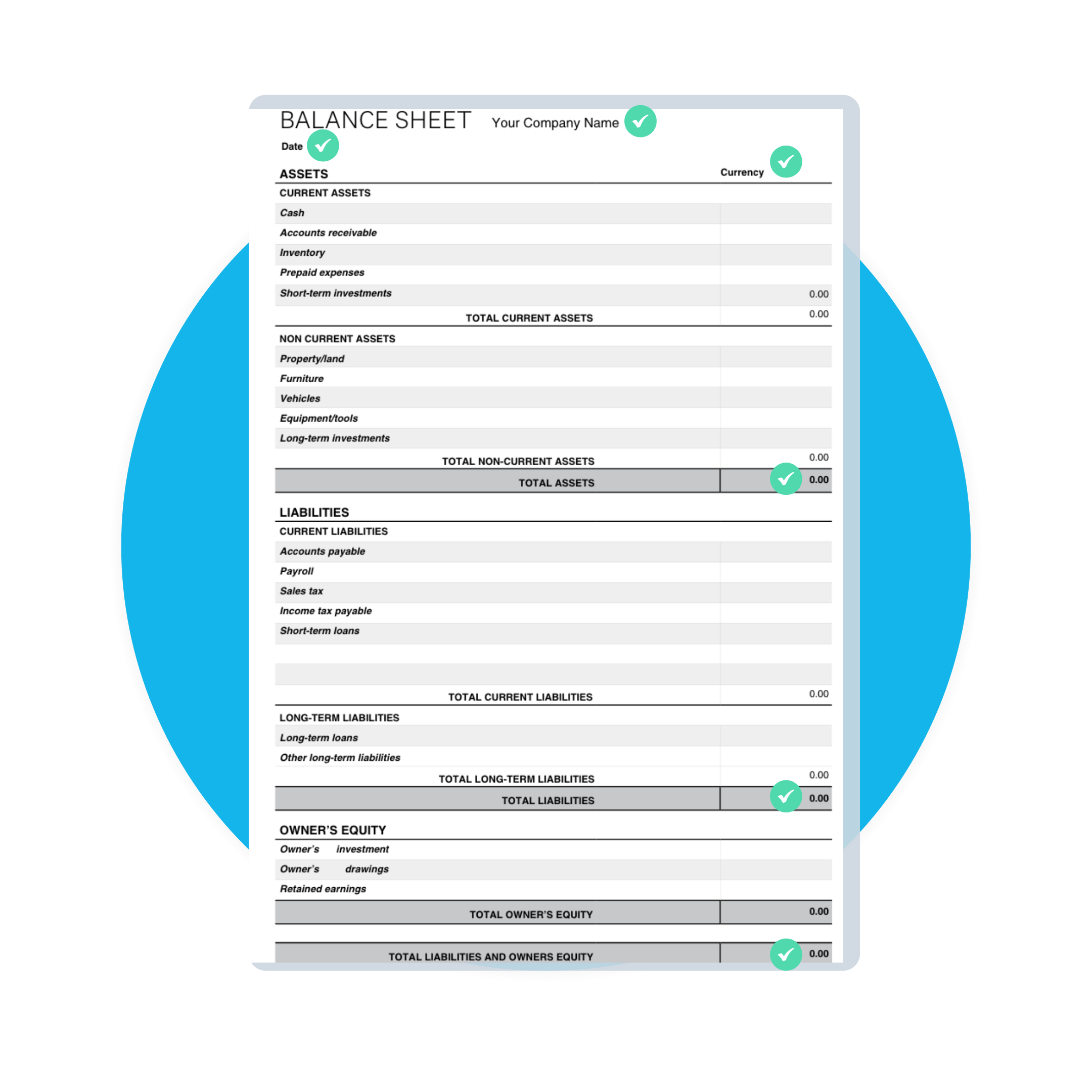

Understand balance sheet basics

A balance sheet gives you a snapshot of your business's financial position at a specific point in time. Think of it as a financial photograph that shows what you own, what you owe, and what's left over.

Every balance sheet has 3 components:

- Assets: everything your business owns that has value, including cash, equipment, inventory, and accounts receivable

- Liabilities: everything your business owes, such as loans, credit card balances, and accounts payable

- Owner's equity: the difference between your assets and liabilities, representing your ownership stake in the business

The fundamental formula is: Assets = Liabilities + Owner's Equity. This equation must always balance. If your total assets are $150,000 and your total liabilities are $90,000, your owner's equity is $60,000. This is closely tied to your working capital, which measures whether you have enough short-term assets to cover short-term liabilities.

Here's a simple example. Imagine your business has $50,000 in cash, $30,000 in equipment, and $20,000 in accounts receivable. That gives you $100,000 in total assets. You owe $25,000 on a business loan and $15,000 in accounts payable, totaling $40,000 in liabilities. Your owner's equity is $60,000.

Review your balance sheet at least monthly. It helps you spot trends, such as rising debt levels or shrinking equity, before they become serious problems.

Cash flow statement basics

A cash flow statement tracks all the money moving in and out of your business over a specific period, such as a month or a quarter. While your profit and loss (P&L) statement shows whether you're profitable on paper, your cash flow statement shows whether you actually have cash available to pay your bills.

This distinction matters because a business can be profitable and still run out of cash. If your customers take 60 days to pay but your suppliers require payment in 30 days, you could face a cash crunch even when sales are strong.

A cash flow statement is divided into 3 sections:

- Operating activities: cash generated or spent through your core business operations, including customer payments received and supplier payments made

- Investing activities: cash spent on or received from long-term assets, such as buying equipment, selling property, or making investments

- Financing activities: cash movements related to funding your business, including loan proceeds, loan repayments, and owner contributions or withdrawals

The key difference between a cash flow statement and a P&L is timing. Your P&L records revenue when it's earned and expenses when they're incurred, regardless of when cash changes hands. Your cash flow statement only records actual cash movements. Both reports are essential, but your cash flow statement gives you the clearest picture of whether you can cover your obligations right now.

Set up your business finances

Before you can manage your money effectively, you need the right financial foundation in place. That means choosing an accounting method, creating a budget, and separating your personal and business finances.

Create a business budget

A budget is your financial roadmap. It sets expectations for how much you'll earn and spend, and it gives you a benchmark to measure your actual performance against. Without one, it's easy to overspend in areas that don't drive growth.

Follow these steps to build a business budget:

- Calculate your total monthly income, including all revenue streams.

- List your fixed expenses, such as rent, insurance, loan payments, and subscriptions.

- List your variable expenses, including materials, utilities, marketing, and contractor fees.

- Set spending limits for each category based on your income and priorities.

- Review and adjust your budget monthly by comparing actual results to your plan.

One popular framework is the 70/20/10 budget rule. Under this approach, you allocate 70% of revenue to operating expenses, 20% to savings and debt repayment, and 10% to owner compensation and business growth. This ratio gives you a starting point; adjust it based on your industry and business stage.

For a detailed walkthrough on setting up your first budget, see Xero's guide to creating a small business budget.

Choose your accounting method

Your accounting method determines when you record income and expenses. The method you choose affects your tax obligations, financial reporting, and how you understand your business's financial health.

There are 2 main approaches:

- Cash basis accounting: you record income when you receive payment and expenses when you pay them. This method is simpler and gives you a clear view of the cash you actually have on hand. Most small businesses start here.

- Accrual basis accounting: you record income when it's earned and expenses when they're incurred, regardless of when money changes hands. This method provides a more accurate picture of profitability over time. It's required for businesses with more than $25 million in annual gross receipts.

Cash basis works well for service businesses, freelancers, and businesses with straightforward transactions. Accrual basis is better for businesses with inventory, long-term contracts, or complex billing cycles.

If you start with cash basis and decide to switch to accrual later, you'll need to file IRS Form 3115 to request approval for the change. Talk with your accountant before making that decision, as it affects how you report income and claim deductions.

Separate personal and business finances

Mixing personal and business money creates confusion at tax time and can put your personal assets at risk. Keeping your finances separate is one of the simplest ways to protect yourself and your business.

Here's why separation matters. If you operate as an LLC or corporation, mixing funds can lead to "piercing the corporate veil," where a court removes your limited liability protection. That means your personal savings, home, and other assets could be used to cover business debts.

Take these steps to keep things clean:

- Open a dedicated business bank account and run all business transactions through it

- Get a business credit card for business purchases only

- Pay yourself a regular salary or draw instead of dipping into business funds as needed

- Keep all receipts organized and categorized from day one

Separation also simplifies bookkeeping. When every transaction in your business account is a business transaction, reconciliation takes minutes instead of hours.

Pay yourself consistently

Paying yourself regularly isn't just good practice; it's essential for accurate financial planning. When you take money from the business inconsistently, it's harder to track profitability and budget effectively.

You have 3 main options for paying yourself:

- Salary: a fixed amount paid on a regular schedule, common for S-corp owners. You pay income tax and payroll taxes on this amount.

- Owner's draw: withdrawals from business profits, typical for sole proprietors and LLC members. You pay self-employment tax on net earnings.

- Combination: many S-corp owners take a reasonable salary plus periodic draws from remaining profits.

To set your compensation, review your business revenue, operating costs, and growth needs. Your pay should be sustainable without putting the business under financial strain.

If you're self-employed, you'll also owe self-employment tax on your net earnings. See the Plan for business taxes section below for the current rates and thresholds.

Use financial planning and forecasting

Financial planning helps you prepare for what's ahead instead of reacting to what's already happened. A solid forecast gives you the confidence to make spending decisions, hire new people, or invest in growth.

A useful starting point is the 50/30/20 revenue allocation model: 50% goes to cost of goods sold and direct expenses, 30% to overhead and operating costs, and 20% to profit and reserves. Discuss this breakdown with your accountant to tailor it to your specific industry.

Forecast at least 6 months ahead. This gives you enough runway to spot potential cash shortfalls and make adjustments before they become emergencies. Update your forecast monthly based on actual performance.

For more guidance, explore Xero's resources on cash flow projection and creating a small business budget.

Be ambitious but stay realistic

Growth requires ambition, but financial decisions need to be grounded in data. Setting stretch goals is healthy; betting the entire business on an optimistic assumption is not.

Balance your ambitions with rational analysis. Before committing to a major expense or expansion, pressure-test your assumptions. What happens if revenue comes in 20% below your forecast? Can you still cover your obligations?

Small mistakes are part of running a business. The key is to learn from them quickly and adjust your plans. Reviewing your forecast against actual results each month helps you spot where your assumptions went wrong so you can course-correct early.

Chart your cash flow

Visual cash flow charts make it easier to spot trends, patterns, and potential problems. Accounting software can generate these charts automatically from your transaction data.

When you review your cash flow chart, watch for these warning signs:

- Thin margins: if your cash flow line stays close to zero, you have very little room for unexpected expenses

- Negative dips: periods where outflows exceed inflows signal times when you may need to draw on reserves or a credit line

- Seasonal patterns: if your business has predictable slow periods, plan ahead by building reserves during peak months

Regular visual monitoring helps you move from reactive to proactive financial management.

Track and manage your cash flow in real time

Checking your cash flow once a month isn't enough for most businesses. Real-time cash flow management gives you an up-to-date view of your financial position so you can act quickly when conditions change.

Having cash reserves on hand protects you against slow-paying customers, seasonal dips, and unexpected costs like equipment repairs or economic downturns. For guidance on how much to set aside, see Build an emergency fund below.

When cash flow gets tight, consider these tactical adjustments:

- Negotiate longer payment terms with suppliers to delay outflows

- Shorten your invoice payment terms from 30 days to 14 days to accelerate inflows

- Reduce sitting inventory by running promotions or adjusting ordering quantities

- Establish a business line of credit before you need it, so it's available when cash gets tight

Modern accounting software enables real-time dashboards that pull in bank transactions, outstanding invoices, and upcoming bills automatically. Alerts can notify you when your cash balance drops below a threshold or when an invoice becomes overdue. Explore Xero's cash flow analytics tools to see how real-time visibility works in practice.

Manage your business debt

Not all debt is bad. Borrowing to fund equipment that generates revenue, or to bridge a seasonal cash gap, can be a smart move when the numbers work. The key is to borrow with a clear repayment plan.

Watch out for variable interest rates that can increase your costs unexpectedly. When rates rise, your monthly payments go up too, which can squeeze your cash flow.

Review your debts regularly with these steps:

- Compare the cost of each debt (interest rate and fees) to determine which to pay down first

- Assess whether your circumstances have changed since you took on the debt

- Shop around for refinancing options if you can get a lower rate

For a deeper look at debt strategy, see Xero's guide to managing business debt.

Review expenses regularly

Routine expense reviews help you catch unnecessary spending, identify cost-saving opportunities, and confirm your business is on track. Set a recurring time, whether weekly or monthly, to sit down with your numbers.

Focus on these key financial reports during your review:

- Profit and loss statement: shows revenue, expenses, and net income over a period

- Balance sheet: shows your financial position at a specific point in time

- Cash flow statement: tracks actual cash movements in and out of the business

- Accounts payable: shows what you owe to suppliers and vendors

- Accounts receivable: shows what customers owe you and how long invoices have been outstanding

- Depreciation schedule: tracks the declining value of your long-term assets

Review these reports with your accountant at least quarterly. They can help you spot trends and recommend adjustments. For more on reading financial statements, visit Xero's financial statement guide.

Plan for business taxes

Tax surprises are stressful and expensive. Planning ahead helps you avoid penalties and frees up cash for growth instead of scrambling to cover a tax bill.

As a general rule, set aside 25 to 30% of your net profit for federal and state income taxes. The exact percentage depends on your business structure, state tax rates, and total income.

If you're self-employed, add 15.3% for self-employment tax on net earnings of $400 or more. This covers Social Security (12.4%) and Medicare (2.9%). High earners pay an additional 0.9% Medicare surtax on income above $200,000 for single filers.

Stay ahead of your tax obligations by following these steps:

- Open a separate savings account specifically for tax payments.

- Transfer your estimated tax percentage into that account with every deposit or payment you receive.

- Make quarterly estimated tax payments to the IRS (due in April, June, September, and January) to avoid underpayment penalties.

- Track all deductible business expenses throughout the year, not just at tax time.

- Work with a CPA or tax professional to identify credits and deductions you may be missing.

For a comprehensive overview of tax preparation, see Xero's tax preparation guide.

Understand the true cost of money

Every dollar in your business has a cost associated with it, whether it's the interest on a loan, the fees on a credit card transaction, or the opportunity cost of tying up cash in inventory. Understanding these costs helps you make better financial decisions.

Consider these factors when evaluating how you spend and manage money:

- Pay bills on time: late payments often come with penalties and can damage your credit score, making future borrowing more expensive

- Evaluate payment methods: credit card processing fees typically range from 1.5 to 3.5% per transaction. Weigh this cost against the convenience and cash flow benefits of accepting cards.

- Compare buying versus leasing: purchasing equipment outright costs more upfront but may be cheaper long-term. Leasing preserves cash flow but typically costs more over the life of the asset.

- Learn tax and insurance rules: certain expenses are deductible, and some assets can be depreciated. Understanding these rules helps you minimize your tax burden legally.

- Be careful with bartering: the IRS considers bartered goods and services as taxable income. You must report the fair market value of what you receive.

Adjust your margins and get your pricing right

Your profit margin is the percentage of revenue left after covering costs. Getting your pricing right is one of the most impactful things you can do for your bottom line.

Markup pricing is a common approach: you add a percentage on top of your cost to set the selling price. For example, if a product costs you $50 and you apply a 60% markup, you sell it for $80.

Price elasticity is another concept worth understanding. It refers to how sensitive your customers are to price changes. If a small price increase causes a significant drop in sales, your product has high price elasticity. If customers keep buying regardless, demand is inelastic.

Test different price points with small customer segments before making broad changes. Even a small improvement in margin, applied across your entire product line, can significantly increase profit. For strategies to improve profitability, visit Xero's guide on how to increase profits.

Chase the money you're owed

Outstanding invoices are one of the biggest drains on small business cash flow. Money sitting in accounts receivable isn't money you can use to pay bills, buy inventory, or invest in growth.

Adopt these habits to keep receivables under control:

- Send invoices immediately after delivering goods or services

- Set clear payment terms upfront, ideally 14 to 30 days

- Track aging invoices and follow up consistently when payments are late

- Consider offering a small discount (such as 2%) for early payment

If you have chronically late-paying clients, invoice factoring is an option. A factoring company buys your unpaid invoices at a discount and collects the payment from your customer. You get cash immediately, though you'll receive less than the full invoice amount.

For more on getting paid faster, see Xero's tips on invoice payment terms.

Five questions to ask before bidding for big contracts

Landing a big contract can transform your business, but it also carries risk. Before you commit, evaluate the opportunity carefully to make sure it won't stretch your resources past the breaking point.

Ask yourself these 5 questions:

- Do you have the staff capacity? Can your current team handle the workload, or will you need to hire? Factor in recruitment time and costs.

- Can you fund the equipment and materials? Large contracts often require upfront investment. Make sure you have the cash or credit available.

- How will this affect your existing clients? If servicing the new contract means neglecting current customers, you could lose reliable revenue.

- What happens when the contract ends? A contract that represents 40% of your revenue creates significant risk if it isn't renewed.

- When will you get paid? Large clients often have long payment cycles. Confirm the payment schedule and make sure your cash flow can absorb the wait.

Diversified revenue is always safer than dependence on a single client. If no single customer accounts for more than 10 to 15% of your revenue, losing one won't threaten the business.

Know when to get accounting help

Handling your own books works when your business is small and transactions are simple. As things grow more complex, professional help can save you money and reduce stress.

Here are signs it's time to bring in an expert:

- Bookkeeping is taking time away from running your business

- Your business is growing and financial decisions are getting more complex

- You're confused about tax obligations or missing potential deductions

- Cash flow problems keep catching you off guard

- You're planning to seek funding, expand, or bring on partners

The type of help you need depends on your situation:

- Bookkeeper: handles day-to-day transaction recording, reconciliation, and basic reporting

- Accountant: provides financial analysis, helps with budgeting, and prepares financial statements

- CPA (Certified Public Accountant): handles tax preparation and planning, audits, and compliance

- Fractional CFO: provides part-time strategic financial leadership for businesses that aren't ready for a full-time CFO

For guidance on finding the right fit, see Xero's resources on small business accounting and when to hire an accountant.

Build an emergency fund

An emergency fund is your financial safety net. It protects your business when unexpected expenses hit, whether it's a broken piece of equipment, a sudden drop in sales, or an economic downturn.

Aim to save 3 to 6 months of operating expenses in a separate, easily accessible account. This gives you enough cushion to handle most disruptions without taking on debt or making panicked cost cuts.

If saving that amount feels overwhelming, start small. Set aside a fixed percentage of monthly revenue, even 5%, and build up gradually. The most important thing is consistency.

Here are a few tips to build your fund faster:

- Automate a monthly transfer from your business account to your emergency savings

- Direct any unexpected income, such as tax refunds or one-time client payments, into the fund

- Review your expenses for subscriptions or costs you can cut, and redirect those savings

Once you reach your target, keep contributing enough to maintain the balance as your operating costs grow.

Simplify your financial management with Xero

Strong financial management is the foundation of a successful small business. When you have clear visibility into your cash flow, expenses, and profitability, you can make decisions with confidence instead of guesswork.

Xero gives you real-time visibility into your finances so you can make confident decisions. From automated bank reconciliation to cash flow forecasting, invoicing, and expense tracking, Xero's online accounting software brings everything together in one place.

Ready to take control of your finances? Get one month free and see the difference real-time financial insights can make. You can also see all features to explore everything Xero offers.

FAQs on small business financial management

Here are answers to frequently asked questions about small business financial management.

What is a cash flow statement and what information does it provide?

A cash flow statement tracks the actual cash moving in and out of your business over a set period. It's divided into 3 sections: operating activities (core business cash flow), investing activities (long-term asset purchases and sales), and financing activities (loans, repayments, and owner contributions). It shows whether you have enough cash on hand to pay your bills, even if your P&L shows a profit.

What's the difference between cash and accrual accounting?

Cash basis accounting records income when you receive payment and expenses when you pay them. Accrual basis records income when it's earned and expenses when they're incurred, regardless of when cash changes hands. Most small businesses start with cash basis because it's simpler. Accrual is required for businesses with over $25 million in annual gross receipts.

How much should I set aside for business taxes?

Set aside 25 to 30% of your net profit for federal and state income taxes. If you're self-employed, add 15.3% for self-employment tax (12.4% Social Security plus 2.9% Medicare) on net earnings above $400. Make quarterly estimated payments to the IRS to avoid underpayment penalties.

Do I really need a separate bank account for my business?

Yes. A separate business bank account simplifies bookkeeping, makes tax preparation easier, and provides legal protection. If you operate as an LLC or corporation, commingling personal and business funds can pierce the corporate veil, removing your limited liability protection. It's one of the first things you should set up.

When should I hire an accountant or bookkeeper?

Consider hiring help when bookkeeping takes too much time away from running your business, when your finances are growing more complex, or when you're unsure about tax obligations. A bookkeeper handles daily transaction recording. An accountant or CPA provides financial analysis, tax planning, and strategic advice.

What is the 70/20/10 budget rule for businesses?

The 70/20/10 rule is a budgeting framework that allocates 70% of revenue to operating expenses, 20% to savings and debt repayment, and 10% to owner compensation and business growth. It's a starting point you can adjust based on your industry, business stage, and financial goals.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Get one month free

Sign up to any Xero plan, and we will give you the first month free.