What is accrual accounting? How it works, types, and examples

Learn how accrual accounting works, when to use it, and how it helps your small business track finances accurately.

Published Thursday 23 July 2026

Table of contents

Key takeaways

- Record revenue when you earn it and expenses when you incur them, not when cash changes hands, to get a more accurate picture of your business's true financial performance.

- Consider switching to accrual accounting if you're seeking investors or loans, selling products with inventory, or planning to grow your business beyond simple freelance work.

- Accrued revenue (money earned but not yet received) shows as an asset on your balance sheet, while accrued expenses (costs incurred but not yet paid) appear as liabilities.

- Use accounting software to automate the complexity of tracking receivables and payables, making accrual accounting manageable without hiring additional help.

What is accrual accounting?

Accrual accounting is a method where you record revenue when it's earned and expenses when they're incurred, regardless of when cash changes hands. It's the standard accounting method under both GAAP (Generally Accepted Accounting Principles) and IFRS (International Financial Reporting Standards), and it gives you a more accurate view of your business's financial health over time.

Accrual accounting requires more effort than cash accounting, but it offers important advantages:

- Accuracy: Provides a more complete long-term view of your finances

- Credibility: Many investors and lenders prefer working with businesses that use accrual accounting

- Compliance: Tax authorities may require certain business types and sizes to use this method

Accrual accounting keeps tabs on bills and sales invoices that are yet to be paid.

Accrual accounting keeps tabs on bills and sales invoices that are yet to be paid, so you always know where your money stands.

How accrual accounting works

Accrual accounting relies on 2 core principles that determine when you record income and costs in your books.

The matching principle

The matching principle requires you to record revenue in the same period as its related expenses. For example, accounting standards provide specific guidance on recognizing the incremental costs of obtaining a contract, which helps give a clearer picture of profitability.

Revenue recognition

Revenue recognition determines exactly when income appears in your records. You record income when you complete the work or deliver the product; official accounting standards state that revenue is recognized when an entity satisfies a performance obligation. Expenses follow the same logic: record costs when you receive goods or services, not when you pay the bill.

A practical example

You finish a consulting project in December but don't receive payment until January. With accrual accounting, you record the revenue in December because that's when you earned it. This shows your true December performance, even though the cash arrives later.

Types of accruals

There are 4 main types of accruals in accounting. Understanding each one helps you record transactions at the right time and keep your financial statements accurate.

Accrued revenue

Accrued revenue is income you've earned but haven't yet received payment for. This happens when you complete work before the customer pays.

For example, you run a software subscription service and bill customers quarterly. On March 31, you've provided 2 months of service but won't invoice until April 30. With accrual accounting, you record the revenue for those 2 months in March when you earned it, not April when you send the invoice.

Accrued expenses

Accrued expenses are costs you've incurred but haven't yet paid. This happens when you receive goods or services before the bill comes due.

For example, your employees work the last week of December, but you don't pay them until January 5. With accrual accounting, you record the wage expense in December when employees did the work, not January when you cut the checks.

Deferred revenue

Deferred revenue is money you've received from a customer before you've delivered the product or service. It appears as a liability on your balance sheet until you fulfill the obligation.

For example, a customer pays you $12,000 upfront for a 12-month service contract. You can't record the full amount as revenue right away. Instead, you recognize $1,000 each month as you deliver the service.

Prepaid expenses

Prepaid expenses are costs you've paid in advance for goods or services you haven't yet received or used. They appear as assets on your balance sheet until you consume them.

For example, you pay $6,000 in January for 6 months of office rent. Rather than recording the full amount as an expense in January, you recognize $1,000 each month as you use the space.

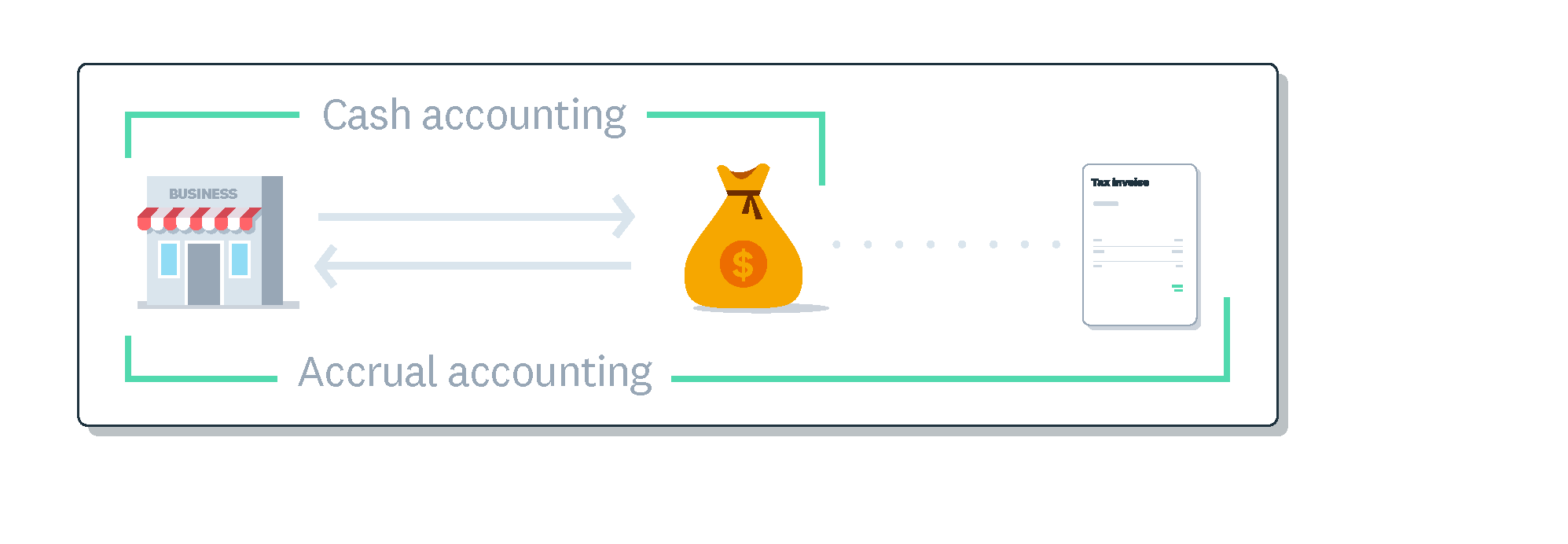

Accrual accounting vs cash accounting

The main difference between the 2 methods is timing. Cash accounting records transactions when money moves. Accrual accounting records transactions when they're earned or incurred.

Here's how they compare across key areas:

When revenue is recorded:

- Cash basis: When you receive payment

- Accrual basis: When you earn the income (complete the work or deliver the product)

When expenses are recorded:

- Cash basis: When you pay the bill

- Accrual basis: When you incur the cost (receive goods or services)

Complexity level:

- Cash basis: Simpler to manage and understand

- Accrual basis: Requires more tracking but provides better financial insight

Best for:

- Cash basis: Freelancers, solopreneurs, and service businesses with simple finances

- Accrual basis: Businesses with inventory, those seeking investors, or companies required by tax law

Cash flow visibility:

- Cash basis: Shows exactly how much cash you have right now

- Accrual basis: Shows money owed to you and money you owe, but requires separate cash flow tracking

Advantages of accrual accounting

Accrual accounting provides a more complete view of your financial health than cash accounting. Here are the key benefits for small businesses:

- Shows accurate profitability: Matches revenue with related expenses so you see true profit margins for each period

- Improves cash flow forecasting: Tracks money owed to you (accounts receivable) and money you owe (accounts payable) in 1 place, improving your cash flow visibility

- Supports better planning: Reveals financial trends and patterns that help you make informed decisions

- Builds credibility: Demonstrates financial sophistication to investors, lenders, and potential buyers

- Simplifies tax preparation: Keeps records organized throughout the year, making tax time less stressful

- Prepares you for growth: Switching accounting methods later can be complicated, so starting with accrual accounting sets you up to scale

This visibility matters more than many business owners realize. According to Xero Small Business Insights, US small businesses waited an average of 27.9 days to be paid in Q4 2025, with invoices arriving 7.8 days past their due date. Accrual accounting captures these outstanding receivables as they occur, giving you a realistic picture of incoming cash rather than waiting until payments actually land.

Disadvantages of accrual accounting

Accrual accounting requires more effort than cash accounting. Before switching methods, consider these challenges:

- Adds complexity: Requires tracking receivables and payables. This complexity is acknowledged in accounting standards, which offer a practical expedient to simplify cases where payment is expected within a year of service

- Takes more time: Demands consistent bookkeeping to record transactions when they occur, not just when cash moves

- May require help: Many small business owners hire a bookkeeper or accountant to manage accrual accounting properly

- Obscures cash position: Shows money you've earned but haven't received, which can make your actual cash balance less obvious

- Needs regular attention: Requires ongoing maintenance to keep records accurate and up to date

Accounting software can reduce much of this complexity by automating calculations and tracking.

When to use accrual accounting

Not every business needs accrual accounting, but certain situations make it necessary or beneficial. Here's how to decide which method fits your business.

Accrual accounting is required if:

- Your business is structured as a C-corporation

- Your annual gross receipts exceed $32 million (averaged over 3 years)

- You maintain inventory and have gross receipts over $32 million

Accrual accounting is recommended if:

- You're seeking loans or investment and need professional financial statements

- You sell products and need to track inventory costs accurately

- You have significant accounts receivable or accounts payable

- You're planning to grow and want to avoid switching methods later

- You want a clearer picture of profitability beyond just cash flow

Cash accounting may work better if:

- You're a freelancer or solopreneur with simple finances

- You provide services and get paid quickly

- You want the simplest possible bookkeeping

- Your business is small with minimal receivables and payables

If you decide to switch from cash to accrual accounting, you'll typically need to make the change at the start of a new tax year and file IRS Form 3115. When in doubt, consult with an accountant who understands your business and industry.

Accrual accounting best practices

Following these best practices helps you get the most from accrual accounting and keep your records reliable.

1. Recognize revenue at the right time

Record revenue only when you've fulfilled your obligation to the customer, not when you send an invoice or receive a deposit. If you deliver services over time, recognize revenue proportionally as you complete each milestone.

2. Standardize your expense tracking

Create clear categories for your expenses and record them consistently in the period they occur. Set up a regular schedule for entering bills and receipts so nothing slips through the cracks.

3. Review your accounts regularly

Reconcile your accounts receivable and accounts payable at least monthly. This helps you catch errors early, follow up on overdue invoices, and keep your financial statements accurate.

4. Set up internal controls

Separate responsibilities where possible so the person creating invoices isn't the same person approving payments. Even small businesses benefit from basic checks and balances that reduce the risk of errors or fraud.

5. Use accounting software

Cloud-based accounting software automates much of the manual work involved in accrual accounting. It tracks receivables and payables as you go, generates reports on demand, and reduces the chance of human error.

Simplify your accrual accounting with Xero

Managing accrual accounting manually can be time-consuming, but the right software handles most of the complexity for you.

With automated accrual accounting, you can focus on running your business:

- Automatic tracking: Records receivables and payables as you create invoices and enter bills

- Flexible reporting: Switch between cash and accrual views with 1 click to see your finances either way

- Real-time visibility: See what customers owe you and what you owe vendors in 1 dashboard

- Bank reconciliation: Matches transactions automatically so your books stay accurate

- Easy collaboration: Share access with your accountant or bookkeeper without extra software

Whether you're using cash or accrual accounting, you get clear insight into your business finances with Xero. Get one month free and see how you can simplify your accounting.

FAQs on accrual accounting

Here are answers to frequently asked questions about accrual accounting for small businesses.

What is a simple example of an accrual?

You receive office supplies in March but don't pay the vendor until April. With accrual accounting, you record the expense in March when you received the supplies, matching the cost with the period you used them.

Are accruals an asset or liability?

Accrued revenue appears as an asset (under accounts receivable), while accrued expenses appear as a liability (under accounts payable). Lenders and investors often look at both figures to assess how effectively you manage cash conversion.

Is accrual accounting required by GAAP?

Yes. GAAP requires the accrual basis of accounting for businesses that issue financial statements to external parties, such as investors or lenders. Smaller businesses that don't issue external financial statements may still choose cash accounting for tax purposes if they meet IRS eligibility rules.

Do I need to use accrual accounting for my small business?

It depends on your business size and structure. C-corporations and businesses with annual gross receipts over $32 million (averaged over 3 years) must use accrual accounting; other businesses can choose the method that best fits their needs.

Can I switch from cash to accrual accounting?

Yes, but you'll typically need to make the change at the start of a new tax year and file IRS Form 3115. Accounting software like Xero supports both methods and makes the transition smoother.

Does Xero support accrual accounting?

Yes. Xero fully supports accrual accounting, automatically tracking receivables and payables as you create invoices and enter bills. You can also switch between cash and accrual reporting views with 1 click.

Handy resources

Advisor directory

You can search for experts in our advisor directory

How to do bookkeeping

Learn about data entry, bank rec, reporting and tax prep in our guide to doing bookkeeping.

Online accounting with Xero

Automate your accounting in the cloud

Disclaimer

This glossary is for small business owners. The definitions are written with their requirements in mind. More detailed definitions can be found in accounting textbooks or from an accounting professional. Xero does not provide accounting, tax, business or legal advice.