How to set financial goals for your small business

Set clear financial goals to grow revenue, manage cash flow, and build a profitable small business.

Written by Shaun Quarton—Accounting & Finance Content Writer and Growth Marketer. Read Shaun's full bio

Published Wednesday 10 June 2026

Table of contents

Key takeaways

- Financial goals are specific, measurable targets that guide your small business toward profitability and long-term stability. Without them, you're reacting to problems instead of building toward outcomes.

- The SMART framework turns vague ambitions into actionable plans by making each goal specific, measurable, achievable, relevant, and time-bound.

- Tracking your goals regularly with accounting software and financial dashboards helps you catch problems early, adjust your strategy, and stay on course throughout the year.

Why are financial goals so important?

Financial goals are specific, measurable targets you set for your business's money: how much revenue you want to earn, how much profit you want to keep, or how quickly you want to pay down debt. They turn your broader business vision into concrete numbers you can track and act on.

For small businesses, setting financial goals isn't optional. According to Xero Small Business Insights, US small business sales growth averaged just 2.4% year-over-year in 2025, well below the long-term average of 5.5%. In a slow-growth environment, you need a clear financial roadmap to make the most of every dollar coming in.

Financial goals also help you make better day-to-day decisions. When you know you're aiming to increase your profit margin by 5% this year, it's easier to evaluate whether a new hire, a marketing campaign, or an equipment purchase is worth the investment. Goals give you a filter for spending decisions that would otherwise feel like guesswork.

Without financial goals, it's easy to confuse being busy with being profitable. You might bring in more revenue each quarter but still struggle to cover expenses if you haven't set targets for margins or cash reserves. Goals keep you focused on the numbers that actually determine your business's health.

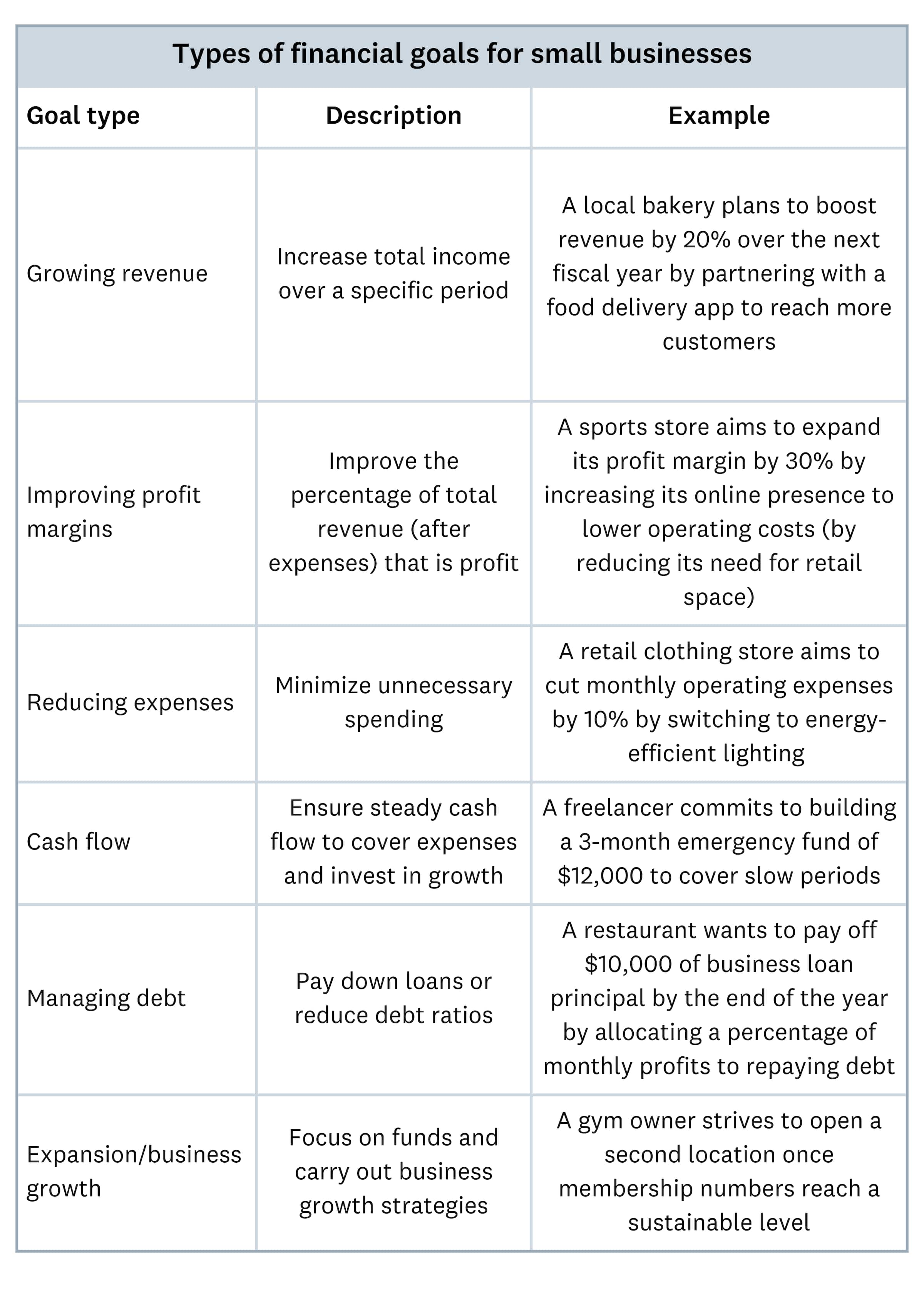

Types of financial goals for small businesses

Not all financial goals look the same. The right goals for your business depend on where you are right now and where you want to go. Here are 6 categories of financial goals that cover the core areas of small business finances.

- Revenue growth: Targets for increasing total sales over a set period. For example, growing monthly revenue from $40,000 to $50,000 within 12 months. Revenue goals help you measure whether your sales and marketing efforts are working.

- Profit margins: Targets for keeping more of what you earn after expenses. For example, increasing your net profit margin from 10% to 15% by the end of the fiscal year. Profit goals make sure revenue growth actually reaches your bottom line.

- Expense reduction: Targets for lowering your operating costs without hurting quality. For example, reducing supply costs by 8% over the next 2 quarters by renegotiating vendor contracts. Cutting unnecessary expenses improves profitability even when revenue stays flat.

- Cash flow management: Targets for keeping enough cash on hand to cover your obligations. For example, maintaining at least 60 days of operating expenses in your business account at all times. Strong cash flow goals protect you from late payments and seasonal slowdowns. Explore strategies for managing your finances and cash flow.

- Debt reduction: Targets for paying down loans, credit lines, or other liabilities. For example, paying off a $25,000 business loan within 18 months by making $1,500 monthly payments. Reducing debt frees up cash for growth and lowers your interest costs. Learn more about how to manage business debt effectively.

- Operational expansion: Targets for investing in growth, such as opening a new location, hiring staff, or launching a product line. For example, saving $30,000 over 12 months to fund a second storefront. Expansion goals tie your ambitions to a realistic financial plan. See more tips for growing your business.

Financial goal examples for small businesses

The best financial goals are tailored to your specific industry and business stage. Here are 4 examples that show how different types of small businesses can set concrete, actionable financial targets.

Retail store: increase quarterly revenue by 15%

A boutique clothing store with $120,000 in quarterly revenue sets a goal to reach $138,000 per quarter within 6 months. The owner plans to launch an online shop, run seasonal promotions, and introduce a loyalty program to drive repeat purchases. Xero Small Business Insights data shows that US small business sales can fluctuate significantly from quarter to quarter, so tracking revenue monthly helps you catch dips early and adjust your approach.

Construction company: improve net profit margin to 12%

A residential remodeling company currently operating at a 7% net profit margin sets a goal to reach 12% within 1 year. The owner reviews project-level costs, identifies materials where bulk purchasing could save 10%, and tightens scope management to reduce overruns. Tracking profit per project, rather than just total revenue, reveals which jobs are worth taking and which ones drain resources.

Freelance consultant: build a 3 month cash reserve

A freelance marketing consultant with $5,000 in monthly expenses sets a goal to save $15,000 in a dedicated business savings account within 9 months. She automates a $1,700 monthly transfer from her operating account and adjusts her invoicing terms from net-60 to net-30. For freelancers, a cash reserve is especially important because income can be unpredictable from month to month.

Cafe owner: reduce food waste costs by 20%

A cafe spending $2,500 per month on wasted ingredients sets a goal to bring that number down to $2,000 within 6 months. The owner implements daily inventory tracking, adjusts order quantities based on sales patterns, and introduces a rotating specials menu to use surplus items. Reducing waste improves profit margins without raising prices or cutting staff.

Set SMART financial goals for your business

Setting a financial goal without a clear framework often leads to vague targets you can't act on. The SMART framework gives your goals structure by making sure each one is specific, measurable, achievable, relevant, and time-bound.

How to set SMART financial goals

Each letter in SMART represents a criterion your goal needs to meet. Here's what each one means for your finances.

- Specific: Define exactly what you want to achieve. "Increase revenue" is too vague. "Increase monthly revenue from online sales by $5,000" is specific.

- Measurable: Attach a number so you can track progress. Use dollar amounts, percentages, or unit counts.

- Achievable: Set a target that stretches your business but is realistic given your current resources and market conditions.

- Relevant: Make sure the goal connects to your broader business priorities. A revenue goal matters more than a social media follower count if you're focused on profitability.

- Time-bound: Set a deadline. Goals without deadlines become wishes.

You can use this formula to write any SMART financial goal:

[Action] + [specific metric] + [target number] + [timeframe]

Here are 2 worked examples that put this formula into practice.

Example 1: revenue growth. A landscaping company wants to grow its revenue. Using the SMART formula, the owner writes: "Increase monthly revenue from $28,000 to $35,000 within 6 months by adding 3 recurring commercial maintenance contracts." This goal is specific (monthly revenue from commercial contracts), measurable ($35,000 target), achievable (3 new contracts is realistic), relevant (commercial contracts provide steady income), and time-bound (6 months).

Example 2: expense reduction. A small bakery wants to lower ingredient costs. The owner writes: "Reduce monthly ingredient spending from $4,200 to $3,600 within 4 months by switching to 2 local suppliers and reducing order frequency from weekly to biweekly." This goal has a specific metric (ingredient costs), a measurable target ($3,600), an achievable plan (supplier switch and order consolidation), relevance to profitability, and a clear deadline (4 months).

How to set financial goals in 6 steps

Knowing the theory behind financial goals is one thing. Actually setting them for your business is another. These 6 steps walk you through the process from start to finish.

1. Review your current financial position

Before you set any new goals, get a clear picture of where your business stands right now. Pull up your profit and loss statement, balance sheet, and cash flow statement for the past 12 months. Look at your total revenue, net profit, outstanding debts, and how much cash you have on hand.

This baseline tells you what's working and what isn't. If your revenue is growing but your profit margin is shrinking, that's a different problem than flat revenue with healthy margins. You can't set realistic goals without understanding your starting point.

2. Define your business priorities

Decide what matters most to your business over the next 6 to 12 months. Are you focused on growth, stability, or paying down debt? Your priorities shape which types of financial goals you should set first.

If you're a new business still building a customer base, revenue growth might be your top priority. If you've been operating for several years but feel stretched thin, improving cash flow or cutting expenses could be more important. Write down your top 2 to 3 priorities before moving to the next step.

3. Set specific targets using the SMART framework

Turn each priority into a SMART goal with a concrete number and deadline. Use the formula from the previous section: action + specific metric + target number + timeframe.

For each goal, write down why you chose that specific target and how you plan to reach it. A goal like "increase revenue by 20% in 12 months" is only useful if you also know the steps you'll take: launching a new product, increasing ad spend, raising prices, or expanding into a new market.

4. Break goals into smaller milestones

Large goals feel more manageable when you split them into monthly or quarterly checkpoints. If your annual revenue goal is $600,000, your quarterly milestone is $150,000 and your monthly target is $50,000.

Milestones let you check progress along the way instead of waiting until the deadline to find out you're behind. They also make it easier to spot seasonal patterns. If your business naturally slows down in January, you can adjust your monthly targets to reflect that.

5. Assign accountability and resources

Every goal needs someone responsible for tracking it and the resources to make it happen. If you're a solo operator, that's you. If you have a team, assign each goal to the person who has the most influence over that outcome.

Also consider what you'll need to invest. Cutting expenses by 10% might require new software or renegotiating contracts. Growing revenue by 25% might require hiring a salesperson or increasing your marketing budget. Factor these costs into your plan so your goals are realistic.

6. Schedule regular reviews

Set a recurring calendar event to review your goals. Monthly reviews work for most small businesses. Quarterly reviews are fine for longer-term goals. The point is to look at your actual numbers, compare them to your targets, and decide whether you need to adjust your approach.

During each review, ask yourself 3 questions: Are you on track? If not, what changed? What will you do differently before the next review? This habit turns goal-setting from a one-time exercise into an ongoing management practice.

Financial basics every small business needs

Before you chase ambitious growth targets, make sure your financial foundations are in place. These 3 basics protect your business from unexpected setbacks and give you a stable platform to build from.

Build an emergency fund

Every small business should have enough cash saved to cover 3 to 6 months of operating expenses. Add up your rent, payroll, insurance, loan payments, and other recurring costs, then multiply by 3 for a starting target or 6 for a more comfortable cushion.

If saving that amount feels impossible right now, start with 1 month of expenses and build from there. Automate a fixed transfer to a separate savings account each month so the fund grows without you having to think about it. This reserve keeps you from taking on emergency debt when a client payment is late, equipment breaks, or business slows down seasonally.

Manage your debt strategically

Not all debt is equal. High-interest credit card debt costs you more over time than a low-interest business loan, so focus your extra payments on the most expensive debt first. List all your outstanding balances, their interest rates, and minimum payments in one place.

2 common approaches can help you make progress. The avalanche method targets the highest-interest debt first, saving you the most money over time. The snowball method targets the smallest balance first, giving you quick wins that build momentum.

Choose the approach you'll actually stick with. The best debt reduction plan is the one you follow consistently.

Create a working budget

A budget is your financial plan in action. It maps out your expected income and expenses for each month so you can see where your money goes before it's gone. Start by listing your fixed costs such as rent and insurance, alongside variable costs like supplies and marketing, then compare them against your projected revenue.

Review your budget against actual results each month. If you consistently overspend in a category, either adjust the budget to reflect reality or find ways to reduce business costs. A budget that sits in a spreadsheet and never gets checked is little more than a wish list. Tools like Xero's budgeting features let you set budgets and compare them to your actuals in real time.

How to track and review your financial goals

Setting financial goals is only the beginning. You need a system for tracking progress, spotting problems, and adjusting your plan as conditions change. Here's how to build that system into your regular routine.

Set a review schedule

Monthly reviews work best for most small businesses. Block 1 to 2 hours at the end of each month to sit down with your financial reports and compare actual results to your targets. Quarterly reviews give you a chance to zoom out, assess trends, and decide whether your goals still make sense.

Keep your reviews consistent. Pick a date, put it on your calendar, and treat it like any other business appointment you wouldn't cancel. Skipping reviews is how small problems turn into big ones.

Use financial dashboards

A financial dashboard pulls your key metrics into 1 view so you don't have to dig through spreadsheets every time you want to check your progress. Most cloud accounting software includes a dashboard that shows your cash position, outstanding invoices, upcoming bills, and profit and loss summary.

The best dashboards update automatically as transactions come in, so you always see current numbers. If your dashboard is out of date because it relies on manual data entry, you're making decisions based on old information.

Automate your tracking

Manual tracking eats up time and introduces errors. Connecting your bank accounts to your accounting software means transactions flow in automatically. Automated invoicing and bill payment reminders keep your cash flow data accurate without extra effort.

Automation also helps you catch issues faster. When your accounting software categorizes transactions in real time, you can spot an unusually large expense or a missing payment the day it happens, not 3 weeks later during a manual reconciliation.

Track the right metrics

Focus on the metrics that connect directly to your goals. If your goal is to improve cash flow, track your accounts receivable aging, average days to payment, and cash balance trend. If your goal is to grow revenue, track monthly sales, average transaction value, and customer acquisition cost.

Don't try to track everything at once. Pick 3 to 5 key metrics that align with your top financial goals and review those consistently. You can always add more once you've built the habit of regular tracking.

Simplify your financial goal tracking with Xero

Setting financial goals is the plan. Tracking them consistently is what makes the plan work. Xero brings your bank transactions, invoicing, bills, and reporting into 1 place so you can see exactly where your business stands at any time.

With automated bank feeds and real-time reporting, Xero makes it easy to compare your actual results to your targets without spending hours on spreadsheets. You can set budgets and pull financial reports in a few clicks, so you spend less time on admin and more time running your business with Xero. Get one month free.

FAQs on setting financial goals

Here are answers to frequently asked questions about setting financial goals.

How will my financial goals affect the growth of my business?

Financial goals give your growth a direction and a pace. Instead of chasing every opportunity, you focus on the moves that actually improve your revenue, margins, or cash position. Businesses that set specific financial targets are better positioned to invest wisely, manage risk, and scale sustainably.

What's the difference between short-term and long-term financial goals?

Short-term financial goals typically span 1 to 12 months and focus on immediate improvements like reducing expenses, building a cash reserve, or paying off a credit card. Long-term goals cover 1 to 5 years or more and target bigger outcomes like opening a second location, reaching $1 million in annual revenue, or eliminating all business debt. You need both: short-term goals keep you moving, and long-term goals keep you on course.

How often should I review my financial goals?

Review your financial goals at least once a month. Monthly reviews let you catch problems early and make adjustments before small issues compound. Schedule a deeper quarterly review to assess whether your goals still align with your business priorities and market conditions.

What are common mistakes to avoid when setting financial goals?

The most common mistake is setting goals that are too vague, like "increase profit" with no target number or deadline. Other frequent errors include setting too many goals at once, ignoring your current financial position when choosing targets, and failing to break annual goals into smaller monthly milestones. Start with 2 to 3 focused goals and build from there.

How can I involve my team in achieving our financial goals?

Share your financial goals openly and explain how each team member's work connects to them. If your goal is to increase revenue by 15%, show your sales team their individual targets and give them regular progress updates. Consider tying bonuses or incentives to specific goal milestones so everyone benefits when the business hits its numbers.

How do I set financial goals during uncertain economic times?

Focus on goals you can control, like reducing expenses, improving cash flow, and building your emergency fund. Set shorter timeframes of 3 to 6 months instead of annual targets so you can adapt quickly as conditions change. Review your goals more frequently during uncertain periods and be willing to revise your targets based on current data rather than outdated projections.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Get one month free

Sign up to any Xero plan, and we will give you the first month free.