Net operating profit after tax: formula and examples

Learn what NOPAT is, how to calculate it, and how to use it to compare businesses and measure performance.

Written by Kari Brummond—Content Writer, Accountant, IRS Enrolled Agent. Read Kari's full bio

Published Tuesday 9 June 2026

Table of contents

Key takeaways

- Net operating profit after tax (NOPAT) measures how much profit your core business generates after taxes, excluding loan interest and non-operating income like investment gains.

- Use the formula NOPAT = operating profit × (1 − tax rate) to isolate your true operational profitability, regardless of how you finance your business.

- NOPAT lets you compare businesses fairly across different debt levels and tax situations, making it useful for benchmarking and acquisition decisions.

- Track NOPAT over time to spot trends in operational performance and calculate Economic Value Added (EVA) to see whether your business earns more than its cost of capital.

What is NOPAT?

Net operating profit after tax (NOPAT) measures how much profit your business earns from its core operations after paying taxes. It strips out financing costs and non-operating income to show your true operational profitability.

NOPAT focuses only on your main business activities. It excludes items that have nothing to do with day-to-day operations.

Specifically, NOPAT excludes:

- Interest expenses: loan payments, credit card interest, or other debt costs

- Non-operating income: investment gains, asset sales, or rental income from side activities

- Financing decisions: the impact of how you fund your business

Corporate filings often define NOPAT as net income adjusted for net interest expense and the effective income tax rate. This metric shows your return on invested capital by measuring how efficiently your operations generate profit.

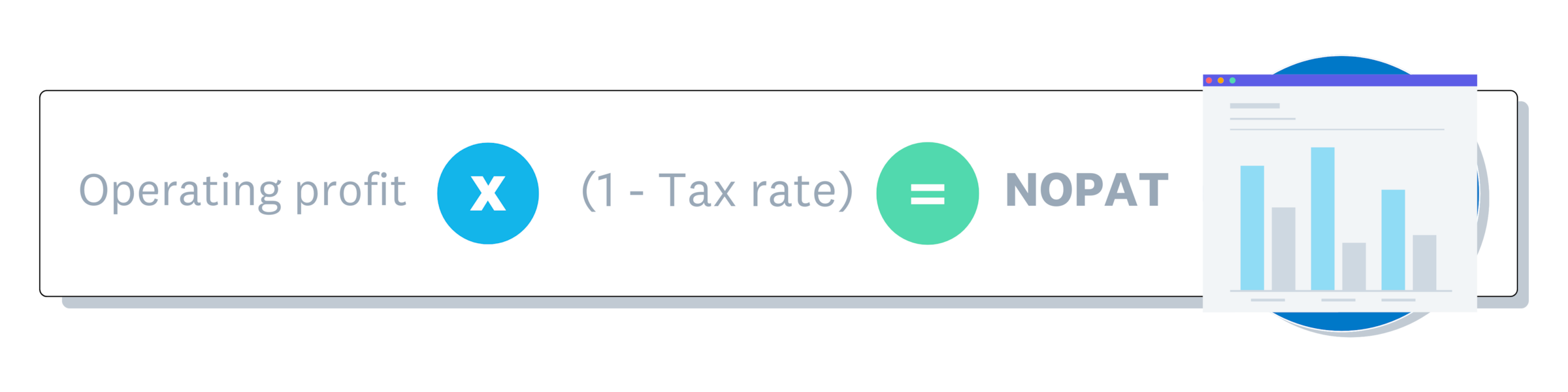

NOPAT formula explained

The NOPAT formula calculates your after-tax operating profit in one step:

NOPAT = operating profit × (1 − tax rate)

This formula has 2 components:

- Operating profit: your earnings from core business activities before tax and interest, excluding non-operating income

- Tax rate: your effective tax rate, expressed as a decimal

The expression (1 − tax rate) gives you the after-tax multiplier. For example, a 25% tax rate means you keep 75% of your operating profit. Multiply your operating profit by 0.75 to get NOPAT.

Note that operating profit and EBIT (earnings before interest and taxes) are not the same thing. Operating profit includes only income from your main business. EBIT can include non-operating income sources like investment gains. For an accurate NOPAT, use operating profit as your starting point.

How to calculate NOPAT

You can calculate NOPAT using 2 different methods. Choose the one that best fits the financial data you have available.

Method 1: Using operating income

This is the most direct approach. Start with your operating profit and apply the tax rate.

1. Determine operating profit

Find your operating profit on your income statement. You can also calculate it by subtracting operating expenses from gross profit. Understanding your gross profit margin is a useful first step. This gives you earnings before tax and interest, excluding non-operating income.

2. Find the tax rate

Calculate your effective tax rate using this formula:

Effective tax rate = income tax paid ÷ pre-tax income

For example, if you paid $12,500 in taxes on $50,000 of pre-tax income, your effective tax rate is 25%.

3. Apply the formula

Multiply your operating profit by (1 − tax rate):

- Operating profit: $50,000

- Tax rate: 25%

Calculation: $50,000 × (1 − 0.25) = $50,000 × 0.75 = $37,500

Your core business operations generate $37,500 per year after taxes, excluding financing costs.

Method 2: Using net income

If you only have net income figures, you can work backward to find NOPAT. This method adds back interest and taxes, then applies the tax rate to isolate operating profit after tax.

The formula is:

NOPAT = (net income + interest expense + taxes) × (1 − tax rate)

Here is a worked example:

- Net income: $30,000

- Interest expense: $5,000

- Taxes paid: $10,000

- Tax rate: 22%

First, add back interest and taxes: $30,000 + $5,000 + $10,000 = $45,000. This reconstructs your pre-tax, pre-interest operating income.

Then apply the tax rate: $45,000 × (1 − 0.22) = $45,000 × 0.78 = $35,100

Your NOPAT is $35,100.

NOPAT calculation example

Here is a detailed example using a realistic small business scenario. Both methods arrive at the same NOPAT, so you can use whichever fits the data you have.

Imagine you own a landscaping company with these financials:

- Revenue: $400,000

- Cost of goods sold: $160,000

- Operating expenses: $140,000

- Interest expense on a business loan: $10,000

- Effective tax rate: 24%

Method 1 (from operating income):

Operating profit = $400,000 − $160,000 − $140,000 = $100,000

NOPAT = $100,000 × (1 − 0.24) = $100,000 × 0.76 = $76,000

Method 2 (from net income):

Pre-tax income = $100,000 − $10,000 = $90,000 (operating profit minus interest)

Taxes = $90,000 × 0.24 = $21,600

Net income = $90,000 − $21,600 = $68,400

NOPAT = ($68,400 + $10,000 + $21,600) × (1 − 0.24) = $100,000 × 0.76 = $76,000

Both methods produce a NOPAT of $76,000. This tells you the landscaping company generates $76,000 in after-tax profit from its core operations, regardless of its loan.

Why is NOPAT important?

NOPAT reveals your operational efficiency regardless of debt levels or financing structure. It gives you a clearer picture of business performance than net income alone.

Reveals true business performance

NOPAT isolates operational performance from financing decisions. This gives you a clear view of how well your core business generates profit after taxes.

Public companies must ensure their non-GAAP calculations do not improperly eliminate or smooth items that are reasonably likely to recur within 2 years.

NOPAT analysis helps you:

- Pinpoint operational inefficiencies that reduce profitability

- Evaluate expansion opportunities based on core performance

- Assess businesses with different financial structures on equal footing

Helps you compare businesses fairly

NOPAT removes the impact of financing choices and local tax differences. This makes it possible to compare businesses that operate under very different conditions.

A profitable business may show low net income simply because it carries high debt. NOPAT strips that distortion away. You can also compare operational efficiency across regions using NOPAT to measure profitability consistently.

For example, imagine you are comparing 2 businesses for acquisition:

- Company A: $100,000 net profit, low debt

- Company B: $80,000 net profit, high debt

Company B's NOPAT reveals $120,000 in operational profit. This shows Company B has stronger earning potential once you address its financing structure.

Helps you make better decisions

NOPAT feeds into Economic Value Added (EVA), which measures whether your business generates returns above its cost of capital.

To calculate EVA, subtract your total invested capital multiplied by the cost of capital from NOPAT.

For example, your NOPAT is $50,000. Your business has $100,000 in loans at 6% interest, and you invested $100,000 in cash. Your total capital investment is $200,000 at an average cost of 3%.

Calculation: $50,000 − ($200,000 × 3%) = $50,000 − $6,000 = $44,000 EVA

This means the $200,000 invested in your company generates $44,000 per year above its cost of capital. A positive EVA signals that your business creates value for its owners.

NOPAT vs net income

NOPAT and net income both measure profit, but they differ in scope. Net income includes all business activities. NOPAT focuses purely on operational performance after taxes.

Net income includes:

- Operating costs: expenses, depreciation, amortization

- Financing costs: interest on loans and debt

- Non-operating items: investment income, asset sales

- All taxes: your complete tax burden

NOPAT includes only:

- Operating costs: core business expenses

- Operating taxes: taxes on business operations

- Depreciation and amortization: non-cash charges tied to your core assets

Here is a practical example. A bakery has $100,000 in net income. It earns $12,000 from renting parking lot space to a food truck and pays $8,000 in interest on loans.

Net income already deducts interest and includes the rental income. To estimate the bakery's core operating income, remove both: $100,000 − $12,000 + $8,000 = $96,000. Then apply your tax rate to $96,000 to get NOPAT.

If a business has no debt or non-operating income, its NOPAT and net income are the same.

Operating profit vs NOPAT

Operating profit and NOPAT both measure core business performance, but they handle taxes differently. Operating profit is calculated before taxes. NOPAT is calculated after taxes.

Operating profit shows earnings before taxes and interest. NOPAT shows earnings after taxes but before interest. Both exclude financing decisions, but NOPAT gives you a more realistic picture of the profit you actually keep from operations.

NOPAT vs unlevered free cash flow

NOPAT and unlevered free cash flow (UFCF) both measure operational performance without the influence of debt. However, UFCF goes further by accounting for real cash movements that NOPAT ignores.

NOPAT tells you your after-tax operating profit on paper. UFCF adjusts that figure for:

- Depreciation and amortization: these non-cash expenses reduce NOPAT but do not affect actual cash flow, so UFCF adds them back

- Capital expenditures: UFCF subtracts the cash you spend on equipment, vehicles, or other long-term assets

- Working capital changes: UFCF accounts for cash tied up in inventory, accounts receivable, and accounts payable

UFCF gives you a more comprehensive picture of the cash your business actually generates. NOPAT is simpler to calculate and useful for profitability comparisons. UFCF is better for valuation and understanding how much cash is available to reinvest or distribute.

How to use NOPAT in financial analysis

NOPAT is more than a single metric. It serves as a building block for several types of financial analysis that help you make better business decisions.

Here are 4 ways to put NOPAT to work:

- Discounted cash flow (DCF) analysis: NOPAT is the starting point for projecting future cash flows when valuing a business. If you are buying or selling a company, DCF models use NOPAT to estimate what the business is worth today.

- Benchmarking against competitors: because NOPAT removes financing and tax distortions, you can compare your operational profitability with competitors of different sizes and capital structures. Explore profitability ratios for more ways to benchmark.

- EVA calculations: subtract your cost of capital from NOPAT to see whether your business creates or destroys value. A positive EVA means your operations earn more than the cost of funding them.

- Strategic planning: track NOPAT quarter over quarter to measure whether operational changes, such as price adjustments or cost-cutting, actually improve your bottom line. See KPIs for your business for other metrics to track alongside NOPAT.

Track your NOPAT with Xero

Calculating NOPAT starts with accurate financial data. Xero's accounting software gives you real-time access to your income statements, operating expenses, and tax figures, so you have the numbers you need in one place.

With customizable reports and analytics tools, you can pull operating profit and tax data in a few clicks. Xero automates bank reconciliation and expense tracking, so your figures stay current without manual data entry. Start tracking the metrics that matter for your business and Get one month free.

FAQs on NOPAT

Here are answers to frequently asked questions about NOPAT.

Why should you use NOPAT instead of net income?

Use NOPAT when you want to evaluate operational performance without the influence of financing decisions or non-operating activities. It makes comparisons more meaningful across companies with different debt structures or tax situations.

Can you use NOPAT for small businesses?

Yes. NOPAT works for any business size and is especially useful when comparing your performance to competitors or industry benchmarks.

How often should you calculate NOPAT?

Calculate NOPAT quarterly or annually to track operational performance trends. Regular calculations help you identify whether your core business is becoming more or less profitable over time.

What is the difference between NOPAT and EBIT?

EBIT measures pre-tax operational performance, while NOPAT measures after-tax operational performance. Both exclude interest expenses.

Does NOPAT include depreciation?

Yes. NOPAT includes depreciation because it is an operating expense that reduces operating profit, which is the starting point for calculating NOPAT.

What is NOPAT margin?

NOPAT margin is NOPAT divided by total revenue, expressed as a percentage, showing how much of each revenue dollar your operations convert into after-tax profit. A higher NOPAT margin indicates stronger operational efficiency. Learn more about profit margin calculations.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Get one month free

Sign up to any Xero plan, and we will give you the first month free.