Small business accounting: Build your system for success

Learn how to build a small business accounting system that saves time, cuts errors, and shows real time cash flow.

Written by Lena Hanna—Trusted CPA Guidance on Accounting and Tax. Read Lena's full bio

Published Monday 22 December 2025

Table of contents

Key takeaways

- Establish a dedicated business bank account as your first step to separate personal and business finances, which simplifies tax preparation, builds business credit, and provides legal protection.

- Choose between cash accounting (records transactions when money changes hands) and accrual accounting (records when transactions occur regardless of payment timing) based on your business size and complexity.

- Implement a general ledger system with five primary account types (assets, liabilities, revenue, equity, and expenses) to organize all financial transactions and generate accurate reports for lenders and tax compliance.

- Utilize accounting software to automate bookkeeping tasks, integrate with your bank accounts, and generate professional financial statements that save time and reduce manual errors.

What is small business accounting?

Small business accounting is the process of recording, tracking, and analyzing your business's financial activities. For regulatory purposes, some entities like Smaller Reporting Companies (SRCs) are defined by financial thresholds – such as having less than $100 million in annual revenues – and are eligible to provide scaled disclosures. It helps you understand your financial health, make informed decisions, and stay compliant with tax laws.

Think of it as the story of your business, told through numbers. It helps you plan for growth and manage cash flow with confidence, so you can focus on running your business, not just your books.

Basic accounting terms you need to know

Getting to grips with your finances is easier when you understand the language. Here are a few key terms that form the foundation of your accounting system:

- Assets: What your business owns, like cash, equipment, or inventory

- Liabilities: What your business owes, such as loans or bills to suppliers

- Equity: The value of your business after subtracting liabilities from assets. It's what you've invested plus retained earnings and is a key component of financial health metrics like the debt-to-equity ratio, which compares a company's total debt to the amount invested by shareholders.

- Revenue: The income your business earns from sales of goods or services

- Expenses: The costs of running your business, like rent, salaries, and supplies

Why your small business needs an accounting system

An accounting system is your business's financial record-keeping foundation that tracks all money coming in and going out. This organized approach helps you understand your business performance and make informed decisions.

Your accounting system provides three key benefits:

- Financial clarity: see exactly how much money you're making and spending

- Strategic planning: use accurate data to plan for growth and challenges

- Tax compliance: maintain organized records for easier tax preparation

Financial statements from your accounting system serve multiple critical purposes:

- Loan applications: lenders require profit and loss statements, balance sheets, and cash flow reports

- Tax audits: organized records help you quickly provide documentation to the IRS

- Business decisions: accurate financial data helps you identify profitable areas and cost-cutting opportunities

Choose your accounting method: cash vs accrual

Choose between two main accounting methods based on your business size and needs:

Cash accounting records transactions only when money changes hands. You track income when customers pay you and expenses when you pay bills.

- Best for: small businesses with simple operations and immediate payments

- Benefits: easier to understand, matches your actual cash flow

Accrual accounting records transactions when they happen, regardless of payment timing. You track income when you send invoices and expenses when you receive bills.

- Best for: larger businesses, those with inventory, or companies extending credit

- Benefits: more accurate picture of business performance and profitability

What is a general ledger?

A general ledger is the master record that contains all your business's financial transactions in one organized system. Setting up your general ledger early helps you track every dollar and maintain accurate financial records.

Modern general ledgers use accounting software instead of paper books. The digital format provides the same organized record-keeping with added benefits like automatic calculations and instant reporting.

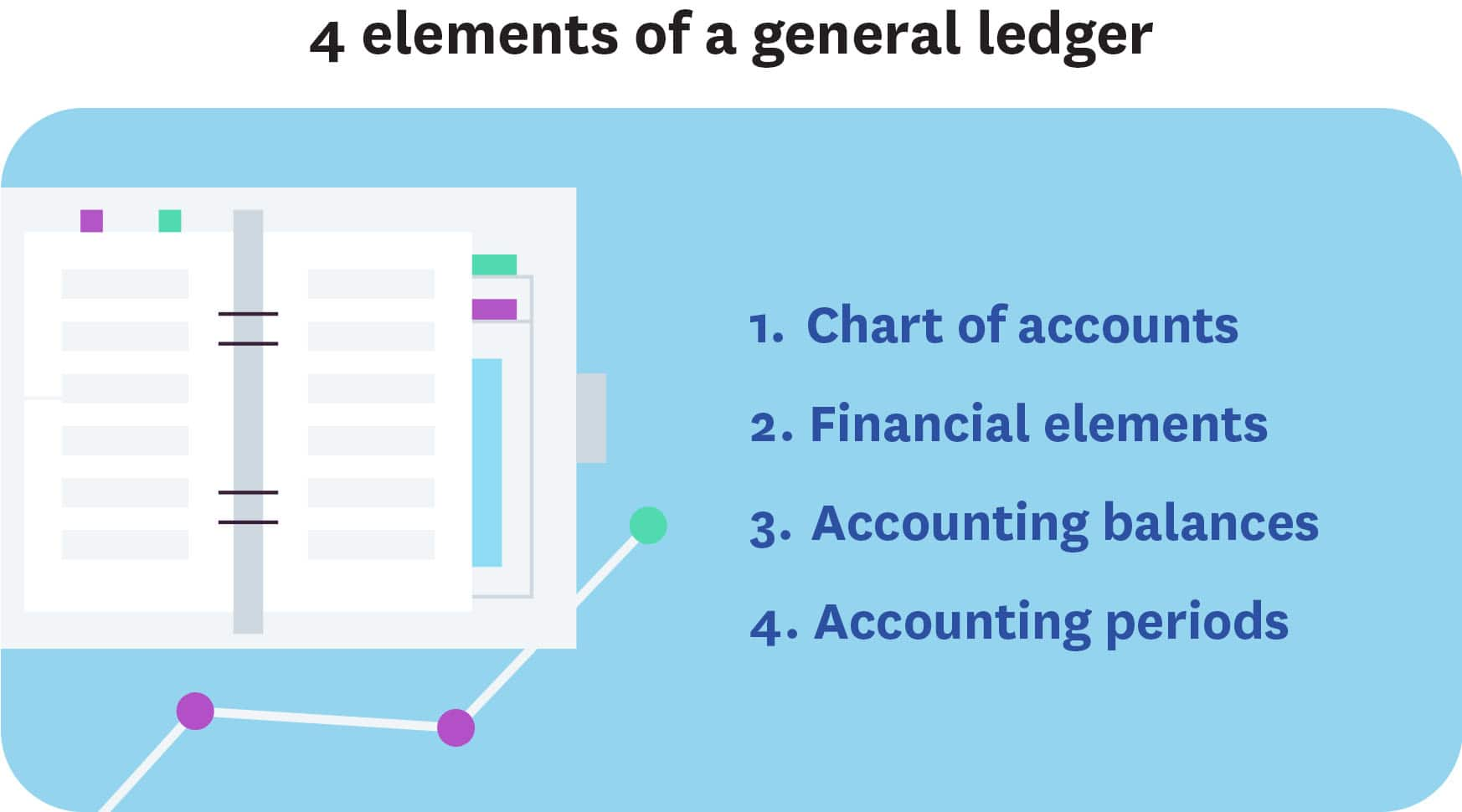

Your general ledger contains four essential elements:

- Chart of accounts: complete list of categories for organizing all business transactions

- Financial transactions: records of money exchanges with customers, vendors, and lenders

- Account balances: running totals that show current amounts in each account

- Accounting periods: time frames for financial reporting (monthly, quarterly, or annually); the Internal Revenue Service (IRS) provides specific rules for determining these periods, for example, a partnership must adopt the tax year of partners who own a majority interest

Features of a chart of accounts

Your chart of accounts organizes all business transactions into logical categories that match your industry and business model. Each business needs different account categories: a restaurant tracks food costs while a consulting firm focuses on professional services.

Consider consulting an accounting professional to set up accounts that align with your specific business needs and tax requirements.

5 primary account types

5 primary account types organize all your business's financial information:

- Asset accounts: track items your business owns (cash, equipment, inventory, property)

- Liability accounts: record money your business owes (loans, credit cards, accounts payable, taxes)

- Revenue accounts: capture income your business earns (sales, service fees, interest income)

- Equity accounts: show ownership value (owner investments, retained earnings, distributions)

- Expense accounts: track costs to run your business (rent, utilities, salaries, supplies)

General ledger sub-accounts

Back when people kept their books with pen and paper, they would have a main account with separate subledgers, such as accounts receivable or inventory. This helped break financial reporting down further.

These days, you can set up a similar structure in your accounting software and tailor these accounts to your needs. If you set them up well, they give you a clear overview of every area of your business that earns or spends money.

Common sub-accounts by category:

- Assets: checking account, savings account, accounts receivable, inventory, equipment

- Liabilities: accounts payable, credit cards, loans, sales tax payable, payroll taxes

- Revenue: product sales, service income, consulting fees, interest income

- Equity: owner's equity, retained earnings, capital contributions

- Expenses: rent, utilities, insurance, office supplies, marketing costs

Details included on a general ledger

Although your accountant or accounting software keeps your books, it is important to know what information is in your general ledger. This can help you better understand your financial reports and the information contained in them. If you are starting out and establishing your own general ledger, create a template to standardize your ledger and accounting system.

Your general ledger includes the following:

- Account name: The name of the account.

- Account number: Not all accounting systems use account numbers. But when they are used, each account is assigned a unique number to assist with locating and identifying accounts.

- Date: The date allows you to find transactions and track them more easily and is required for tax and most reporting purposes.

- Opening balance: The starting balance for the account. Some accounts start at $0, and some will carry over from a previous financial period.

- Customer/vendor: Name of the customer or vendor for the transaction.

- Description: This column provides space for the details about each transaction.

- Debit and credit columns: Debits will increase your assets and expenses and decrease your liabilities, revenue and equity accounts. Credits will decrease your assets and business expenses and increase your liabilities, revenue and equity accounts.

- Closing balance: The closing balance for an account at the end of the financial period.

Steps for developing your accounting system

Stay involved in your accounting system setup even when working with professionals or software. Understanding how your system works helps you make better business decisions and communicate effectively with lenders, investors, and advisors.

Your accounting system generates all financial reports you'll need for business planning and stakeholder meetings.

1. Create a bank account

A business bank account separates your personal and business finances, which is essential for accurate accounting and tax compliance.

Key benefits of a dedicated business account:

- Tax preparation: easily identify business expenses and income

- Financial clarity: track business cash flow without personal transactions

- Legal protection: maintain separation between personal and business assets

- Credit building: establish business credit history for future loans

- Professional image: business checks and cards look more credible to customers

2. Choose your tracking method

You will need to choose an appropriate system to track your business transactions. There are three ways to do this.

- Accounting software such as Xero.

- Use a CPA or accountant to handle it for you.

- Use an Excel template. Some small businesses may start off doing this until they are established.

3. Establish your chart of accounts

When you establish your chart of accounts, you will need to set up the accounts for your general ledger. This system is based on double-entry bookkeeping, so every transaction has a debit and credit entry.

4. Organize your records

You will need to decide how you want to keep your documents, such as receipts for transactions. Decide if you will keep soft copies or hard copies of them and then how you will organize them. However you decide to do your recordkeeping, you should be consistent, organize by type of transaction and in chronological order.

Track your business expenses

Keeping a close eye on your expenses is crucial for managing your budget, maximizing tax deductions, and understanding your profitability. From office supplies and software subscriptions to travel and marketing costs, every dollar spent impacts your bottom line.

A consistent tracking system, whether through accounting software or organized digital receipts, ensures you have an accurate record of where your money is going. This helps you identify areas to save and makes tax time much less stressful.

Advantages of using accounting software

Accounting software automates time-consuming bookkeeping tasks and generates professional financial reports instantly.

Key advantages for small businesses:

- Time savings: automate data entry, calculations, and report generation

- Professional reports: create balance sheets and income statements in minutes

- Stakeholder ready: produce lender and investor-quality financial documents

- Real-time insights: access current financial data anytime, anywhere

Bank integration keeps your financial data current by automatically importing transactions from your business accounts. This eliminates manual data entry and reduces errors.

Cloud access lets you check your business finances from any device, anywhere. Mobile apps provide on-the-go access to key reports and account balances.

Payroll integration handles employee payments, tax calculations, and compliance reporting automatically, saving hours of manual work each pay period.

Accurate records make it easier to track your business’s financial transactions. They streamline your income tax filing because all the information you need, including tax deductions, is easy to find.

When you plan and forecast your finances, summary reports show trends in your income and spending. This makes it easier to get a clear overall picture of your business's performance.

Start building your accounting system with Xero

Xero's small business accounting software can make your bookkeeping much easier and save you time.

Ready to run your business, not your books? Get one month free and get started with Xero today.

FAQs on small business accounting

Here are answers to a few common questions about managing your business finances.

Can I do my own accounting for my business?

Yes, many small business owners manage their own books, especially when starting out. Using intuitive accounting software can simplify the process, automate tasks, and help you stay organized. As your business grows, you might choose to work with an accountant or bookkeeper for more complex tasks and strategic advice.

How much does an accountant for a small business cost?

The cost of an accountant varies based on your needs and location. Services can range from a few hundred dollars for a one-time consultation to several thousand dollars per year for ongoing bookkeeping, payroll, and tax services. Many accountants offer monthly packages, making it easier to budget for professional support.

What's the first step to setting up small business accounting?

Opening a separate business bank account is the best first step. It keeps your personal and business finances distinct, which simplifies tracking transactions, managing cash flow, and preparing for tax season. It creates a clear financial foundation for your business.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Get one month free

Sign up to any Xero plan, and we will give you the first month free.