What is cash flow?

Cash flow tracks money moving in and out of your business. Learn how to calculate, forecast, and manage it.

Published Wednesday 1 July 2026

Table of contents

Key takeaways

- Cash flow is the total movement of money into and out of your business over a set period, and it determines whether you can pay bills, cover payroll, and invest in growth.

- There are 3 main types of cash flow: operating, investing, and financing. Tracking each one separately gives you a clearer picture of where your money is coming from and where it's going.

- Positive cash flow doesn't always mean your business is profitable, and a profitable business can still run out of cash. Understanding the difference helps you make smarter financial decisions.

- Regular cash flow forecasting and proactive management, such as invoicing promptly and negotiating payment terms, help you avoid shortfalls before they become problems.

What is cash flow?

Cash flow is the net amount of money moving into and out of your business over a specific period. It measures whether your business has enough cash on hand to cover its obligations and pursue new opportunities.

Money coming in, known as cash inflows, includes revenue from sales, loan proceeds, and returns on investments. Money going out, known as cash outflows, covers expenses like rent, payroll, supplier payments, and taxes.

When your inflows exceed your outflows, you have positive cash flow. When outflows exceed inflows, you have negative cash flow. A business can be profitable on paper but still face cash shortages if the timing of payments and receipts doesn't line up.

It's also worth noting that "cash" in this context doesn't just mean physical money in the bank. It includes cash equivalents: assets that can be converted to a known amount of cash at short notice, typically within 90 days.

Why cash flow matters for your business

Cash flow is the lifeblood of your business because it determines your ability to meet financial obligations day to day. Without enough cash on hand, you can't pay suppliers, employees, or lenders on time, regardless of how much revenue you're generating.

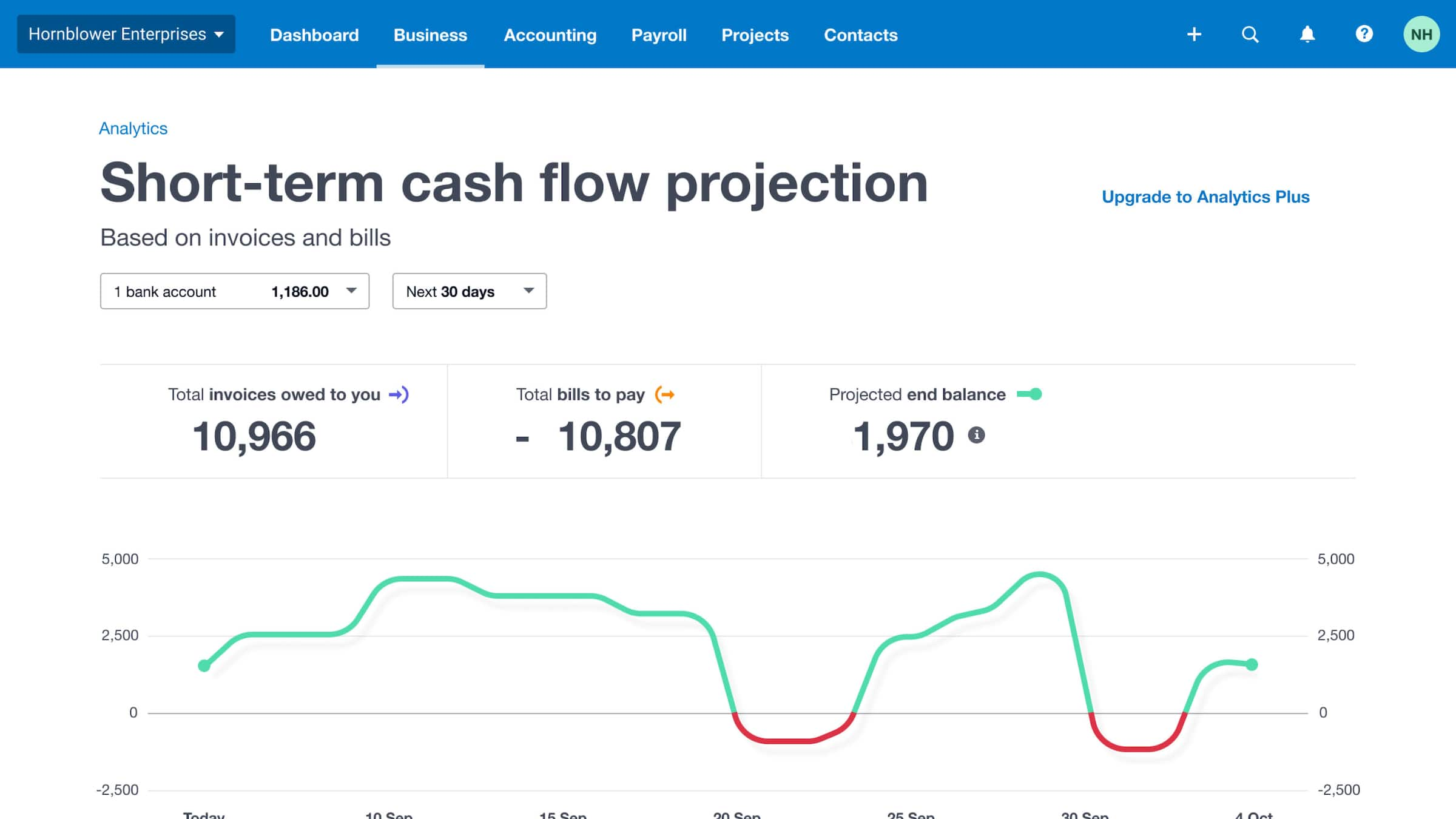

Small businesses can get a picture of future cash flow by accounting for upcoming bills and payments (example from Xero dashboard).

Strong cash flow also gives you the flexibility to act on growth opportunities. Whether you want to hire new staff, invest in equipment, or expand into a new market, you need available cash to make it happen.

Poor cash flow is 1 of the most common reasons small businesses fail. According to a SCORE study, 82% of small business failures involve cash flow problems. Keeping a close eye on your cash position helps you spot trouble early and take corrective action before a temporary shortfall becomes a crisis.

Recent data underscores why cash flow management matters so much. In 2025, US small business sales growth averaged just 2.4% year over year, roughly half the long-term average of 5.5%, according to Xero Small Business Insights. With tighter margins, having a clear picture of your cash position becomes even more important.

Beyond the numbers, healthy cash flow reduces financial stress. When you know you can cover upcoming expenses, you can focus on running and growing your business with confidence.

Types of cash flow

Cash flow is typically divided into 3 main categories based on the source or use of funds. Understanding each type helps you identify where your money is coming from and whether those sources are sustainable.

Cash flow from operations

Operating cash flow, sometimes called cash flow from operations (CFO), is the money generated by your core business activities. It includes cash received from customers minus the cash spent on day-to-day expenses like inventory, wages, rent, and utilities.

This is the most important type of cash flow for small businesses. If your operating cash flow is consistently positive, it means your business model is generating enough revenue to sustain itself. If it's consistently negative, you may need to rethink your pricing, reduce costs, or find ways to collect payments faster.

Payment timing also plays a major role. According to Xero Small Business Insights, US small businesses waited an average of 27.9 days to be paid in Q4 2025, and invoices were paid an average of 7.8 days late. Even when operations are profitable, these payment delays can create real cash flow gaps.

Cash flow from investing

Investing cash flow tracks money spent on or received from long-term assets. Purchases of equipment, property, or vehicles are cash outflows. Selling those same types of assets produces cash inflows.

Negative investing cash flow isn't necessarily a bad sign. It often means you're investing in the future of your business. However, if you're regularly selling assets to cover operating expenses, that's a red flag worth investigating.

Cash flow from financing

Financing cash flow covers money moving between your business and its owners or lenders. Cash inflows include proceeds from loans, lines of credit, or equity investments. Cash outflows include loan repayments, dividend payments, and share buybacks.

It's normal for newer businesses to show positive financing cash flow as they take on loans or bring in investors. Over time, a healthy business should rely less on financing and more on operating cash flow to fund its activities.

Free cash flow

Free cash flow (FCF) is the cash your business has left after covering operating expenses and capital expenditures. You can calculate it by subtracting capital expenditures from operating cash flow.

FCF shows how much cash is truly available for discretionary spending, whether that's paying down debt, distributing profits, or reinvesting in the business. A consistently positive free cash flow is a strong indicator of financial health.

How to calculate cash flow

Calculating your net cash flow gives you a clear snapshot of whether your business is bringing in more money than it's spending. The basic formula is straightforward.

Net cash flow = total cash inflows − total cash outflows

To calculate it, add up all the cash your business received during a specific period, including sales revenue, loan proceeds, and any other income. Then subtract all cash payments made during the same period, including operating expenses, loan repayments, and asset purchases.

For a more detailed view, you can calculate cash flow for each of the 3 categories separately.

- Operating cash flow = net income + non-cash expenses (like depreciation) + changes in working capital

- Investing cash flow = cash received from asset sales − cash spent on asset purchases

- Financing cash flow = cash received from loans or investments − cash spent on repayments or dividends

Free cash flow builds on operating cash flow with a simple adjustment.

Free cash flow = operating cash flow − capital expenditures

Xero's reporting and analytics tools can help you track these numbers in real time so you don't have to calculate them manually.

Cash flow statements explained

A cash flow statement is a financial report that summarizes the movement of cash into and out of your business over a specific period, such as a month, quarter, or year. It's 1 of the 3 core financial statements, alongside the balance sheet and income statement.

The statement is divided into 3 sections that mirror the types of cash flow.

- Operating activities: cash generated or spent through day-to-day business operations

- Investing activities: cash used to buy or received from selling long-term assets

- Financing activities: cash received from or paid to lenders and investors

At the bottom of the statement, you'll find the net change in cash for the period. This tells you whether your overall cash position increased or decreased. Comparing cash flow statements across multiple periods helps you spot trends and identify whether your business is becoming more or less cash-efficient over time.

If you're using Xero accounting software, you can generate cash flow statements automatically from your transaction data. This saves time and reduces the risk of manual errors.

Cash flow forecasting

Cash flow forecasting is the process of estimating how much cash your business will receive and spend over a future period. It helps you anticipate shortfalls before they happen and plan around them.

A basic cash flow forecast starts with your current cash balance, then adds expected inflows (like customer payments and other income) and subtracts expected outflows (like rent, payroll, and supplier payments) for each week or month in the forecast period.

Forecasting is especially valuable when conditions are volatile. Xero Small Business Insights found that US small business sales growth in 2025 swung from as low as 0.2% in October to 7.1% in September, making month-to-month planning difficult without a forward-looking projection.

The more accurate your forecast, the better positioned you are to make decisions. You might discover you need to delay a large purchase, accelerate invoicing, or arrange a line of credit before cash gets tight.

Forecasting doesn't need to be complicated. Even a simple spreadsheet can work for short-term projections. However, dedicated tools make the process faster and more reliable. Xero's cash flow forecasting features let you project future cash positions based on your actual financial data, giving you a more realistic view of what's ahead.

Aim to review and update your forecast regularly. Weekly reviews work well for businesses with tight margins, while monthly reviews may be sufficient for those with more stable cash positions.

How to manage and improve cash flow

Managing cash flow effectively means keeping more money coming in than going out, and making sure the timing works in your favor. Here are practical steps you can take to strengthen your cash position.

- Invoice promptly and follow up on overdue payments. The sooner you send invoices, the sooner you get paid. Set up automated reminders to reduce the time you spend chasing late payments.

- Offer early payment incentives. A small discount for paying within 10 days can motivate customers to settle invoices faster.

- Request deposits or partial payments upfront. For large projects or orders, collecting a portion of the payment before you start work improves your cash position.

- Negotiate longer payment terms with suppliers. If your suppliers allow 60-day terms instead of 30, you keep cash in your account longer.

- Review recurring expenses regularly. Cancel subscriptions and services you no longer use, and look for opportunities to reduce costs without compromising quality.

- Build a cash reserve. Setting aside a portion of your revenue each month creates a buffer for unexpected expenses or slow periods.

Xero customers who use online invoice payments get paid up to twice as fast, which can make a significant difference to your cash flow. Features like automatic bank feeds and daily reconciliation also help you stay on top of your cash position in real time.

Cash flow vs. profit

Cash flow and profit are related but measure different things. Cash flow tracks the actual movement of money into and out of your business, while profit measures revenue minus expenses on an accrual basis.

The key difference comes down to timing. Profit is recorded when a sale is made, even if the customer hasn't paid yet. Cash flow only reflects money that has actually been received or spent. This means you can show a profit on your income statement while having no cash in the bank.

For example, if you invoice a customer for $10,000 in March but they don't pay until May, your income statement records the revenue in March. Your cash flow statement won't reflect that money until May, when it actually arrives in your account.

This distinction matters because you can't pay bills with profit. You need actual cash. Many small businesses that fail are profitable on paper but unable to cover their short-term obligations because of cash flow gaps.

Tracking both metrics gives you a complete picture of your financial health. Profit tells you whether your business model is sustainable over time. Cash flow tells you whether you can keep the lights on today.

Cash flow vs. working capital and liquidity

Cash flow, working capital, and liquidity are all measures of your financial health, but each one tells you something different. Understanding how they relate helps you make better decisions about your business finances.

Cash flow measures the movement of money over a period of time. It shows whether your business generated or consumed cash during a given week, month, or quarter.

Working capital is the difference between your current assets (like cash, accounts receivable, and inventory) and your current liabilities (like accounts payable and short-term debt). It tells you how much money you'd have left after covering all your near-term obligations.

Liquidity measures how easily you can convert assets into cash to meet short-term commitments. It's often expressed as a ratio, such as the current ratio (current assets divided by current liabilities). A ratio above 1 means you have enough liquid assets to cover your upcoming bills.

A business can have positive cash flow but low working capital if most of its assets are tied up in inventory or receivables. Conversely, a business might have strong working capital on its balance sheet but still face cash flow problems if payments from customers are consistently late.

Monitoring all 3 metrics together gives you the clearest view of your short-term financial position and helps you plan accordingly.

Take control of your cash flow with Xero

Staying on top of your cash flow doesn't have to mean hours of manual tracking and guesswork. With the right tools, you can see exactly where your money is going, spot potential shortfalls early, and make informed decisions with confidence.

Xero brings your finances together in 1 place, giving you real-time visibility into your cash position. Automatic bank feeds, customizable reports, and cash flow forecasting tools help you manage your money with less manual work. Get one month free.

FAQs on cash flow

Here are answers to some frequently asked questions about cash flow.

What is the difference between positive and negative cash flow?

Positive cash flow means your business brought in more money than it spent during a given period, leaving you with surplus cash. Negative cash flow means your outflows exceeded your inflows, which can be a warning sign if it continues over multiple periods.

How often should you review your cash flow?

Most small businesses benefit from reviewing cash flow at least monthly, though weekly reviews are better if your margins are tight or your income is seasonal. Regular reviews help you catch problems early and adjust your spending or collection efforts before cash gets too low.

What causes cash flow problems in small businesses?

The most common causes include late-paying customers, overinvestment in inventory, unexpected expenses, and taking on too much debt. Seasonal fluctuations in revenue can also create temporary cash flow gaps that catch businesses off guard.

How does cash flow differ from revenue?

Revenue is the total amount you earn from sales, recorded when the transaction occurs. Cash flow reflects the actual money received and spent, so it accounts for the timing of payments and may differ significantly from revenue in any given period.

Handy resources

Advisor directory

You can search for experts in our advisor directory

Cash flow forecast template

Download our free template to help predict cash flow for your business

Business analytics with Xero

See future cash flow, check financial health and track metrics

Disclaimer

This glossary is for small business owners. The definitions are written with their requirements in mind. More detailed definitions can be found in accounting textbooks or from an accounting professional. Xero does not provide accounting, tax, business or legal advice.