Managing finances in a business: cash flow made easy

Learn smart ways to manage finances and cash flow, cut admin, avoid crunches, and grow profit.

Written by Jotika Teli—Certified Public Accountant with 24 years of experience. Read Jotika's full bio

Published Tuesday 3 March 2026

Table of contents

Key takeaways

- Separate your personal and business finances completely by opening dedicated business bank accounts and credit cards, paying yourself a consistent salary, and keeping all receipts organized to protect yourself legally and simplify tax preparation.

- Maintain three to six months of operating expenses in cash reserves and track your cash flow patterns regularly to identify seasonal slowdowns or problem periods before they threaten your business stability.

- Chase unpaid invoices consistently by setting clear payment terms, following up persistently with late-paying customers, and using accounting software to track aging invoices since late payments are a leading cause of cash flow problems.

- Review your financial reports monthly including profit and loss statements, balance sheets, and cash flow statements to spot warning signs early and make informed decisions about spending, pricing, and growth opportunities.

Money management matters

Managing your business finances means tracking money coming in and going out, planning for future expenses, and making informed decisions to keep your business profitable. Cash flow problems and poor financial management are leading causes of small business failure in the first few years.

Common financial pitfalls include:

- failing to plan: no budget or financial framework in place

- losing track of costs: expenses grow faster than revenue

- not chasing payments: unpaid invoices drain cash flow

- setting unrealistic goals: targets too high or too low to sustain growth

Taking practical steps now helps you control spending and grow your business without excessive risk. Here's how to get started.

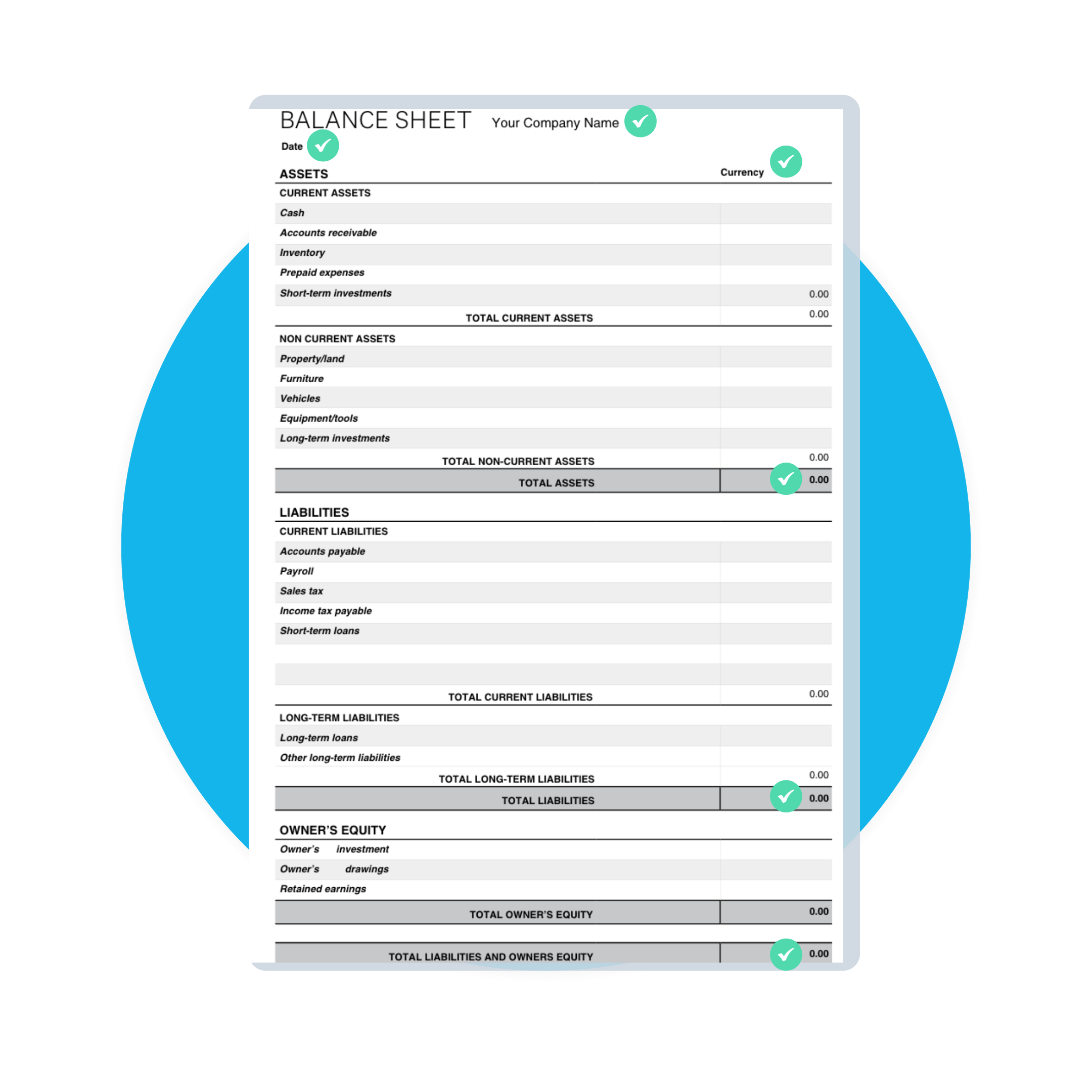

Understand balance sheet basics

A balance sheet shows your business's financial position at a specific point in time. It answers one essential question: what is your business worth right now?

The balance sheet has three components:

- assets: what your business owns (cash, equipment, inventory, accounts receivable)

- liabilities: what your business owes (loans, accounts payable, credit card balances)

- owner's equity: the difference between assets and liabilities, representing your ownership stake

The balance sheet follows a simple formula: Assets = Liabilities + Owner's Equity. If your assets exceed your liabilities, your business has positive equity. If liabilities exceed assets, you may have a solvency problem.

Review your balance sheet monthly to track whether your business is building value or accumulating debt. Your accountant can help you interpret the numbers and spot warning signs early.

Choose your accounting method

Your accounting method determines when you record income and expenses. This choice affects your taxes, financial reports, and how you track cash flow.

Small businesses typically choose between two methods:

Cash basis accounting:

- record income when you receive payment

- record expenses when you pay them

- simpler to manage for small businesses

- shows actual cash on hand at any time

Accrual basis accounting:

- record income when you earn it, even if payment comes later

- record expenses when you incur them, even if you pay later

- required for businesses with over $25 million in revenue

- gives a more accurate picture of profitability over time

Most small businesses start with cash basis because it's simpler. As your business grows or if you carry inventory, accrual accounting may give you better financial insights.

Talk to your accountant before choosing. Once you select a method, changing it requires Internal Revenue Service (IRS) approval.

Separate personal and business finances

Keeping personal and business finances separate protects you legally, simplifies taxes, and gives you a clear picture of business performance. Mixing accounts makes it nearly impossible to track true business costs or identify tax deductions.

Take these steps to separate your finances:

- open a dedicated business bank account: deposit all business income here and pay business expenses from this account only

- get a business credit card: use it exclusively for business purchases to simplify expense tracking

- pay yourself a regular salary: transfer a consistent amount to your personal account rather than dipping into business funds randomly

- keep receipts organized: store business receipts separately from personal ones for easier tax preparation

Separation also matters for legal protection. If your business is a Limited Liability Company (LLC) or corporation, mixing personal and business funds can pierce the corporate veil, making you personally liable for business debts.

Set up separate accounts from day one. Untangling mixed finances later is time-consuming and expensive.

Pay yourself consistently

Paying yourself a regular salary keeps your personal finances stable and your business finances clear. Many small business owners skip this step, pulling money randomly when they need it. This approach makes budgeting impossible and obscures true business profitability.

Choose a payment structure that fits your business type:

- salary: if your business is an S-corp or C-corp, pay yourself a reasonable salary with payroll taxes withheld

- owner's draw: if you're a sole proprietor or LLC, take regular draws from business profits

- combination: some owners take a base salary plus periodic draws when profits allow

Follow these steps to set your compensation:

- Calculate your minimum personal expenses

- Review your business's average monthly profit

- Set a salary or draw amount you can sustain in slow months

- Schedule regular payments to yourself, just like any other bill

- Adjust as revenue grows or circumstances change

Set aside money for self-employment taxes if you take owner's draws, as the IRS requires you to pay this tax if your net earnings from self-employment are $400 or more. Unlike W-2 employees, you're responsible for the full Social Security and Medicare contribution.

According to the IRS, the self-employment tax rate is 15.3%, which breaks down into 12.4% for social security and 2.9% for Medicare.

Use financial planning and forecasting

Financial planning is the process of mapping out how money flows through your business so you can make smarter decisions. A simple framework helps you allocate revenue intentionally.

One common model divides revenue like this:

- 50% on operating expenses: payroll, supplies, rent, and day-to-day costs

- 30% on business growth: equipment, hiring, marketing, and expansion

- 20% on future development: new products, services, or innovation

Different plans work for different businesses. Discuss options with your accountant to find what fits your situation.

Circumstances change, and your financial plan should change too. Conduct simple forecasting for at least the next six months. Estimate how much you'll sell and spend, then plug those numbers into your plan.

If the results don't work, adjust your plan. You can also use a budget to structure your plan and set realistic boundaries.

Be ambitious but stay realistic

Ambition drives business growth, but rational financial decisions keep your business alive. When you're your own boss, you can make any financial choice you want. Some will pay off. Others won't.

Learning to run a business means experimenting, succeeding, and occasionally failing. The key is making mistakes small enough to recover from financially.

Successful entrepreneurs share two traits: they learn from mistakes, and they limit the size of those mistakes. Few large businesses grew overnight. They built steadily, with setbacks along the way.

Taking calculated risks is part of good business. Taking unnecessarily big risks is not.

Chart your cash flow

Cash flow charting shows the money moving into and out of your business over time. Good accounting software creates visual charts of inflows (sales) and outflows (expenses) so you can spot patterns and problems.

Your inflows need to exceed outflows to make a profit. But the size of that difference matters most, and it varies over time. Few businesses make consistent profit every day. Some weeks are good, some aren't.

Review your charts regularly to identify patterns. Watch for these warning signs:

- small margins: the gap between income and expenses stays tight

- negative dips: outflows exceed inflows during certain periods

- seasonal patterns: predictable slowdowns at specific times of year

When you spot a problem period, find out what's causing it. Then restructure your operations to smooth out the dips.

Make minor adjustments to regulate cash flow

Keep three to six months of operating expenses in cash reserves. This buffer protects your business during slow periods without forcing dramatic changes.

If cash flow problems occur at predictable times, try these adjustments:

- negotiate supplier payment dates: align when you pay suppliers with when customers pay you

- shorten invoice payment terms: reduce terms by a day or two to speed up customer payments

- reduce sitting inventory: unsold stock ties up cash and costs you storage space

- establish a business credit line: access short-term funds when you need to bridge gaps

Manage your business debt

Business debt makes sense when borrowing costs less than the return your business generates from that money. Most businesses carry some debt, whether startup funding, equipment loans, or commercial mortgages.

Keep an eye on your borrowing costs, especially with variable rate loans. Rates can change for reasons buried in the fine print of your loan contract.

Review your debts regularly by taking these steps:

- compare repayment costs: calculate what you're actually paying in interest and fees

- assess your circumstances: determine if your situation has changed since you borrowed

- decide on adjustments: reduce debt if it's straining cash flow, or increase it if growth opportunities justify the cost

- shop around: ask your accountant about better borrowing options, since switching lenders can save money

Review expenses regularly

Regular expense reviews reveal where your money goes and whether you're staying profitable. Good accounting software generates the reports you need to track spending patterns.

Key financial reports to review include:

- profit and loss: shows income, expenses, and profits over a specific period

- balance sheet: shows assets, liabilities, and owner equity at a point in time

- cash flow statement: shows money moving into and out of your business

- accounts payable: shows what you owe to suppliers and vendors

- accounts receivable: shows what customers owe you

- depreciation: shows the declining value of business assets over time

Keep an eye on payroll too, even if you outsource it. For growing businesses, payroll complexity often exceeds expectations.

Review these reports regularly with your accountant or financial advisor. They can spot issues you might miss and suggest improvements.

Understand the true cost of money

Every dollar has a cost, whether you're receiving it or spending it. For example, high-earning self-employed individuals may be liable for an additional 0.9% Medicare Tax if their income exceeds certain thresholds set by the IRS. Understanding the true cost of money helps you maximize value on both sides of every transaction.

Consider these factors when evaluating costs:

- pay bills on time: avoid interest charges and protect your credit score

- evaluate payment methods: credit cards and PayPal charge fees that cut into margins, but convenience encourages customers to pay

- compare buying vs leasing: factor in hidden fees for maintenance, damage, and different tax implications

- learn tax and insurance rules:understanding regulations helps you avoid penalties and find savings

- consider bartering carefully: trading goods and services can reduce costs, but most countries treat barter as taxable income

Good accounting software breaks down your accounts in detail, showing the true cost of every payment into and out of your business.

Adjust your margins and get your pricing right

Profit margin is the difference between what you pay for something and what you sell it for. Understanding your margins helps you price products and services for maximum profitability.

Simple markup pricing is easy. A retailer might add 50% to cost, selling a $20 item for $30. But basic formulas often leave money on the table.

Price elasticity measures how sensitive customers are to price changes. At $50, you might sell 80 units per week. At $30, would you sell 300? At $60, would you sell 70? The answer depends on product demand, your location, marketing effectiveness, and competitor pricing.

Test different prices to find your optimal point:

- Set a test price for one to two weeks

- Track units sold at each price point

- Compare revenue and profit across price levels

- Factor in seasonal variation and overhead costs

- Adjust pricing based on results

With experimentation, you can fine-tune prices to maximize profit from everything you sell.

Chase the money you're owed

Collecting payments on time keeps cash flowing through your business. Late payments from customers are one of the most common causes of cash flow problems for small businesses.

Follow these steps to improve collections:

- track aging invoices: use accounting software to identify which customers take longest to pay

- set clear payment terms: state due dates prominently on every invoice to avoid confusion

- follow up consistently: chase late payers politely but persistently until they pay

- send invoices immediately: the sooner you invoice, the sooner you get paid

If you have many invoices to chase, consider invoice factoring. Factoring agencies buy your accounts receivable at a discount and guarantee payment within a set number of days.

Factoring trade-offs: agencies charge a percentage of invoice value, and some exclude bad debt collection. But for businesses with unpredictable cash flow, factoring can provide stability.

Five questions to ask before bidding for big contracts

Big contracts bring prestige but also risk. Before bidding on a large opportunity, evaluate whether your business can handle the demands without straining cash flow or neglecting existing clients.

Ask yourself these questions before you bid:

- staffing capacity: do you have the team to fulfill the contract, or will you need to hire?

- equipment funding: can you afford any new equipment the contract requires?

- client impact: will the new work cause you to neglect existing customers?

- contract end: what happens to your business when the contract ends or gets terminated early?

- payment timing: what happens if the new client takes months to pay?

Sometimes building a base of smaller clients is smarter than chasing one or two large ones. Diversified revenue means more predictable cash flow. If one contract ends suddenly, your business survives.

Know when to get accounting help

Hiring an accountant or bookkeeper makes sense when financial tasks consume too much time or exceed your expertise. Many business owners wait too long, only seeking help after problems arise.

Signs you need professional accounting help:

- time drain: you spend hours on bookkeeping instead of running your business

- growing complexity: multiple revenue streams, employees, or inventory make tracking difficult

- tax confusion: you're unsure about deductions, quarterly payments, or compliance requirements

- cash flow problems: you can't figure out why money is tight despite steady sales

- growth plans: you're seeking loans, investors, or preparing to scale

Types of accounting professionals:

- bookkeeper: handles day-to-day transaction recording and reconciliation

- accountant: prepares financial statements, provides analysis, and advises on business decisions

- CPA (Certified Public Accountant): offers all accounting services plus tax preparation and audit representation

- fractional CFO (Chief Financial Officer): provides part-time strategic financial leadership for growing businesses

Start with a bookkeeper if you just need help with daily tasks. Hire an accountant or CPA when you need strategic advice or tax expertise. Many small businesses use accounting software like Xero for daily tasks and consult an accountant quarterly or at tax time.

Put financial management at the heart of your business

Financial management belongs at the center of your business strategy, not as an afterthought. Understanding the numbers that drive your business gives you the knowledge to keep it running and grow when the time is right.

Good accounting software makes it easier to plan, forecast, track cash flow, and collect payments. But the software is just a tool. Only you can steer your business in the right direction.

Xero gives you real-time visibility into your finances so you can make confident decisions. Try Xero free for one month and see how the right tools can transform your financial management.

FAQs on managing business finances

Here are answers to common questions about managing your business finances.

What's the difference between cash and accrual accounting?

Cash accounting records income when you receive payment and expenses when you pay them. Accrual accounting records income when earned and expenses when incurred, regardless of when money changes hands. Most small businesses use cash accounting for simplicity.

How much should I set aside for business taxes?

Set aside 25% to 30% of your net profit for federal and state taxes. If you're self-employed, include an additional 15.3% for self-employment tax. Adjust based on your tax bracket and state requirements.

Do I really need a separate bank account for my business?

Yes. Separate accounts simplify expense tracking, make tax preparation easier, and protect your personal assets if your business is sued. Open a dedicated business account before you make your first sale.

What's the 70/20/10 budget rule for businesses?

The 70/20/10 rule allocates 70% of revenue to operating expenses, 20% to savings or debt repayment, and 10% to owner compensation or growth investments. Adjust percentages based on your industry and growth stage.

When should I hire an accountant or bookkeeper?

Hire help when bookkeeping takes more than a few hours weekly, your taxes become complex, or you're making financial decisions that need expert guidance. Many businesses start with software like Xero and add professional support as they grow.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Get one month free

Sign up to any Xero plan, and we will give you the first month free.