2026 Tax brackets for small businesses

See this year’s federal tax brackets, standard deduction, and steps for estimating your tax bill as a small business owner.

Written by Kari Brummond—Content Writer, Accountant, IRS Enrolled Agent. Read Kari's full bio

Published Friday 24 July 2026

Table of contents

Key takeaways

- Pass-through (sole props, partnerships, and S-corp) profits flow to your personal tax return, and you pay tax accordingly. C-corporations pay tax at the company level, but owners/shareholders are only taxed when they receive dividends or sell their shares.

- Sole props and partnerships pay self-employment tax on all profits, but the rules are more complicated with S- and C-corporations.

- To determine your taxable income, you subtract deductions from total income on your individual tax return. Then, the tax rate depends on the tax brackets that apply to you.

- Tax brackets and the standard deduction change each year, as do tax credits and other deductions. Be aware of how changes may affect your tax liability.

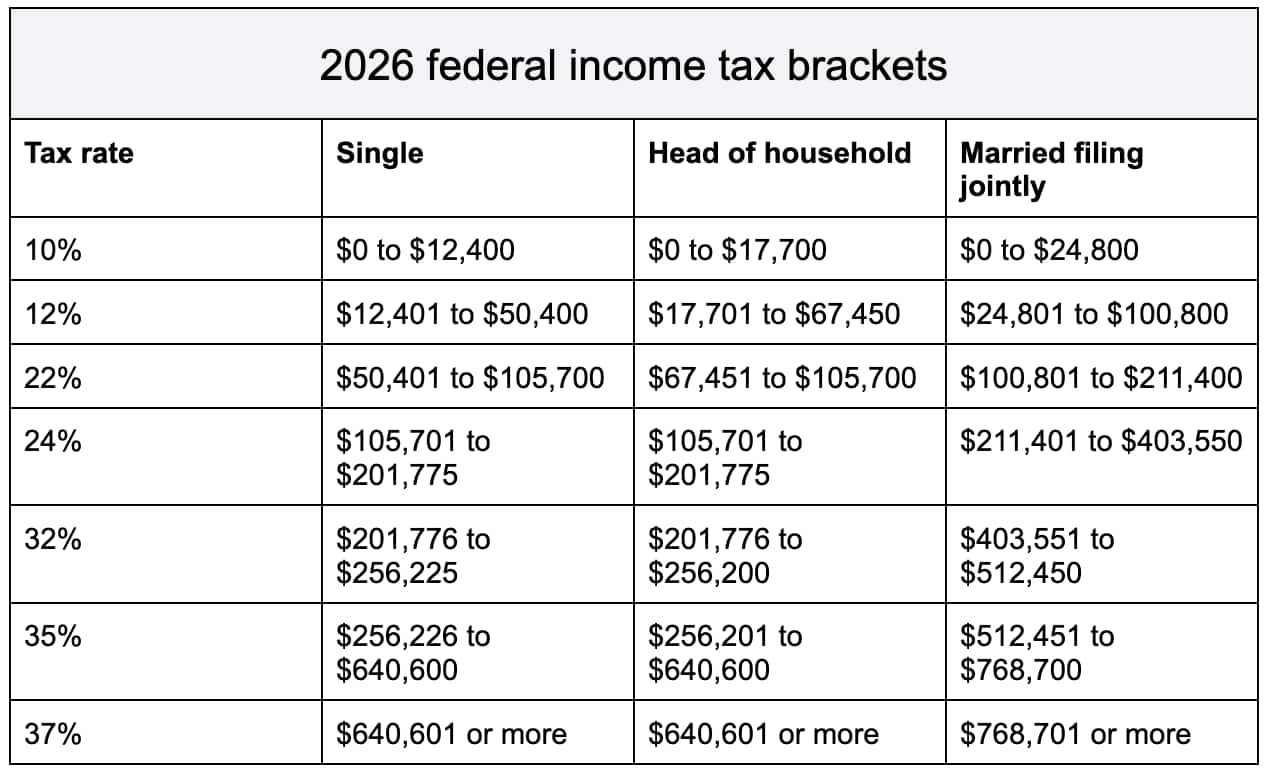

Federal income tax brackets

Federal tax brackets show which income tax rate applies to you based on your taxable income and filing status. These brackets apply to everyone who files a U.S. individual income tax return, but small business owners and investors must also understand how self-employment tax and capital gains tax affect their total tax liability. The IRS uses a progressive income tax system, which means rates increase as your income gets higher. The agency also adjusts income tax brackets annually based on inflation, and new tax legislation often adjusts brackets and rates as well.

Here are the 2026 tax brackets:

These rates apply to your taxable income – that's your income after deductions. If you have long-term capital gains, they may be taxed at a lower rate (see below).

Learn more about 2026 tax brackets and tax changes from the IRS.

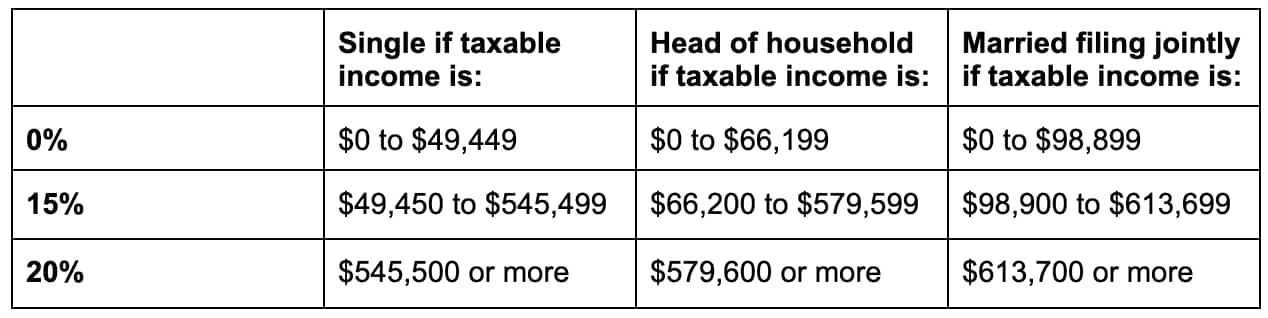

Capital gains tax brackets

Short-term capital gains are taxed based on your income tax bracket and apply to assets sold in under a year. Long-term capital gains are taxed at a lower rate and come from the sale of assets held over a year.

The rate depends on your taxable income. Here are the 2026 capital gains tax brackets:

Be aware that capital gains tax brackets work differently from income tax brackets. With income tax, taxable income is taxed progressively – income in each bracket is taxed at that bracket’s rate (10%, 12%, 22%, etc.), so most taxpayers pay multiple marginal rates. Long-term capital gains use three rates – 0%, 15%, or 20% – based on your total taxable income. Capital gains are stacked on top of your other income, and different portions of the gain may fall into different capital gains brackets.

For example, if you are single and your taxable income (including long-term capital gains) is $48,000, your long-term capital gains would likely fall in the 0% bracket. However, if you're single and your taxable income (including capital gains) is $100,000, your long-term capital gains would generally fall in the 15% bracket, though very large gains could push a portion into the 20% bracket.

Both the 2026 federal income tax brackets and capital gains rate apply to your taxable income. Again, that's your income after deductions. IRS Topic 409 explains more about capital gains and losses.

What is the standard deduction amount?

Every taxpayer who files a tax return gets to claim a standard or itemized deduction – you deduct that amount from your income to determine your taxable income.

The 2026 standard deduction amount, based on filing status, is:

- single: $16,100

- head of household: $24,150

- married filing jointly: $32,200

You get a slightly higher standard deduction if you're either over age 65 or blind – and a double increase if both of these apply to you.

Alternatively, you may itemize deductions, which is when you add up a variety of deductible personal expenses and deduct that total from your income instead of the standard deduction. Only about 10% of taxpayers itemize, and typically only if their itemized deductions exceed the standard amount.

Itemized deductions include mortgage interest, state and local taxes (SALT), and medical expenses. These deductions are subject to limits or thresholds – for example, you can only itemize medical expenses over a certain threshold and only claim up to $40,000 as a SALT deduction (temporarily for 2025-2029 for joint filers).

In addition, taxpayers can also claim certain above-the-line deductions (deductions you take before calculating your Adjusted Gross Income) on top of their standard or itemized deduction. These include certain retirement account contributions and interest on student loans (subject to income limits).

How federal tax brackets work for different types of small businesses

Tax brackets show the income tax rate that applies to your taxable income, but small business owners also need to deal with self-employment tax or corporate income tax.

Here's a breakdown of how federal tax brackets affect you based on your business structure:

Sole proprietorships and partnerships

Sole props report their profits directly on their individual income tax return (Schedule C), while partnerships file a partnership return (Form 1065) and then issue a Schedule K-1 showing each partner's share of profits, losses, and deductions.

Here's what happens on the owner's individual tax return in both cases:

- Self-employment tax generally applies to business profits.

- Business profit is combined with other income to calculate total income.

- Above-the-line deductions (including 50% of self-employment tax) reduce adjusted gross income. Then standard or itemized deductions reduce taxable income.

- Income tax is calculated according to the total taxable income and the applicable tax bracket for the year.

- Tax credits are used to reduce tax liability – including business tax credits, such as the qualified business income (QBI) credit, and personal credits like the child tax credit.

To learn more, check out this IRS resource on self-employment tax.

S-corporations

The S-corp files an S-corp return and issues 1099-Ks reporting profits to all owners or shareholders. The S-corp reports the following as expenses on its business tax return:

- wages paid to owners

- employer payroll taxes based on those wages

It also issues W-2s to any owner/shareholders who work in the company.

To report your S-corp income, take these steps:

- Add the income from the 1099-K and the W-2 to income from all other sources on the individual income tax return.

- Subtract the standard or itemized deduction, as well as any other deductions, to determine the taxable income.

- Calculate the tax liability based on the taxable income and the current federal tax brackets.

- Use individual tax credits, if available, to reduce the S-corp’s tax liability.

S-corp owners don't pay self-employment tax. Instead, the business withholds Social Security and Medicare tax from the owner-employee’s pay, and then the business makes a matching payment.

C-corporations

C-corps file a corporate income tax return, and they pay tax at the entity level on their profits. The 2026 corporate tax rate is 21%. For example, if a corporation has $100,000 in profits, it will owe $21,000 in corporate income tax. However, there are all kinds of business deductions and tax credits to help lower the effective rate.

Corporations claim wages paid to owners/shareholders as business expenses, and then issue W-2s to those individuals. If a C-corp issues dividends to owners or shareholders, it cannot claim a deduction for the dividends, and it reports the payments to those individuals using 1099-DIV forms.

Owners/shareholders who receive W-2s or 1099-DIVs need to report those as income on their tax returns, and then pay tax according to their other income, deductions, and credits.

If you file taxes for an LLC, the process varies depending on whether you're taxed as a sole prop, partnership, or corporation.

Learn more from the IRS about business structures and taxation.

What has changed for small businesses this year

The One Big Beautiful Bill (OBBB) brought in several new tax laws for 2026, including some that were retroactive to tax year 2025. Here are some of the main changes that may change your effective small business tax rate in 2026.

- QBI deduction made permanent: the pass-through business income deduction in 2026 is worth 20% of qualified business income, subject to certain rules and limitations

- 100% bonus depreciation made permanent: allows businesses to claim 100% of qualifying capital assets, rather than depreciating them over time

- Increased limits for Section 179 deductions: an increased maximum deduction (to $2.5 million) and a raised phase-out threshold (to $4.09 million)

- Research and development (R&D) expenses: can now be deducted in the year expenses are incurred, rather than depreciated – and qualifying businesses can make retroactive changes (amend previously filed returns)

- Standard mileage rate: increased to 72.5 cents per mile, up from 70 cents per mile in 2025

The QBI deduction and bonus depreciation started in 2018 and were scheduled to end in 2025, but were made a permanent part of the tax code in 2025 instead.

How to estimate your tax bill

If your earnings are similar to last year's, use last year's tax liability to estimate your tax bill this year – a good way to determine your quarterly estimated payments. But be careful: changes to tax brackets, the tax code, or your personal situation can change your current year tax liability.

If you own a sole prop or partnership, here’s how you can estimate your tax liability:

- Multiply your anticipated profits by 15.3% (the self-employment tax rate 2026).

- Add up all of your income and subtract the 2026 standard deduction amount.

- Find the 2026 tax brackets that apply to your situation, and calculate your tax.

Keep in mind this doesn't include tax credits or deductions.

You could use an income tax calculator to help you, and it’s always good to ask an accountant to help figure out how to calculate estimated taxes in 2026. They might also be able to lower your taxes by helping you with your small business tax planning.

Make tax time easy with Xero

Xero makes sure you have accurate numbers to report your business income and expenses. That makes tax time as easy as possible – you can focus on maximizing tax credits and deductions, not catching up on bookkeeping or gathering financial records at the last minute.

FAQs on tax brackets

Check out these questions and answers to learn more:

What tax bracket will I be in?

Your tax bracket varies based on your income. You may be in multiple brackets. For example, if you file as head of household and you have $100,000 in taxable income, the first $17,700 is taxed at 10%, the next $49,750 at 12%, and the remaining $32,550 at 22%.

Do tax brackets change this year?

Tax brackets change annually based on inflation, and also update based on new tax legislation. The One Big Beautiful Bill Act, passed in 2025, increased 2026 tax brackets beyond their usual inflationary adjustment.

What is the self-employment tax rate?

The self-employment tax rate in 2026 is 15.3%. That's 12.4% for Social Security taxes and 2.9% for Medicare taxes.

Are there different tax brackets within each state?

Yes, states have different income tax brackets for individual tax payers according to their income. They also have different rules for businesses – even if your business doesn't have to pay federal tax on the entity level, it may still pay business tax to the state. For example, although S-corps don't pay business taxes to the IRS on the entity level, they may face franchise tax, gross receipts tax, or other business-level taxes in their state.

Where can I find official IRS numbers?

The IRS website is the best place to find up-to-date numbers on tax brackets, small business tax rates, and new tax laws. You can also ask an experienced tax preparer for help.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Get one month free

Sign up to any Xero plan, and we will give you the first month free.