Solvency meaning: definition, ratios and liquidity

Learn what solvency means, how it differs from liquidity, and what both tell you about your business.

Written by Lena Hanna—Trusted CPA Guidance on Accounting and Tax. Read Lena's full bio

Published Monday 20 April 2026

Table of contents

Key takeaways

- Recognize that solvency and liquidity measure different things: solvency checks whether your total assets exceed total liabilities over the long term, while liquidity checks whether you can pay bills in the coming months.

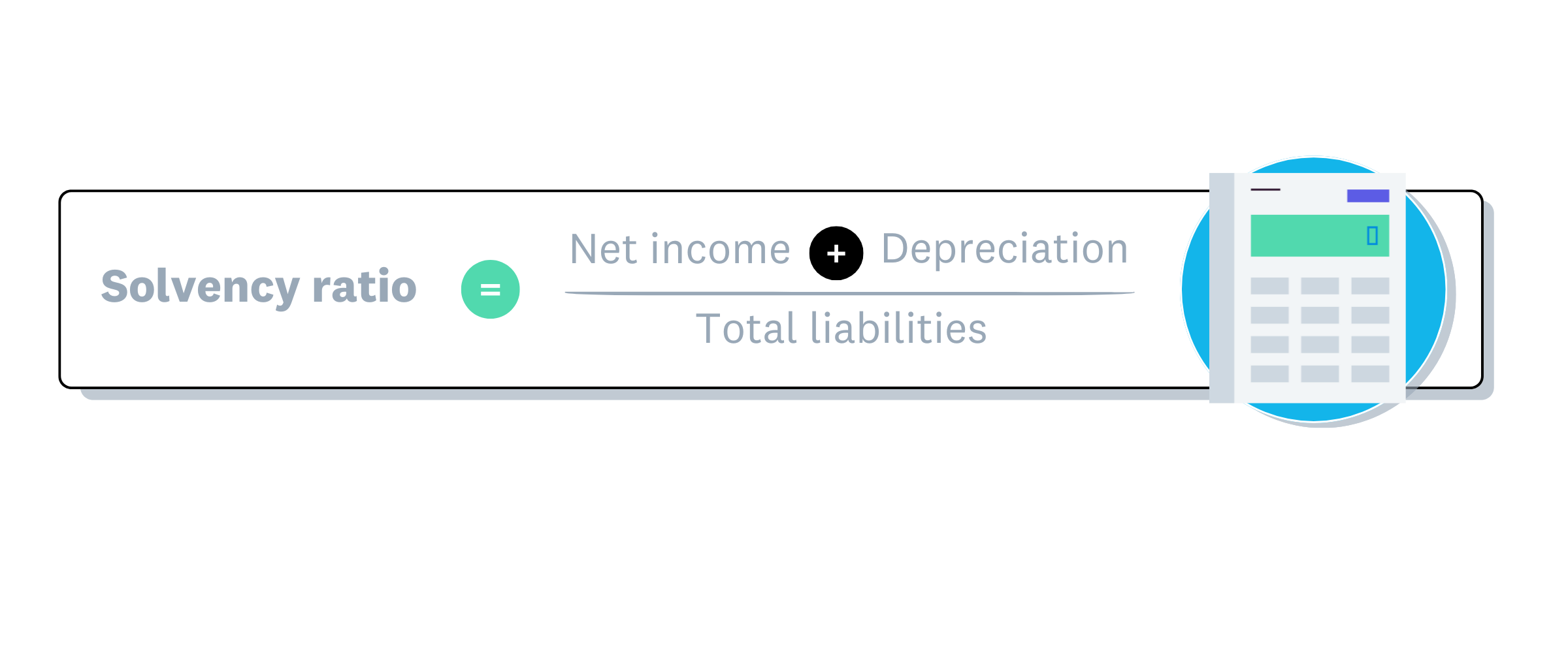

- Calculate your solvency ratio regularly by adding net income and depreciation, then dividing by total liabilities — a result above 20% generally signals good financial health, though this varies by industry.

- Monitor your liquidity using the current ratio, quick ratio, and cash ratio each month so you can spot cash flow problems early and keep daily operations running smoothly.

- Avoid taking on new debt without paying down existing loans, as this can push total liabilities above total assets and create insolvency risk even when your business looks profitable.

What does solvency mean in business?

Solvency is your business's ability to meet long-term financial commitments, ensuring you maintain adequate financial resources so liabilities can be met as they fall due. A solvent business has total assets that exceed total liabilities, which means it maintains positive net equity.

A solvent business typically shares these characteristics:

- Assets exceed liabilities: your business owns more than it owes

- Long-term stability: can pay debts over months and years

- Positive equity: maintains a financial cushion for unexpected challenges

Steps to maintain solvency

Follow these steps to keep your business solvent:

- Stay profitable: generate consistent profits to keep total assets exceeding total liabilities

- Manage debt strategically: negotiate lower repayments and understand collateral loan terms if payments become difficult

- Optimise asset use: ensure your inventory and equipment generate enough returns to cover debt obligations

What is solvency vs profitability?

Solvency measures whether your assets exceed your liabilities, while profitability measures whether your revenue exceeds your costs. A business can be profitable but still become insolvent if it takes on too much debt.

Profitable businesses generally have better solvency because profits build assets. However, taking new loans without paying existing ones can push total liabilities above assets. This creates insolvency risk even when profits look healthy. Most accountants agree that financial risk becomes too high when the proportion of debt exceeds equity.

Read more in the guide on profitability.

How does solvency affect your business growth?

Staying solvent opens doors for your business:

- Access credit: borrow from banks and lenders who feel confident you can repay

- Attract investors: bring in resources and expertise to accelerate growth

- Negotiate better terms: use cash reserves to buy in bulk and lower your cost per unit

- Plan ahead: keep operations running smoothly while building for the future

What does liquidity mean in business?

Liquidity measures your business's ability to pay bills and loan repayments in the coming months. It compares current assets against current liabilities.

Understanding the key components helps you assess your liquidity position:

- Current liabilities: amounts owed within the coming year

- Current assets: cash, inventory, payments due, and quickly sellable assets

- Common ratios: cash ratio, quick ratio, and current ratio

Other liquidity ratios

Small businesses typically use three ratios to measure liquidity:

- Current ratio: compares all current assets to current liabilities (while a safe ratio should ideally exceed 2:1, acceptable levels vary widely by industry)

- Quick ratio (acid test): uses only assets convertible to cash within three months

- Cash ratio: compares only cash and cash equivalents to current liabilities

How liquid are your assets?

Different assets convert to cash at different speeds. Here's how common business assets rank from most to least liquid:

- Cash: physical currency and immediately withdrawable savings convert instantly

- Accounts receivable:invoices owed to you convert within payment terms

- Physical assets:buildings and equipment can take months to sell

Table of the difference between solvency and liquidity

Table of the difference between solvency and liquidity

Liquidity vs other financial concepts

Liquidity often gets confused with related financial concepts. Here's how they differ:

- Liquidity: how easily you can cover upcoming costs

- Cash flow: the movement of cash in and out of your business

- Working capital: money remaining after covering upcoming costs

- Free cash flow: cash remaining after capital investments

Why solvency and liquidity matter for your small business

Solvency ratio formula

Understanding both solvency and liquidity helps you make better financial decisions.

Solvency supports your long-term position:

- Financial stability: manage risks like unpaid invoices

- Growth capacity: use resources for expansion

- Stakeholder confidence: keep shareholders satisfied

Liquidity keeps daily operations running:

- Operational continuity: pay staff and suppliers on time

- Risk protection: handle unexpected costs and market changes

- Cash availability: maintain funds for daily operations

Poor financial health creates serious risks:

- Poor liquidity: struggle to pay immediate obligations

- Poor solvency: difficulty meeting long-term debts

- Insolvency: cannot meet debts and may face formal insolvency procedures

In late 2023, reports showed more than 47,000 UK companies in critical financial distress. Monitoring your position early helps you avoid joining them.

For more detail, read the UK government guidance on liquidation and insolvency.

The main differences between solvency and liquidity

Solvency focuses on long-term financial health, while liquidity focuses on short-term cash availability. Both metrics matter, but they measure different things.

Key differences between solvency and liquidity:

- Time horizon: solvency looks at years ahead; liquidity looks at months ahead

- What's measured: solvency compares total assets to total liabilities; liquidity compares current assets to current liabilities

- Primary concern: solvency asks "can you survive long-term?"; liquidity asks "can you pay bills this month?"

Monitor both regularly to understand your complete financial picture.

How to measure solvency and liquidity in your business

Calculating your solvency and liquidity ratios helps you understand your financial position. Here's how to work out each one.

Solvency ratio formula

Solvency ratio formula

Here's how the solvency ratio works in practice.

Martha owns a cafe with these figures:

- net income of £50,000

- depreciation of £10,000

- total liabilities of £150,000

Her solvency ratio is: (£50,000 + £10,000) ÷ £150,000 = 0.4 or 40%

This means Martha can cover 40% of her total liabilities with one year's earnings. A ratio above 20% generally indicates good solvency, though this varies by industry.

Liquidity ratio formulas

The three main liquidity ratios help you assess short-term financial health:

Current ratio: Current assets ÷ current liabilities

Quick ratio: (Current assets - inventory) ÷ current liabilities

Cash ratio: Cash and cash equivalents ÷ current liabilities

A current ratio of 2:1 or higher usually indicates strong liquidity, but acceptable levels vary by industry.

FAQs on solvency and liquidity

Here are answers to common questions about solvency and liquidity.

Can a business be solvent but not liquid?

Yes. A business can have assets that exceed liabilities (solvent) but lack immediate cash to pay current bills (illiquid). This often happens when assets are tied up in property, equipment, or slow-paying customers.

What's a good solvency ratio?

A solvency ratio above 20% is generally considered healthy, but this varies by industry. Capital-intensive businesses may have lower ratios, while service businesses typically have higher ratios.

How can I improve my liquidity?

You can improve liquidity by collecting payments faster, negotiating longer payment terms with suppliers, reducing inventory levels, and maintaining a cash reserve for emergencies.

What causes insolvency?

Insolvency occurs when liabilities exceed assets or when you can't pay debts as they fall due. Common causes include taking on too much debt, sustained losses, poor cash flow management, and unexpected market changes.

How often should I check my solvency and liquidity?

Check your liquidity ratios monthly to ensure you can meet short-term obligations. Review solvency ratios quarterly or annually as part of your strategic planning and financial health assessment.

Published Monday 20 April 2026

Table of contents

Key takeaways

- Recognize that solvency and liquidity measure different things: solvency checks whether your total assets exceed total liabilities over the long term, while liquidity checks whether you can pay bills in the coming months.

- Calculate your solvency ratio regularly by adding net income and depreciation, then dividing by total liabilities — a result above 20% generally signals good financial health, though this varies by industry.

- Monitor your liquidity using the current ratio, quick ratio, and cash ratio each month so you can spot cash flow problems early and keep daily operations running smoothly.

- Avoid taking on new debt without paying down existing loans, as this can push total liabilities above total assets and create insolvency risk even when your business looks profitable.

What does solvency mean in business?

Solvency is your business's ability to meet long-term financial commitments, ensuring you maintain adequate financial resources so liabilities can be met as they fall due. A solvent business has total assets that exceed total liabilities, which means it maintains positive net equity.

A solvent business typically shares these characteristics:

- Assets exceed liabilities: your business owns more than it owes

- Long-term stability: can pay debts over months and years

- Positive equity: maintains a financial cushion for unexpected challenges

Steps to maintain solvency

Follow these steps to keep your business solvent:

- Stay profitable: generate consistent profits to keep total assets exceeding total liabilities

- Manage debt strategically: negotiate lower repayments and understand collateral loan terms if payments become difficult

- Optimise asset use: ensure your inventory and equipment generate enough returns to cover debt obligations

What is solvency vs profitability?

Solvency measures whether your assets exceed your liabilities, while profitability measures whether your revenue exceeds your costs. A business can be profitable but still become insolvent if it takes on too much debt.

Profitable businesses generally have better solvency because profits build assets. However, taking new loans without paying existing ones can push total liabilities above assets. This creates insolvency risk even when profits look healthy. Most accountants agree that financial risk becomes too high when the proportion of debt exceeds equity.

Read more in the guide on profitability.

How does solvency affect your business growth?

Staying solvent opens doors for your business:

- Access credit: borrow from banks and lenders who feel confident you can repay

- Attract investors: bring in resources and expertise to accelerate growth

- Negotiate better terms: use cash reserves to buy in bulk and lower your cost per unit

- Plan ahead: keep operations running smoothly while building for the future

What does liquidity mean in business?

Liquidity measures your business's ability to pay bills and loan repayments in the coming months. It compares current assets against current liabilities.

Understanding the key components helps you assess your liquidity position:

- Current liabilities: amounts owed within the coming year

- Current assets: cash, inventory, payments due, and quickly sellable assets

- Common ratios: cash ratio, quick ratio, and current ratio

Other liquidity ratios

Small businesses typically use three ratios to measure liquidity:

- Current ratio: compares all current assets to current liabilities (while a safe ratio should ideally exceed 2:1, acceptable levels vary widely by industry)

- Quick ratio (acid test): uses only assets convertible to cash within three months

- Cash ratio: compares only cash and cash equivalents to current liabilities

How liquid are your assets?

Different assets convert to cash at different speeds. Here's how common business assets rank from most to least liquid:

- Cash: physical currency and immediately withdrawable savings convert instantly

- Accounts receivable:invoices owed to you convert within payment terms

- Physical assets:buildings and equipment can take months to sell

Table of the difference between solvency and liquidity

Table of the difference between solvency and liquidity

Liquidity vs other financial concepts

Liquidity often gets confused with related financial concepts. Here's how they differ:

- Liquidity: how easily you can cover upcoming costs

- Cash flow: the movement of cash in and out of your business

- Working capital: money remaining after covering upcoming costs

- Free cash flow: cash remaining after capital investments

Why solvency and liquidity matter for your small business

Solvency ratio formula

Understanding both solvency and liquidity helps you make better financial decisions.

Solvency supports your long-term position:

- Financial stability: manage risks like unpaid invoices

- Growth capacity: use resources for expansion

- Stakeholder confidence: keep shareholders satisfied

Liquidity keeps daily operations running:

- Operational continuity: pay staff and suppliers on time

- Risk protection: handle unexpected costs and market changes

- Cash availability: maintain funds for daily operations

Poor financial health creates serious risks:

- Poor liquidity: struggle to pay immediate obligations

- Poor solvency: difficulty meeting long-term debts

- Insolvency: cannot meet debts and may face formal insolvency procedures

In late 2023, reports showed more than 47,000 UK companies in critical financial distress. Monitoring your position early helps you avoid joining them.

For more detail, read the UK government guidance on liquidation and insolvency.

The main differences between solvency and liquidity

Solvency focuses on long-term financial health, while liquidity focuses on short-term cash availability. Both metrics matter, but they measure different things.

Key differences between solvency and liquidity:

- Time horizon: solvency looks at years ahead; liquidity looks at months ahead

- What's measured: solvency compares total assets to total liabilities; liquidity compares current assets to current liabilities

- Primary concern: solvency asks "can you survive long-term?"; liquidity asks "can you pay bills this month?"

Monitor both regularly to understand your complete financial picture.

How to measure solvency and liquidity in your business

Calculating your solvency and liquidity ratios helps you understand your financial position. Here's how to work out each one.

Solvency ratio formula

Solvency ratio formula

Here's how the solvency ratio works in practice.

Martha owns a cafe with these figures:

- net income of £50,000

- depreciation of £10,000

- total liabilities of £150,000

Her solvency ratio is: (£50,000 + £10,000) ÷ £150,000 = 0.4 or 40%

This means Martha can cover 40% of her total liabilities with one year's earnings. A ratio above 20% generally indicates good solvency, though this varies by industry.

Liquidity ratio formulas

The three main liquidity ratios help you assess short-term financial health:

Current ratio: Current assets ÷ current liabilities

Quick ratio: (Current assets - inventory) ÷ current liabilities

Cash ratio: Cash and cash equivalents ÷ current liabilities

A current ratio of 2:1 or higher usually indicates strong liquidity, but acceptable levels vary by industry.

FAQs on solvency and liquidity

Here are answers to common questions about solvency and liquidity.

Can a business be solvent but not liquid?

Yes. A business can have assets that exceed liabilities (solvent) but lack immediate cash to pay current bills (illiquid). This often happens when assets are tied up in property, equipment, or slow-paying customers.

What's a good solvency ratio?

A solvency ratio above 20% is generally considered healthy, but this varies by industry. Capital-intensive businesses may have lower ratios, while service businesses typically have higher ratios.

How can I improve my liquidity?

You can improve liquidity by collecting payments faster, negotiating longer payment terms with suppliers, reducing inventory levels, and maintaining a cash reserve for emergencies.

What causes insolvency?

Insolvency occurs when liabilities exceed assets or when you can't pay debts as they fall due. Common causes include taking on too much debt, sustained losses, poor cash flow management, and unexpected market changes.

How often should I check my solvency and liquidity?

Check your liquidity ratios monthly to ensure you can meet short-term obligations. Review solvency ratios quarterly or annually as part of your strategic planning and financial health assessment.

Get one month free

Purchase any Xero plan, and we will give you the first month free.