S corp vs LLC: key differences, tax benefits, and how to choose

A practical framework for advising clients on S corp vs LLC entity selection.

Written by Joshua Poh—B2B Fintech Writer and Small Business Owner. Read Joshua's full bio

Published Sunday 14 June 2026

Table of contents

Key takeaways

- S corp tax savings typically begin at $60,000+ in annual profit. Advise clients earning above this threshold to consider S corp election.

- S corps require board meetings, annual reports, and strict IRS record-keeping, which increases compliance workload for your practice.

- S corps limit ownership to 100 US-based individual shareholders. Verify client eligibility before recommending S corp election.

- Position entity selection as a strategic advisory conversation that strengthens client relationships and creates recurring compliance revenue.

S corp vs LLC: what your clients need to know

"Should I be an S corp or an LLC?" is one of the most common questions you'll hear from small business clients. It's also one of the highest-value advisory conversations you can have. Getting entity selection right affects your client's tax burden, compliance obligations, and long-term growth options.

Entity selection is more than a one-time decision. It's an entry point for broader advisory engagements, including tax planning, cash flow forecasting, and succession planning. When you guide a client through the S corp vs LLC analysis, you demonstrate the kind of strategic thinking that turns a transactional relationship into a long-term advisory partnership.

This guide provides a practical framework you can apply across your client base. It covers the tax differences, structural requirements, conversion process, and practice workflow implications so you can advise clients confidently and manage the resulting compliance work efficiently.

How S corp and LLC tax treatment differs

The core tax difference between S corps and LLCs is how self-employment taxes apply. Both structures use pass-through taxation, meaning business profits flow to owners' personal tax returns without corporate-level tax.

With an LLC, all profits are subject to the 15.3% self-employment tax (12.4% Social Security plus 2.9% Medicare). With an S corp, the owner pays themselves a reasonable salary, which is subject to payroll taxes, and then takes remaining profits as distributions that aren't subject to self-employment tax.

That salary-plus-distribution structure is where the tax savings come from.

Self-employment tax savings by profit level

The following examples illustrate how S corp tax savings scale with profit levels. Each assumes a reasonable salary determination based on industry norms.

- $75,000 profit: LLC self-employment tax of approximately $10,598 vs S corp of approximately $6,885 (salary of $45,000). That's roughly $3,713 in annual savings.

- $150,000 profit: LLC self-employment tax of approximately $21,195 vs S corp of approximately $10,710 (salary of $70,000). That's roughly $10,485 in annual savings.

- $250,000 profit: LLC self-employment tax of approximately $28,522 vs S corp of approximately $13,770 (salary of $90,000). That's roughly $14,752 in annual savings.

These are illustrative. Actual figures depend on the specific salary determination and applicable rates. Note that the Social Security portion of self-employment tax applies only to the first $176,100 of earnings (2025 figure).

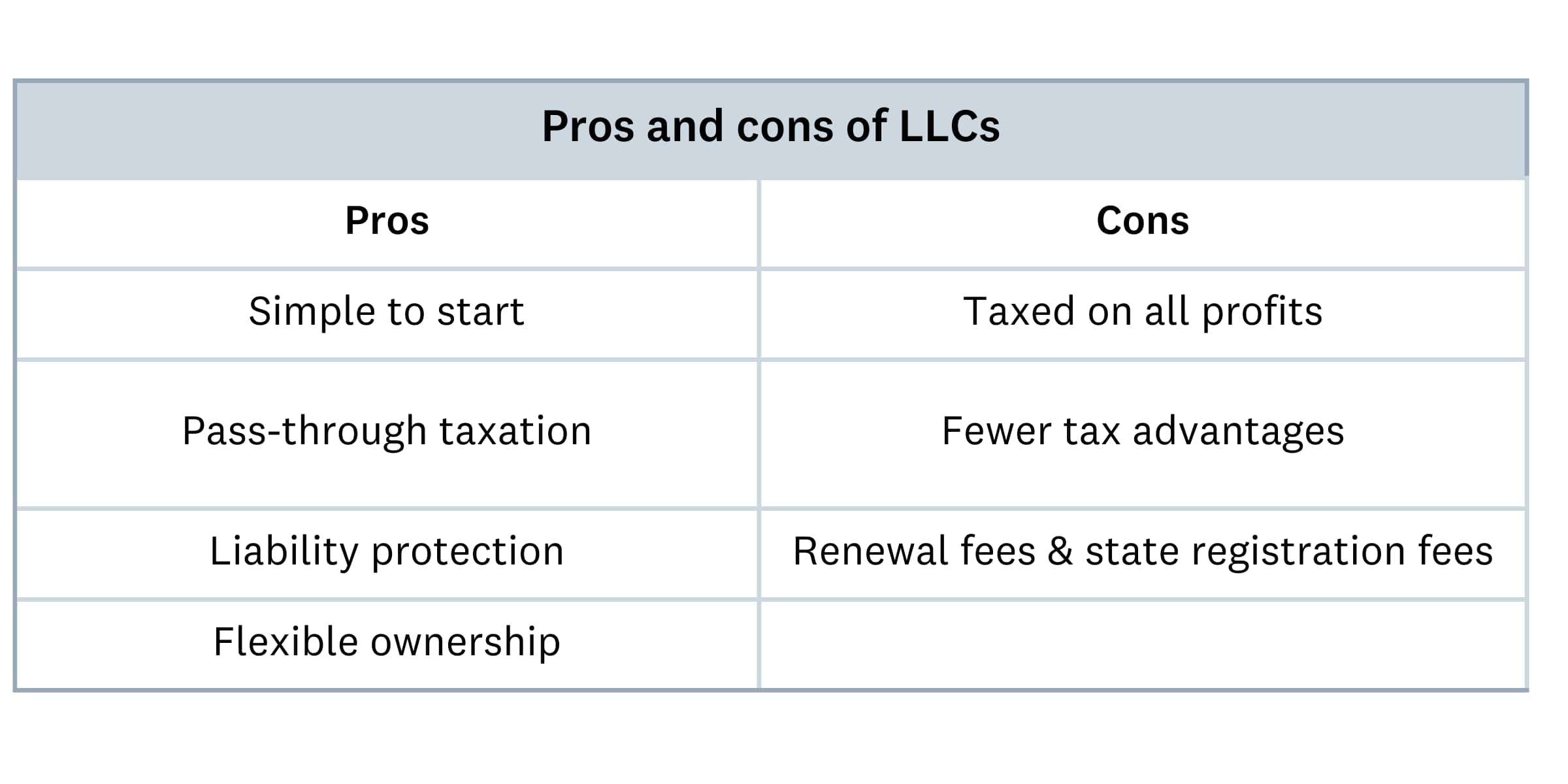

Key structural differences between S corps and LLCs

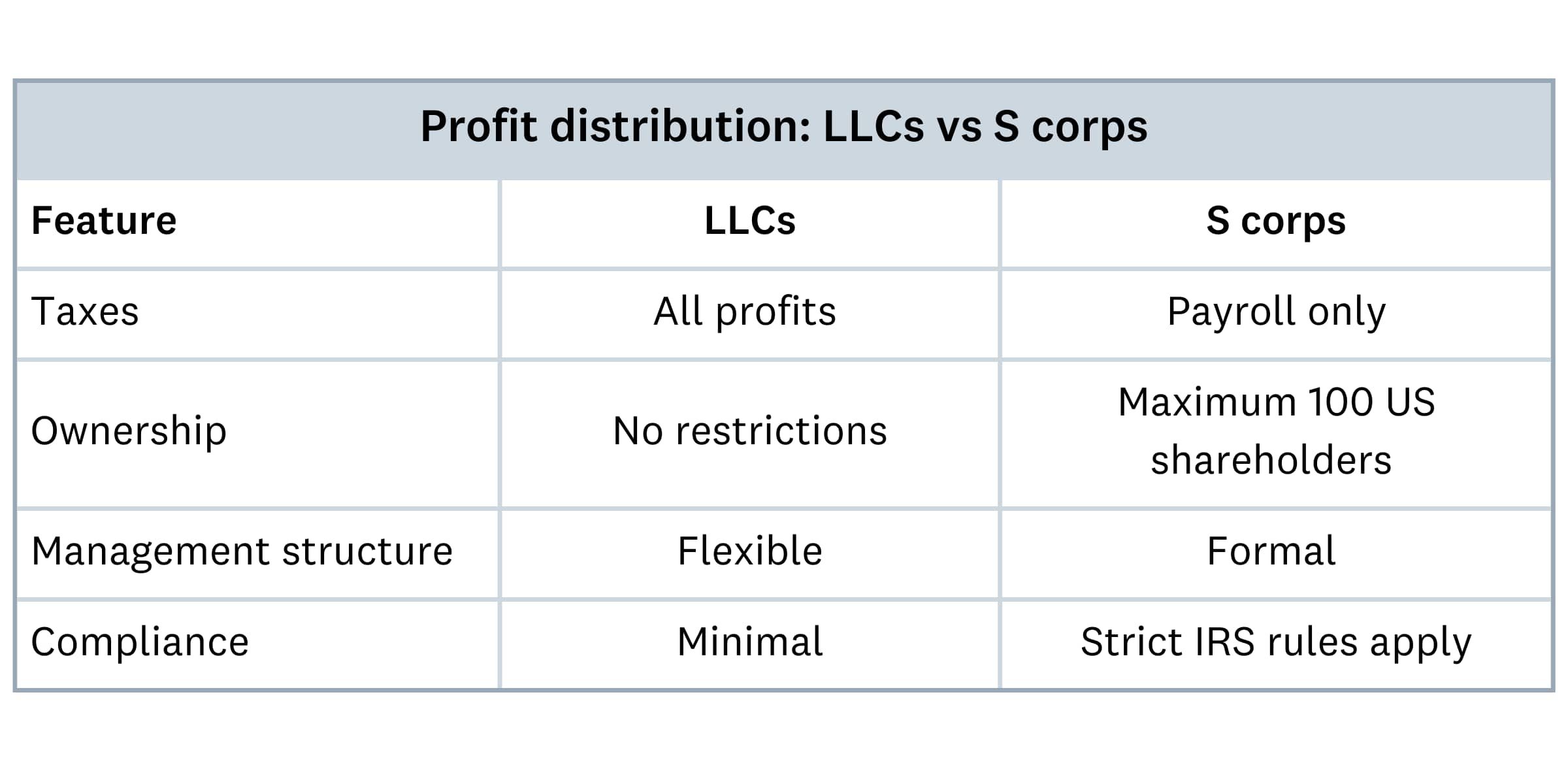

Beyond tax treatment, S corps and LLCs differ in ownership rules, management requirements, and profit distribution. Understanding these differences helps you set accurate expectations with clients before they make an election.

Ownership rules and restrictions

Before recommending S corp election, verify these eligibility requirements with your client:

- Shareholder limit: S corps can have no more than 100 shareholders

- Citizenship requirement: All shareholders must be US citizens or resident aliens

- Entity restrictions: Shareholders must be individuals, certain trusts, or estates. Partnerships, corporations, and nonresident entities can't hold S corp shares.

- Single stock class: S corps can only issue one class of stock

LLCs have none of these restrictions. They can have unlimited members, including foreign entities, corporations, and other LLCs. If your client plans to raise capital from foreign investors or institutional sources, an LLC structure preserves that flexibility.

Management and compliance requirements

LLCs operate with minimal formality. Members can manage the business directly or appoint a manager, and there's no requirement for board meetings or corporate minutes.

S corps follow a stricter corporate governance structure. They must:

- Appoint and maintain a board of directors

- Hold annual director and shareholder meetings

- Keep detailed corporate minutes and records

- File annual reports with the state

- Maintain ongoing compliance with both IRS and state requirements

From a practice perspective, these requirements generate billable work. Corporate minutes, annual meeting documentation, and compliance monitoring are recurring engagements you can build into your service packages.

Profit distribution rules

LLCs can distribute profits in any proportion regardless of ownership percentage. An owner with 20% equity can receive 80% of distributions if the operating agreement allows it.

S corps must distribute profits strictly in proportion to ownership. A 50% shareholder receives 50% of distributions.

The bigger advisory challenge is determining the reasonable salary split. The IRS expects S corp owners to pay themselves a reasonable salary before taking distributions, and the IRS has the authority to reclassify non-wage distributions as wages subject to employment taxes if the salary is deemed inadequate.

When to recommend S corp election to clients

Not every client benefits from S corp election. Use the following decision framework to evaluate candidates across your client base.

- Profit threshold: S corp tax savings typically become meaningful at $60,000 or more in annual profit. Below that level, the compliance costs and payroll overhead may outweigh the tax benefit.

- Consistent profitability: The client should have a track record of stable or growing profits, not just one strong year.

- Reasonable salary capacity: The business must generate enough revenue to pay the owner a reasonable salary before distributions.

- Compliance readiness: The client needs to be willing and able to maintain corporate formalities, including board meetings, annual reports, and detailed record-keeping.

Before filing, run through this eligibility checklist: US-based ownership only, no more than 100 shareholders, single class of stock, and no prohibited entity types among shareholders.

The Form 2553 filing deadline is the 15th day of the third month of the tax year for the election to take effect that year. Missing this deadline means waiting until the following tax year, so flag the timeline early in client conversations.

How entity choice affects your practice workflows

Entity selection doesn't just affect your clients. It changes the scope, complexity, and recurring nature of the work your practice handles for each engagement.

- Bookkeeping differences: S corps require payroll processing, W-2 preparation, and quarterly payroll tax filings (Forms 941). LLCs with a single member typically use simpler Schedule C reporting. Multi-member LLCs file partnership returns.

- Compliance calendar: S corps file Form 1120-S annually, plus state-level annual reports, corporate minutes documentation, and annual meeting records. LLCs have lighter state-level filing requirements.

- Salary documentation: For every S corp client, you'll need to research and document the reasonable salary determination. Use Bureau of Labor Statistics wage data, industry benchmarks, and the client's specific role to build a defensible salary position.

- Multi-entity management: If your practice handles a mix of LLCs and S corps, you're managing different compliance calendars, tax forms, and payroll requirements across clients. Standardized workflows and templates help maintain consistency.

- Technology: Cloud accounting software like Xero can streamline workflows across entity types. Automated bank feeds, integrated payroll, and smart reporting reduce the manual effort of managing different compliance requirements from a single platform.

How to advise clients switching from LLC to S corp

Many of your LLC clients will eventually become strong candidates for S corp election as their profits grow. Here's how to manage the conversion process.

The filing process involves two forms. Form 8832 elects corporate tax treatment for the LLC. Form 2553 then requests S corp status. Form 2553 must be filed by the 15th day of the third month of the tax year for the election to take effect that year.

Before filing, verify eligibility: all owners must be US citizens or residents, the entity can have no more than 100 shareholders, and only one class of stock is permitted. Check state-level requirements as well, since some states require a separate S corp election at the state level.

Frame the conversion conversation around tangible outcomes. Show the client their projected self-employment tax savings at current profit levels vs the added compliance costs. If the net benefit is clear, walk them through the timeline and filing requirements.

Conversion doesn't make sense for every client. If profits are below the $60,000 threshold, ownership includes foreign entities, or the client plans to bring on corporate or partnership investors, the LLC structure is likely the better fit. Advising a client to stay with their current structure is just as valuable as recommending a change.

Streamline entity management with Xero

Whether your clients choose LLC or S corp structures, Xero gives you real-time visibility across your entire client portfolio. Automated bank feeds, integrated payroll, and smart reporting make it straightforward to manage entities with different compliance requirements from a single platform.

Join the partner program to access free Xero for your practice, client subscription discounts, and dedicated partner support.

Frequently asked questions about S corps and LLCs

Here are frequently asked questions about advising clients on S corp vs LLC entity selection.

When should a client elect S corp status?

Don't wait for clients to ask. Build an annual review into your advisory workflow that flags clients crossing the $60,000 profit threshold. When profits are trending upward over two or more consecutive years, initiate the conversation proactively. This positions you as a strategic advisor rather than a reactive service provider, and it gives clients time to prepare for the compliance shift before the Form 2553 filing deadline.

What is a reasonable salary for an S corp owner?

The IRS doesn't define a specific number. Base the determination on what someone with similar experience and responsibilities would earn in the same industry. Use Bureau of Labor Statistics wage data, industry surveys, and the client's geographic market as supporting documentation. A conservative approach reduces audit risk.

Can a single-member LLC elect S corp status?

Yes. A single-member LLC can elect S corp tax treatment by filing Form 2553 with the IRS, provided the owner meets all S corp eligibility criteria including US citizenship or residency.

What are the tax implications of an S corp earning $200,000?

At $200,000 in profit, the S corp structure can produce meaningful self-employment tax savings compared to an LLC. The exact savings depend on the reasonable salary determination, but the distribution portion above the salary would be exempt from the 15.3% self-employment tax.

How does entity choice affect payroll workflows?

When a client converts from LLC to S corp, you'll need to set up payroll immediately since the IRS expects salary payments from day one of the election. Build the payroll setup into your conversion checklist alongside the Form 2553 filing. Factor the added payroll work into your pricing for S corp clients, as the quarterly filings and year-end reconciliation represent ongoing scope that should be reflected in your engagement fees.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Get one month free

Sign up to any Xero plan, and we will give you the first month free.