Cash flow forecasting: a guide for small businesses

Learn how to predict your cash position and plan ahead with confidence.

Written by Kari Brummond—Content Writer, Accountant, IRS Enrolled Agent. Read Kari's full bio

Published Tuesday 26 May 2026

Table of contents

Key takeaways

- A cash flow forecast predicts how much money your business will have at specific future dates, helping you spot potential shortfalls before they become emergencies and plan spending with confidence.

- Choose forecasting periods that match your goals: short-term forecasts (up to three months) for daily cash management, medium-term (three to 12 months) for annual planning, and long-term (one to five years) for expansion or financing decisions.

- Build your forecast in clear steps by gathering financial data, estimating inflows and outflows, calculating net cash flow, and reviewing regularly against actual results to improve accuracy over time.

- Accounting software with automatic bank feeds and real-time data reduces manual errors and keeps your forecast current, so you can focus on making decisions instead of updating spreadsheets.

What is a cash flow forecast?

A cash flow forecast is a financial plan that predicts how much money your business will have at specific future dates by estimating incoming and outgoing cash. It shows your expected cash position so you can plan spending, avoid shortfalls, and make informed decisions about growth.

Cash flow forecasting gives you visibility into your business's future financial health before problems arise. According to a Federal Reserve survey, cash flow challenges remain one of the most common financial difficulties for small businesses. A forecast helps you stay ahead of those challenges by mapping out when money comes in and when it goes out.

A cash flow projection is different from a cash flow statement. While a statement looks back at past cash movements, a projection looks forward to help you prepare for what's next.

What goes into a cash flow forecast

A complete cash flow projection includes four core elements that give you a full picture of your cash position. Here's what each one covers:

- Starting balance: the current cash in your business accounts at the beginning of the forecast period

- Cash inflows: expected money coming in from sales, customer payments, loans, grants, tax refunds, and owner contributions

- Cash outflows: planned expenses, loan repayments, payroll, rent, inventory costs, and other money leaving your business

- Ending balance: your projected cash position at the end of the forecast period, calculated by adding inflows to and subtracting outflows from your starting balance

Cash flow forecast vs. cash flow statement

A cash flow forecast and a cash flow statement serve different purposes, and understanding the distinction helps you use each one effectively. One looks forward; the other looks back.

A cash flow statement is a historical financial report that shows how cash actually moved through your business during a specific period. It records real transactions that already happened, organized into operating activities, investing activities, and financing activities. Lenders and investors often require cash flow statements to evaluate your business's financial health.

A cash flow forecast, on the other hand, estimates future cash movements based on your expected income and expenses. It's a planning tool you use to anticipate shortfalls, time large purchases, and make decisions about hiring or expansion before cash problems arise.

The two work best together. Your cash flow statement provides the historical data that makes your forecasts more accurate, while your forecast helps you act on that data to plan ahead. Comparing forecasted figures to actual results over time also helps you refine your estimates and improve forecast reliability.

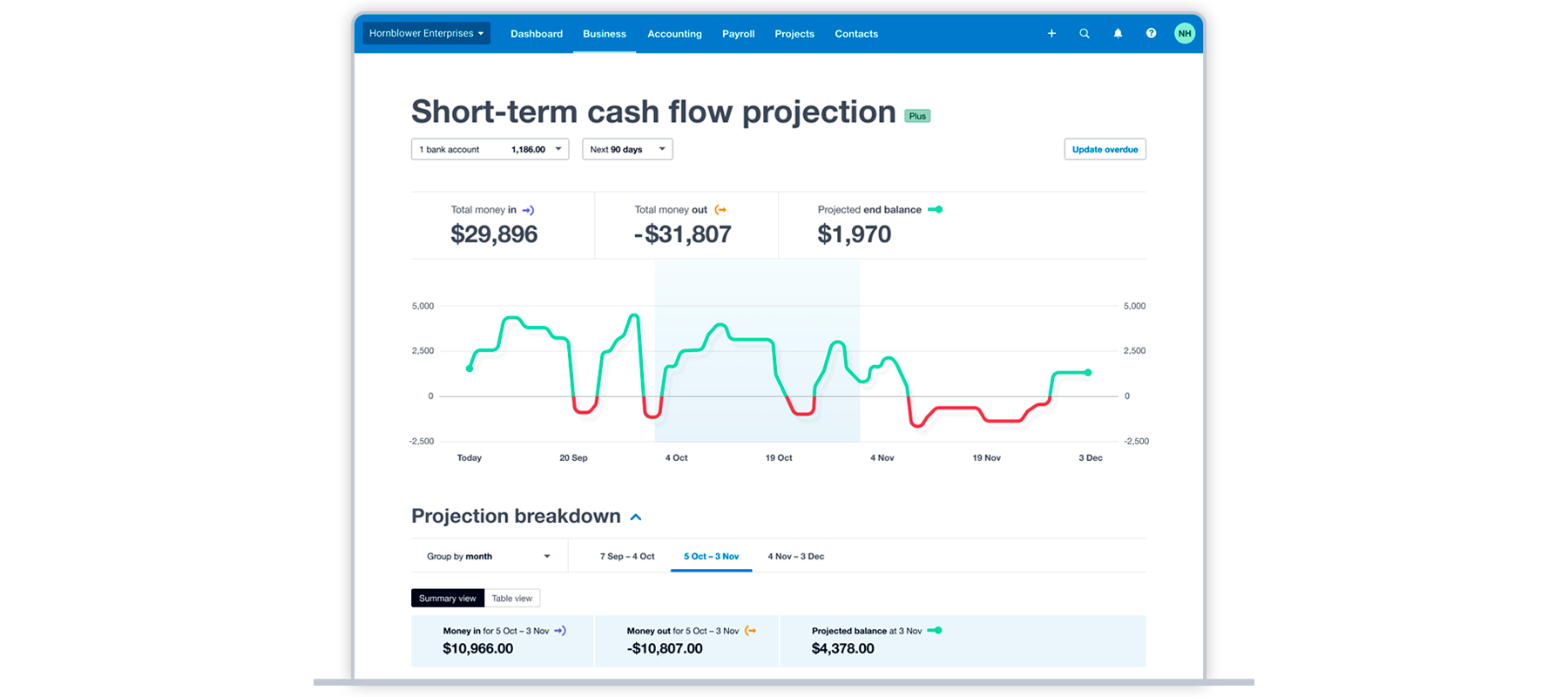

A cash flow dashboard shows how cash balances will rise and fall in response to expected transactions.

Components of a cash flow forecast

A cash flow forecast has three main parts that work together to show you the full picture of your money. Each component feeds into the next, giving you a clear view of where your cash stands.

- Cash inflows: all money coming into your business, including revenue from sales, customer payments, loan proceeds, grants, and investment income. Tracking inflows helps you see when cash is available to cover expenses and fund growth.

- Cash outflows: all money going out of your business, including rent, payroll, inventory costs, loan repayments, tax payments, and marketing spend. Categorizing outflows lets you identify where you're spending the most and where you might cut back.

- Net cash flow and closing balance: the difference between your inflows and outflows for a period, added to your starting cash balance. A positive net cash flow means more money came in than went out. A negative result signals that you may need to adjust spending or accelerate collections.

Benefits of a cash flow forecast

Cash flow forecasting helps you maintain financial control and avoid costly surprises. Instead of reacting to problems after they happen, a forecast gives you the information to act early. Here are some of the most valuable benefits:

- Spot potential shortfalls early: identify gaps before cash runs out so you can secure financing, delay non-essential spending, or speed up collections

- Evaluate growth plans: determine if you can afford new equipment, additional staff, or expansion projects before committing

- Detect financial trends: identify rising expenses or declining income patterns quickly so you can course-correct

- Address cash flow problems: resolve issues like slow-paying customers or unsustainable payment terms before they create a crisis

- Plan owner compensation: make sure there's enough cash flow to pay yourself regularly without putting the business at risk. For broader tips, see this guide on managing cash flow

- Strengthen loan applications: lenders want to see that you understand your cash position, and a well-prepared forecast demonstrates financial awareness

Learn more from SCORE about how cash flow forecasts can help you make business decisions.

Types of cash flow forecasting periods

Cash flow forecasting periods determine how far into the future you predict your cash position. Different timeframes serve different business planning needs, and the right choice depends on what decisions you're trying to make.

Short-term forecasts

Short-term forecasts cover cash flow over the next few days to three months, focusing on immediate cash availability. Use them to avoid overdrawing your account, plan inventory purchases, or prepare for urgent expenses like payroll or tax payments.

Many small businesses maintain a rolling 13-week short-term forecast as their primary cash management tool. This gives you enough visibility to catch problems early while keeping the data manageable.

Medium-term forecasts

Medium-term forecasts project cash flow three to 12 months ahead, helping with annual planning and larger business decisions. Common uses include:

- Planning for seasonal cash flow changes

- Budgeting for equipment purchases or office moves

- Preparing for off-season revenue drops

- Setting hiring timelines based on expected revenue

Long-term forecasts

Long-term forecasts project cash flow one to five years into the future, guiding major business strategy decisions. Use them for:

- Loan applications and financing decisions

- Business expansion planning

- Preparing for economic shifts or market changes

- Evaluating long-range profitability and sustainability

Mixed-period forecasts

Mixed-period forecasts combine multiple timeframes into a single view, letting you see both near-term details and long-range trends. They're useful for testing scenarios, such as:

- How a large short-term purchase affects your cash position six months from now

- How improving short-term collections makes it possible to invest in growth over the long term

- How seasonal revenue dips in one quarter affect your cash reserves in the following quarter

Learn more about financial management with the FDIC's small business education resources.

Cash flow forecasting methods

There are several methods you can use to build a cash flow forecast. The right one depends on your available data, business complexity, and how much detail you need.

Direct method

The direct method involves listing individual cash transactions, such as sales receipts, bill payments, and loan disbursements, to build your forecast line by line. It gives you a highly detailed view of cash timing, which is especially useful for short-term forecasts where precision matters.

The trade-off is that the direct method takes more time and effort to maintain. You need to track each transaction individually, which can become complex as your business grows.

Indirect method

The indirect method starts with your net income from existing financial statements and adjusts for non-cash items like depreciation, changes in accounts receivable, and inventory fluctuations. It's faster to set up if your financial statements are current and works well for medium- and long-term forecasts.

Because the indirect method relies on accrual-based data rather than actual cash transactions, it may be less precise for short-term cash timing. However, it gives you a solid overview of your overall cash trajectory.

Rolling forecasts

A rolling forecast continuously extends your projection by adding a new period as each current period ends. For example, a 13-week rolling forecast always looks 13 weeks ahead, with a new week added each time one passes.

Rolling forecasts keep your projections current and reduce the risk of relying on outdated assumptions. They work well for businesses with fluctuating revenue or seasonal patterns, since you're constantly refreshing the data rather than working from a static annual projection.

How to forecast your cash flow

Building a cash flow forecast involves estimating when money will come in and go out of your business, then calculating your expected cash position at specific future dates. Follow these seven steps to create a reliable forecast.

1. Set clear forecasting goals

Define your purpose before building a projection. Your goals shape every other decision in the process, from the timeframe to the level of detail. Common forecasting goals include:

- Making sure you have enough cash for payroll and immediate expenses

- Planning a major equipment purchase or facility improvement

- Evaluating financing needs for business expansion

- Preparing a cash flow projection for a lender or investor

2. Choose your forecasting time frame

Select a time frame that aligns with your goals. If you need to manage day-to-day cash, a short-term forecast of up to 13 weeks works well. For annual planning, use a medium-term forecast of three to 12 months. Long-term or mixed-period forecasts are better suited for expansion planning or loan applications.

3. Choose a forecasting method

Decide whether to use the direct method, indirect method, or a rolling forecast. The direct method gives you detailed transaction-level projections. The indirect method is faster if your financial statements are up to date. A rolling forecast keeps your projections current by continuously extending the timeline.

Select the method that matches your available data and the level of detail your goals require.

4. Gather your financial data

Collect the numbers you need to build your forecast. Start with your current cash balance across all business accounts. Then pull together historical data on income, expenses, and payment timing.

Accounting software with automatic bank feeds makes this step faster by pulling real-time transaction data directly from your bank accounts. If you're using spreadsheets, gather your most recent bank statements, invoices, and bills. You can also use a cash flow forecast template to organize your data.

5. Estimate inflows and outflows

List every expected source of incoming cash and every anticipated expense for your forecast period. For inflows, include sales revenue, customer payments, loan proceeds, grants, tax refunds, and any other money you expect to receive. For outflows, include rent, payroll, inventory, estimated tax payments, loan repayments, utilities, and any other planned spending.

Be specific about timing. A sale you make in March may not turn into cash until April or May, depending on your payment terms. Dating each expected transaction helps you see exactly when cash will be available.

6. Calculate net cash flow

For each period in your forecast, subtract total outflows from total inflows to get your net cash flow. Then add that figure to your starting balance to find your closing balance for the period.

Here's the formula: Starting balance + total inflows - total outflows = closing balance. A positive closing balance means you have enough cash to cover your obligations. A negative result means you need to take action, whether that's cutting expenses, speeding up collections, or arranging short-term financing.

7. Review and adjust regularly

Compare your forecasted figures to actual results at the end of each period. Note where your estimates were accurate and where they fell short. Then update future projections based on what you've learned.

Regular reviews make your forecast more reliable over time. You can use a business plan template from SCORE to structure your review process alongside your broader financial planning.

Cash flow forecast example

A simple numerical walkthrough can make the forecasting process concrete. Here's how a one-month cash flow forecast might look for a small consulting business.

Start with your opening cash balance. In this example, you begin the month with $15,000 in your business account.

Next, estimate your expected inflows for the month:

- Client payments: $12,000

- Retainer fees: $3,000

- Tax refund: $500

- Total inflows: $15,500

Then list your expected outflows:

- Rent: $2,500

- Payroll (including your own salary): $6,000

- Software subscriptions: $400

- Marketing: $1,200

- Insurance: $350

- Utilities and internet: $250

- Estimated tax payment: $2,000

Total outflows: $12,700.

Calculate your net cash flow: $15,500 (inflows) - $12,700 (outflows) = $2,800 positive net cash flow.

Finally, calculate your closing balance: $15,000 (opening) + $2,800 (net cash flow) = $17,800. That's your projected cash position at the end of the month.

If the result had been negative, you'd know to take action before the month starts, perhaps by invoicing clients earlier, delaying a non-essential expense, or arranging a line of credit. The value of the forecast is that it shows you these scenarios in advance.

Cash flow forecasting best practices

A forecast is only as useful as the effort you put into keeping it accurate and actionable. These practices help you get the most from your cash flow projections.

- Use conservative estimates. Project lower income and higher expenses than you expect. This gives you a buffer for late payments, unexpected costs, or slower sales months. If actual results come in better than projected, that's a welcome surprise rather than a cash crisis.

- Update your forecast regularly. A monthly review is the minimum for most businesses. If your cash flow fluctuates significantly, update weekly. Each review is a chance to compare projections to actual results and sharpen future estimates.

- Run scenario analysis. Create best-case, worst-case, and most-likely versions of your forecast. This helps you prepare for different outcomes and identify how much financial cushion you need. For example, what happens if your largest client pays 30 days late?

- Track variance between forecasted and actual figures. The gap between what you predicted and what actually happened reveals patterns in your estimating. Over time, tracking variance helps you build more reliable forecasts.

- Connect your forecast to your accounting system. When your forecast pulls directly from your accounting data, you spend less time on manual data entry and reduce the risk of errors. Xero's cash flow monitoring tools and bank feeds keep your financial data current, so your projections stay grounded in real numbers. Learn more about how to manage your finances and cash flow effectively.

Common cash flow forecasting challenges

Even with a solid process in place, cash flow forecasting comes with challenges that can affect accuracy. Recognizing these pitfalls helps you work around them.

- Inaccurate or incomplete data. Your forecast is only as good as the numbers behind it. If your books aren't up to date, or if you're missing transactions, your projections will be off. Keeping your accounting records current and reconciling bank accounts regularly is the foundation of a reliable forecast.

- Unpredictable payment timing. Customers don't always pay on schedule, and unexpected expenses can appear without warning. Build flexibility into your forecast by accounting for payment delays and keeping a cash reserve for unplanned costs.

- Over-optimistic revenue estimates. It's natural to expect the best, but projecting income too high is one of the most common forecasting mistakes. Use historical data and conservative assumptions to keep your estimates grounded.

- Manual process errors. Spreadsheet-based forecasts are prone to formula mistakes, copy-paste errors, and version control problems. As your business grows, the volume of transactions can make manual updates unsustainable. Accounting software with automated bank feeds and built-in reporting reduces these risks.

- Failing to update the forecast. A forecast created in January and never revisited by March is already outdated. Business conditions change, and your projections need to change with them. Build regular forecast reviews into your financial routine.

Take control of your cash flow with Xero

A strong cash flow forecast gives you the clarity to plan ahead, avoid surprises, and make confident financial decisions for your business. The key is consistent, accurate data and a regular review process.

Xero Accounting Software makes cash flow forecasting easier by automatically pulling in bank transactions, keeping your books up to date, and giving you real-time visibility into your cash position. Xero also integrates with apps like Fathom and Calxa for more detailed, long-term projections. Get one month free.

FAQs on cash flow forecasting

Here are answers to frequently asked questions about cash flow forecasting for small businesses.

What's the difference between a cash flow forecast and a cash flow statement?

A cash flow statement is a historical report that shows how cash actually moved through your business during a past period. A cash flow forecast is a forward-looking plan that estimates future cash movements based on your expected income and expenses. The statement tells you what happened; the forecast helps you prepare for what's next.

How often should I update my cash flow forecast?

Update your forecast at least monthly, or weekly if your business has significant cash flow fluctuations or seasonal patterns. Regular updates let you compare projections to actual results, catch potential problems early, and refine your estimates over time.

What's the best forecasting period for a small business?

Most small businesses benefit from maintaining a short-term rolling forecast of 13 weeks for day-to-day cash management alongside a medium-term forecast of 12 months for annual planning. Add a long-term forecast of one to five years when you're planning expansion or applying for financing.

How do I calculate cash flow for my business?

Start with your opening cash balance, add all expected inflows (sales, payments, loans) for the period, then subtract all expected outflows (rent, payroll, expenses). The result is your closing balance. The formula is: opening balance + total inflows - total outflows = closing balance. Repeat this calculation for each period in your forecast.

What is a rolling cash flow forecast?

A rolling forecast continuously extends your projection by adding a new period as each current period ends. For example, a 13-week rolling forecast always looks 13 weeks into the future, with a new week added each time one passes. This approach keeps your projections current and prevents you from relying on assumptions that may no longer reflect your business reality.

What are common cash flow forecasting mistakes?

The most frequent mistakes include over-estimating revenue, under-estimating expenses, not accounting for payment timing delays, and creating a forecast once without updating it. Using outdated data or ignoring seasonal patterns can also throw off your projections. Building conservative estimates and reviewing your forecast regularly against actual results helps you avoid these pitfalls.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Get one month free

Sign up to any Xero plan, and we will give you the first month free.