What is accumulated depreciation? A guide for small businesses

Learn how accumulated depreciation works and how to calculate it for your small business.

Written by Jotika Teli—Certified Public Accountant with 24 years of experience. Read Jotika's full bio

Published Monday 15 June 2026

Table of contents

Key takeaways

- Accumulated depreciation is the running total of depreciation recorded against an asset since purchase, and subtracting it from the original cost gives you the asset's book value.

- The straight-line method spreads depreciation evenly over an asset's useful life, while declining balance and units of production methods suit assets that lose value faster early on or based on usage.

- Depreciation is a non-cash expense that gets added back on the cash flow statement, so it doesn't reduce the cash available in your business.

- Tracking accumulated depreciation accurately helps you claim capital allowances to reduce your tax bill, plan asset replacements, and present stronger financial records when applying for financing.

How accumulated depreciation works

Accumulated depreciation is the total depreciation expense recorded against an asset since you bought it. It tracks how much value your asset has lost over time due to wear, tear, and obsolescence.

You record accumulated depreciation in a contra asset account. Unlike regular asset accounts that carry a debit balance, this account carries a credit balance.

On your balance sheet, accumulated depreciation sits directly beneath the related fixed asset. This lets you see the original cost and total depreciation side by side.

Subtract accumulated depreciation from the asset's original cost to get its book value. This figure shows what the asset is currently worth to your business.

Is accumulated depreciation an asset or a liability?

Accumulated depreciation is a contra asset account, not an asset or a liability. It appears on the balance sheet but works differently from both.

Here's why it isn't classified as a liability:

- No debt obligation: you don't owe money to anyone

- No repayment requirement: it simply reduces asset value over time

- No cash outflow: it measures wear, tear, and obsolescence without affecting cash

A contra asset reduces the value of assets on your balance sheet. It carries a credit balance, showing how much an asset's worth has decreased from its original cost.

Depreciation vs accumulated depreciation

Depreciation and accumulated depreciation are related but different concepts. Understanding the distinction helps you read your financial statements accurately.

- Depreciation: the annual expense showing how much an asset's value decreases in a single year

- Accumulated depreciation: the running total of all depreciation expenses recorded for that asset since purchase

Each year, you add the current year's depreciation expense to the accumulated total. Over time, accumulated depreciation grows until the asset reaches the end of its useful life.

How does accumulated depreciation affect financial statements?

Accumulated depreciation appears on 3 key financial statements, each showing a different aspect of how asset values affect your business finances.

Accumulated depreciation on the balance sheet

On the balance sheet, accumulated depreciation reduces your asset's book value. Your balance sheet displays the original purchase price, then subtracts accumulated depreciation to show the asset's current worth.

Accumulated depreciation on the income statement

While depreciation expense reduces your accounting profit, it's not allowed as a deduction when computing taxable profits. Instead, capital allowances may be given to lower your tax bill. This non-cash expense gives you the tax benefit without any money leaving your business.

In the UK, businesses can often claim a 100% allowance on qualifying plant and machinery (a type of capital expenditure) up to a £1 million threshold through the Annual Investment Allowance (AIA).

Accumulated depreciation on the cash flow statement

Depreciation gets added back to net income on the cash flow statement because no actual cash leaves your business. This adjustment shows the difference between accounting profits and actual cash available.

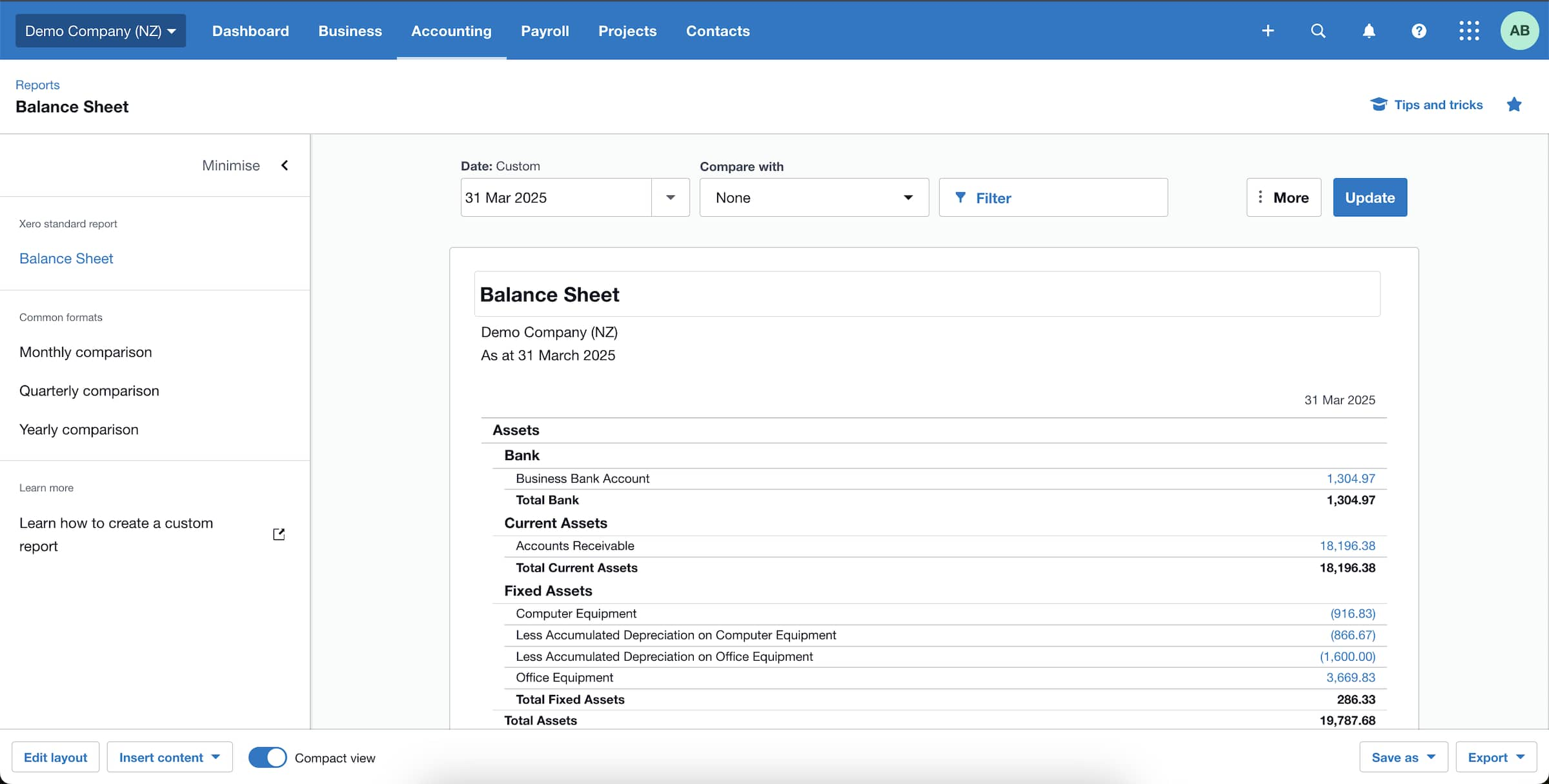

Example: balance sheet for accumulated depreciation

Here's a simple example of how accumulated depreciation appears on a balance sheet for a delivery van:

- Cost of van: £20,000

- Accumulated depreciation after 3 years: £9,000

- Net book value: £11,000

On your balance sheet, you show the cost of the van and subtract the accumulated depreciation to arrive at the net book value.

How to calculate accumulated depreciation

Calculating accumulated depreciation helps you track your asset's current value for financial reporting and tax purposes. The result shows how much total depreciation you've recorded since purchasing the asset.

The straight-line method is the simplest approach and most popular with small businesses because it spreads the cost evenly over the asset's useful life. If that useful economic life is estimated to be longer than 50 years, FRS 102 Section 27 requires annual impairment reviews to make sure the asset's carrying amount isn't overstated.

The straight-line depreciation method

The straight-line formula spreads an asset's cost evenly over its useful life:

Annual depreciation expense = (Asset cost - Salvage value) / Useful life

What each term means

Here's what each term in the formula represents:

- Asset cost: original purchase price including delivery and setup costs

- Salvage value: expected resale or scrap value when the asset reaches end of life

- Useful life: number of years you expect to use the asset before replacing it

Under FRS 102 Section 25, businesses may also need to capitalise borrowing costs incurred during construction as part of the asset's total cost. Learn more about measuring depreciation.

Useful life is an estimate. You may need to reassess it during the asset's lifetime, which would change the annual depreciation expense for future years.

Each variable affects your annual depreciation expense differently:

- Shorter useful life: spreads depreciation over fewer years, resulting in higher annual expense

- Higher salvage value: reduces the depreciable amount, resulting in lower annual expense

- Higher asset cost: increases the depreciable amount, resulting in higher annual expense

Worked example: straight-line method

Here's how to calculate accumulated depreciation using the straight-line method. In this example, the asset costs £1,000, has a useful life of 5 years, and a salvage value of £100.

- Calculate the annual depreciation expense. Using the formula: (£1,000 - £100) / 5 = £180 per year.

- Track accumulated depreciation each year. Create a depreciation schedule showing how accumulated depreciation grows: Year 1 = £180, Year 2 = £360, Year 3 = £540, Year 4 = £720, Year 5 = £900.

- Calculate the asset's book value. Use the formula: Book value = Initial cost - Accumulated depreciation. After 3 years: £1,000 - £540 = £460 book value.

Alternative depreciation methods

The straight-line method works well for many assets, but alternative methods may suit your business better depending on how your assets lose value. Some assets depreciate faster in early years or based on usage.

For complex assets, you can also depreciate components separately. Learn more about depreciation methods. For example, you might depreciate a furnace's lining over 5 years while depreciating the main body over 10 years.

Declining balance method

The declining balance method applies higher depreciation in early years and lower depreciation in later years. This front-loads the expense to match how some assets actually lose value.

The formula is:

Depreciation expense = Book value at start of year x Depreciation rate

For example, if you buy equipment for £10,000 with a 20% depreciation rate:

- Year 1: £10,000 x 20% = £2,000 depreciation (book value drops to £8,000)

- Year 2: £8,000 x 20% = £1,600 depreciation (book value drops to £6,400)

- Year 3: £6,400 x 20% = £1,280 depreciation (book value drops to £5,120)

Use this method for assets like vehicles or tech equipment that lose value more quickly at the start of their useful life.

Units of production method

The units of production method bases depreciation on usage rather than time. You calculate depreciation based on the number of units produced or hours operated.

The formula is:

Depreciation expense = ((Asset cost - Salvage value) / Total estimated units) x Units produced in the period

For example, if you buy a printing press for £50,000 with a £5,000 salvage value and an estimated output of 500,000 units:

- Depreciation per unit: (£50,000 - £5,000) / 500,000 = £0.09

- Year 1 (120,000 units produced): 120,000 x £0.09 = £10,800

- Year 2 (80,000 units produced): 80,000 x £0.09 = £7,200

This method is ideal for manufacturing equipment or machinery where wear and tear relates directly to how much you use the asset. It provides more accurate depreciation when usage varies significantly from year to year.

Choose your depreciation method based on how the asset loses value and your business needs. If you later switch methods, such as moving from declining balance to straight-line, you must account for this prospectively as a change in accounting estimate. Talk with your accountant to decide which approach gives the most accurate picture of your asset values.

Accumulated depreciation and book value

Book value shows what an asset is worth on your balance sheet after accounting for depreciation. It's one of the most practical figures for understanding your business's financial position.

The formula is straightforward:

Book value = Original cost - Accumulated depreciation

As accumulated depreciation increases each year, the book value decreases. When an asset is fully depreciated, its book value equals its salvage value (or zero if no salvage value was set).

Book value matters for several practical reasons:

- It determines the gain or loss when you sell or dispose of an asset

- Lenders and investors review book values to assess your business's net worth

- It helps you decide when to replace ageing assets

- It feeds into your overall balance sheet totals for fixed assets

Keep in mind that book value doesn't always reflect what you'd actually receive if you sold the asset. Market value can be higher or lower depending on demand, condition, and market trends.

What happens when you sell or dispose of an asset

When you sell or dispose of a fixed asset, you need to remove both the asset's original cost and its accumulated depreciation from your books. The difference between the sale price and the book value determines whether you've made a gain or a loss.

Here's how to work it out:

- If you sell for more than book value, you record a gain on disposal

- If you sell for less than book value, you record a loss on disposal

- If you sell for exactly book value, there's no gain or loss

For example, if a piece of equipment originally cost £10,000 and has £7,000 of accumulated depreciation, the book value is £3,000. If you sell it for £4,500, you record a £1,500 gain. If you sell it for £2,000, you record a £1,000 loss.

The basic journal entries for a disposal involve removing the asset and its accumulated depreciation from your accounts, recording what you received, and recognising the gain or loss. Your accounting software typically handles these entries when you record the disposal of a fixed asset.

In the UK, gains or losses on disposal may also affect your capital allowances position. If you sell an asset for more than its tax written-down value, you may face a balancing charge. Selling for less may generate a balancing allowance. Talk with your accountant to make sure you claim the right allowances.

Why understanding accumulated depreciation matters for your business

When you understand accumulated depreciation, it helps your small business in several practical ways.

- Reduce your tax bill: depreciation feeds into capital allowances calculations, which lower your taxable income. Tracking accumulated depreciation accurately means you can claim the right allowances each year and keep more cash in your business.

- Plan asset replacements: as accumulated depreciation grows, book values fall. Monitoring this trend helps you budget for replacements before assets fail or become inefficient, avoiding unexpected costs.

- Strengthen loan applications: lenders review your balance sheet when assessing creditworthiness. Accurate depreciation records show that you manage your finances carefully, improving your chances of securing business financing.

- Value your business accurately: if you're looking to sell or bring in investors, your asset values need to reflect reality. Correct accumulated depreciation gives a true picture of what your business owns and what those assets are worth.

- Make confident investment decisions: knowing the book value and remaining useful life of your assets helps you decide whether to repair, upgrade, or replace equipment. This leads to smarter spending and better returns on your investments.

Simplify your accounting with Xero

As your business grows, depreciation becomes more complex to track. Xero streamlines these tasks so you spend less time on admin and more time running your business.

With Xero, you can create detailed depreciation schedules for a clear view of your fixed asset values. This means more accurate financial reporting and a clearer view of what your assets are worth. Get one month free.

FAQs on accumulated depreciation

Here are some frequently asked questions about accumulated depreciation.

What is the journal entry for accumulated depreciation?

The journal entry debits depreciation expense and credits accumulated depreciation. This records the expense on your income statement while increasing the contra asset on your balance sheet.

What happens to accumulated depreciation when you sell an asset?

When you sell an asset, you remove both the original cost and the accumulated depreciation from your books. The difference between the sale price and the book value is recorded as a gain or loss on disposal.

Does accumulated depreciation affect cash flow?

Depreciation is a non-cash expense, so it doesn't directly reduce your cash. On the cash flow statement, it gets added back to net income to show the actual cash your business generated.

Can accumulated depreciation exceed an asset's original cost?

No, accumulated depreciation can't exceed the asset's depreciable amount (original cost minus salvage value). Once an asset is fully depreciated, you stop recording depreciation expense even if you continue using it.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Get one month free

Purchase any Xero plan, and we will give you the first month free.