Margin of safety formula: calculate it and assess risk

Learn how the margin of safety formula helps your business spot risk, plan sales, and protect profit.

Written by Shaun Quarton—Accounting & Finance Content Writer and Growth Marketer. Read Shaun's full bio

Written by Shaun Quarton—Accounting & Finance Content Writer and Growth Marketer. Read Shaun's full bio

Published Monday 20 April 2026

Table of contents

Key takeaways

- Calculate your margin of safety by subtracting your break-even sales from your current sales, then dividing the result by your current sales — the percentage tells you how far sales can fall before your business starts making a loss.

- Aim for a margin of safety of 20% or more, and recalculate it monthly or quarterly, or whenever your costs, pricing, or supplier prices change significantly.

- Use your margin of safety to guide key business decisions, such as setting sales targets, adjusting prices, cutting costs, or assessing whether a new product launch is financially viable.

- Combine your margin of safety with other financial tools, such as cost-volume-profit analysis, to get a fuller picture of your business's profitability and financial risk.

What is the margin of safety?

Margin of safety is the percentage by which your current sales exceed your break-even point. It shows how far sales can drop before your business starts making a loss.

The wider this margin, the better protected you are from unexpected changes like rising costs or falling demand.

What is the margin of safety formula?

The margin of safety formula calculates what percentage your sales can drop before reaching break-even:

Margin of safety = (Current sales - Break-even sales) ÷ Current sales

The result is a percentage that represents your financial buffer against declining sales. Find out how to calculate margin.

- Current sales: the total revenue your business earns from selling goods and services over a specific period

- Break-even sales: the exact revenue needed to cover all fixed and variable costs, resulting in zero profit and zero loss

A business has current sales of £50,000 and needs £30,000 to break even.

Margin of safety = (£50,000 – £30,000) / £50,000 = 0.4 (40%)

This means sales could drop by 40% before hitting break-even. Any further decline would result in a loss.

How to calculate margin of safety

Here's how to break down the margin of safety calculation.

1. Find your current sales

The first step is to determine your current sales, whether actual or forecasted.

You can usually find your current sales figures quickly in your existing sales tools.

When you forecast sales, you predict future revenue using data analysis and industry insights. Use these four methods to forecast accurately:

- Historical data: analyse past sales trends and seasonal patterns from your point-of-sale system, e-commerce platform, or accounting software like Xero. Run financial reports with Xero

- Market research: study your target market, industry trends, and competitor performance to understand market conditions

- Qualitative forecasting: gather insights from your sales team or industry experts based on their experience

- Quantitative forecasting: apply statistical methods to historical and market data to predict more precisely

Choose your approach based on your business type and available data.

For example, a craft business uses a POS system to track monthly sales. Last month, sales were £5,000. This figure feeds into the margin of safety calculation below.

2. Calculate your break-even sales revenue point

To work out your break-even sales, divide your total fixed costs by the contribution to sales ratio. Learn more in this CVP analysis guide. For margin of safety, you need this as a revenue figure, not unit sales.

Break-even sales = Fixed costs ÷ ((Sales price - Variable cost) ÷ Sales price)

- Fixed costs: expenses that stay the same regardless of sales volume, such as salaries and rent

- Variable costs: expenses that change with sales volume, such as raw materials and sales commission. Find more information on variable costs and how they differ from fixed costs. Learn more about calculating marginal cost

Your accountant can also help you distinguish between them.

The craft business has:

- fixed costs of £2,000

- variable costs of £5 per unit

- a sales price of £25 per unit

Therefore:

2,000 ÷ ((25 – 5) ÷ 25) = 2,000 ÷ (20 ÷ 25) = 2,000 ÷ 0.8 = £2,500

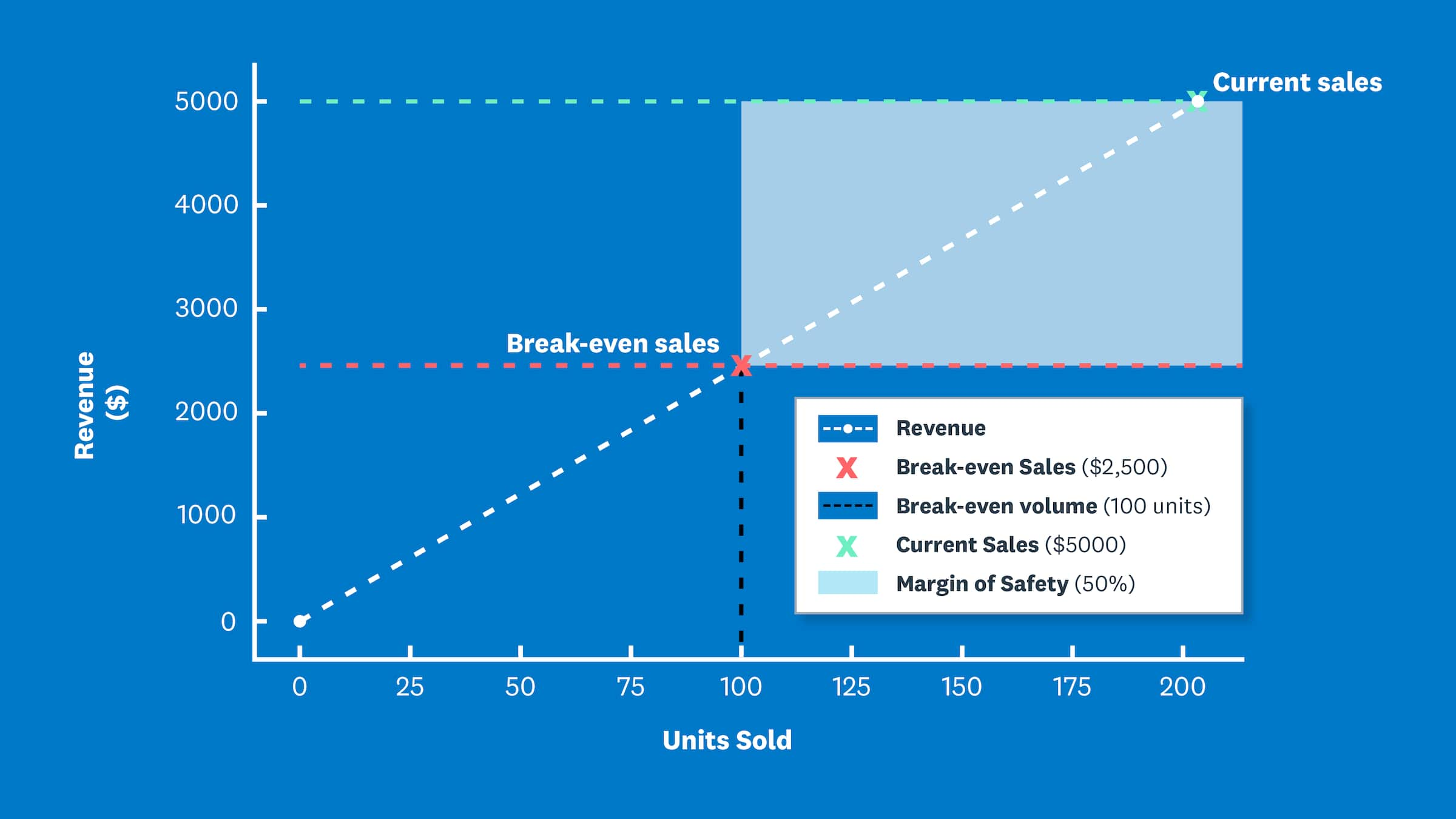

With a sales price of £25, you need revenue of £2,500 (100 units) to break even.

3. Apply the margin of safety formula

Finally, apply the margin of safety formula:

(Current sales – Break-even sales) ÷ Current sales = Margin of safety

Your margin of safety ratio is the percentage by which sales can fall before your business starts operating at a loss.

Applying the formula to the craft business example, where current sales are £5,000 and break-even sales are £2,500:

(£5,000 – £2,500) ÷ £5,000 = 0.5 = 50%

The craft business has a 50% margin of safety, meaning sales could fall by half before reaching break-even.

The importance of the margin of safety for your small business

Understanding your margin of safety helps you assess your business's financial risk. Studies show corporations manage risks in the belief it will increase corporate value.

Research shows larger firms often manage this type of risk, while smaller companies do not. This creates an opportunity for small businesses to gain an edge.

- High margin of safety: your business can absorb market shifts without disruption, keeping risk low

- Low margin of safety: your business is operating close to break-even with little room for error, keeping risk high

Consider how an external shock, like a jump in supplier prices, would affect your business. Learn more about calculating gross profit. This increase in variable costs pushes up your break-even point, eating into your margin of safety and leaving you exposed to further cost increases or falling sales.

Your margin of safety also supports smarter financial decisions, from pricing to cost control and growth plans.

How the margin of safety supports your business decisions

Use your margin of safety to make smarter choices in these areas:

- Performance targets: set achievable sales targets above your break-even point to ensure profitability

- Pricing strategy: adjust prices when your margin shrinks to ensure each sale covers costs adequately

- Cost control:cut expenses when your margin is low to protect your financial buffer

- Product launches: evaluate how new products affect your margin before investing in development

Beyond these decisions, consider how margin of safety works with other financial tools.

Use margin of safety alongside other key metrics

Margin of safety is most effective when used alongside other financial metrics, particularly when you calculate break-even points for multiple products. Learn more in this CVP analysis guide.

For example, combine it with cost-volume-profit (CVP) analysis to calculate the sales revenue required to achieve a target profit. Learn more about CVP analysis. This gives you a clearer view of your profitability and risk.

Master your margin of safety with Xero

Calculating margin of safety manually wastes valuable time tracking figures across spreadsheets and reports.

Xero automates how you collect data and generate reports, so you can calculate accurately. Access real-time financial data and generate reports instantly, so you can decide confidently and faster.

Ready to manage your finances more simply? Get one month free and see how easy it is to calculate margin of safety.

FAQs on margin of safety

Here are answers to common questions to help you get the most out of this metric.

What is a good margin of safety ratio?

There's no single 'good' ratio as it depends on your industry and how stable your business is. Many businesses aim for 20% or more, which provides a healthy buffer. Volatile industries may need an even wider margin to protect against unexpected changes.

When should I recalculate my margin of safety?

Check your margin of safety quarterly or monthly. Recalculate whenever significant changes occur, such as:

- shifts in fixed costs

- changes in supplier prices

- new pricing strategies

Can margin of safety be negative?

Yes. A negative margin of safety means your sales are below break-even and your business is making a loss.

Act quickly to lift sales or reduce costs. If losses continue, your accountant may question whether your business can keep trading. This is referred to as a 'going concern' issue. This level of professional oversight is used by 98% of the best global brands who rely on chartered accountants. Learn more about breakeven analysis.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Get one month free

Purchase any Xero plan, and we will give you the first month free.