Break-even point formula

Learn how to calculate your break-even point in units and revenue with simple formulas and worked examples.

November 2023 | Published by Xero

Published Thursday 23 July 2026

Table of contents

Key takeaways

- The break-even point is where your total revenue equals your total costs, meaning you're neither making a profit nor a loss.

- You can calculate your break-even point in units (how many items you need to sell) or in revenue (how much money you need to bring in) using 2 simple formulas.

- Understanding your break-even point helps you set prices, control costs, and plan for profitability before you start spending.

- Regularly recalculating your break-even point as costs and prices change keeps your financial planning accurate and up to date.

What is the break-even point?

The break-even point (BEP) is the moment your business revenue exactly covers all your costs. At this point, you haven't made a profit, but you haven't made a loss either.

To find your break-even point, you need to understand 3 key figures: your fixed costs, your variable costs, and your selling price. The difference between your selling price and your variable cost per unit is called the contribution margin. It's the amount each sale contributes towards covering your fixed costs.

Once your total contribution margin equals your fixed costs, you've reached your break-even point. Every sale after that generates profit.

Why break-even analysis matters

Knowing your break-even point gives you a clear financial target to work towards. It's one of the most practical tools for making confident decisions about your business.

Here's how break-even analysis helps:

- Setting prices: it shows the minimum price you need to charge to cover your costs, so you can price with confidence

- Controlling costs: it highlights the relationship between your fixed and variable costs, making it easier to spot where you can cut spending

- Planning for profit: it tells you exactly how many sales you need before you start making money, so you can set realistic profitability targets

- Securing funding: lenders and investors often expect to see a break-even analysis in your business plan, as it demonstrates you understand your finances

How to calculate the break-even point

Before running the formula, you'll need to gather 3 numbers from your business finances.

- Fixed costs: these are expenses that stay the same regardless of how much you sell, such as rent, insurance, salaries, and software subscriptions

- Variable costs per unit: these are expenses that change with each unit you produce or each hour you work, such as raw materials, packaging, or contractor fees

- Selling price per unit: this is what you charge your customers for each product or hour of service

The contribution margin per unit is your selling price minus your variable cost per unit. This figure is the foundation of both break-even formulas below.

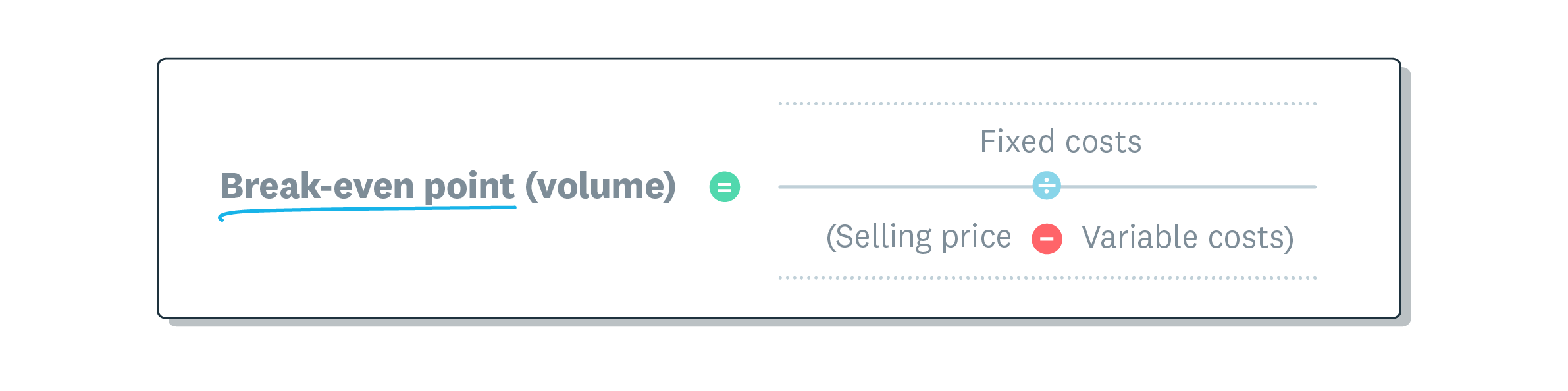

Break-even point in units

This formula tells you how many units you need to sell to cover all your costs.

Break-even point (units) = Fixed costs / (Selling price per unit - Variable cost per unit)

In other words, you're dividing your total fixed costs by the contribution margin per unit. The result is the exact number of units you need to sell before you start making a profit.

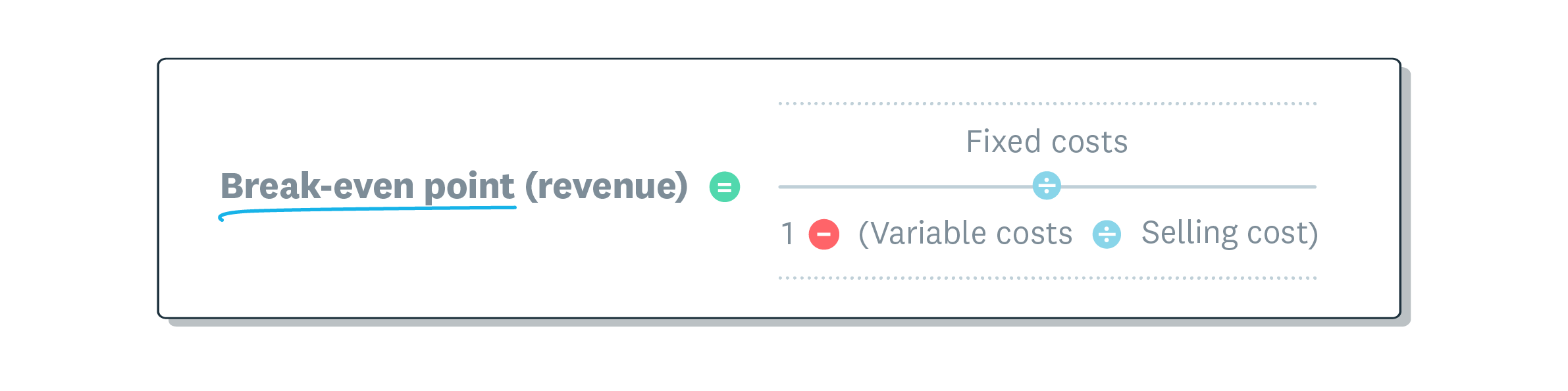

Break-even point in revenue

This formula tells you the total sales value you need to reach to cover all your costs. It uses the contribution margin ratio instead of the per-unit figure.

First, calculate the contribution margin ratio:

Contribution margin ratio = (Selling price per unit - Variable cost per unit) / Selling price per unit

Then use it in the revenue formula:

Break-even point (revenue) = Fixed costs / Contribution margin ratio

This approach is especially useful for service-based businesses or those selling multiple products at different prices.

Break-even calculation examples

These 2 worked examples show how to calculate the break-even point for both a product-based and a service-based business.

Break-even example for a product-based business

A kombucha brewery has fixed monthly costs of £6,000 for rent, utilities, insurance, and advertising. Their variable costs are £2 per bottle for packaging, ingredients, and labour. They sell each bottle for £7.

Break-even in revenue:

Contribution margin ratio = (£7 - £2) / £7 = 0.714

Break-even point (revenue) = £6,000 / 0.714 = £8,403

The kombucha brewery needs to bring in £8,403 in monthly revenue to break even.

Break-even in units:

Break-even point (units) = £6,000 / (£7 - £2) = £6,000 / £5 = 1,200

The kombucha brewery needs to sell 1,200 bottles per month to break even.

Break-even example for a service-based business

A graphic designer has fixed monthly costs of £2,700 for utilities, hardware leases, software subscriptions, and advertising. Their variable costs are £35 per hour to hire a contractor. They charge clients £75 per hour.

Break-even in revenue:

Contribution margin ratio = (£75 - £35) / £75 = 0.533

Break-even point (revenue) = £2,700 / 0.533 = £5,066

The graphic designer needs to earn £5,066 in monthly revenue to break even.

Break-even in units:

Break-even point (units) = £2,700 / (£75 - £35) = £2,700 / £40 = 67.5

The graphic designer needs to bill 67.5 hours per month to break even.

Factors that affect your break-even point

Your break-even point isn't fixed. It shifts whenever your costs or pricing change, so it's worth recalculating regularly.

- Fixed cost changes: if your rent increases or you take on a new subscription, your break-even point rises because you've got more costs to cover before you make a profit

- Variable cost changes: a rise in material prices or contractor rates pushes your break-even point higher by shrinking your contribution margin on each sale

- Selling price adjustments: raising your prices increases the contribution margin per unit, which lowers your break-even point; dropping prices has the opposite effect

- Product or service mix: if you sell multiple items at different margins, your overall break-even point depends on the proportion of high-margin and low-margin sales. Learn more about margin of safety to understand the buffer between your sales and your break-even point

Limitations of break-even analysis

Break-even analysis is a useful starting point, but it doesn't capture every aspect of running a business. Keep these limitations in mind when using it.

- It's based on assumptions: the formula assumes your costs and selling price stay constant, which rarely happens in practice

- It doesn't account for demand: the calculation tells you how much you need to sell, but not whether customers will actually buy that amount

- It assumes linear costs: in reality, variable costs per unit can change at different production levels; for example, bulk discounts on materials lower your cost per unit as you scale

- It excludes indirect costs: break-even analysis typically focuses on direct fixed and variable costs, and may not capture overhead like marketing spend or administrative expenses

Simplify your break-even analysis with Xero

Accurate break-even calculations depend on having clear, up-to-date financial data. Xero's accounting software automatically tracks your income and expenses, giving you the figures you need to calculate your break-even point with confidence.

With real-time reporting and easy-to-read dashboards, you can monitor how your costs and revenue are trending, so you'll know when you're approaching profitability. Get one month free.

FAQs on break-even point formula

Here are some frequently asked questions about break-even point formula.

How do you calculate break-even for multiple products?

Calculate a weighted average contribution margin based on the proportion of each product you sell, then divide your total fixed costs by that weighted average. This gives you an overall break-even figure that accounts for your full product mix.

What is contribution margin?

Contribution margin is the difference between your selling price per unit and your variable cost per unit. It represents the portion of each sale that goes towards covering your fixed costs and, eventually, generating profit.

What's the difference between break-even in units and break-even in revenue?

Break-even in units tells you how many items you need to sell, while break-even in revenue tells you the total sales value you need to reach. The revenue method is often more practical for service businesses or those with multiple products at different prices.

How can you reduce your break-even point?

You can lower your break-even point by reducing fixed costs, cutting variable costs per unit, or increasing your selling price. Any change that widens your contribution margin will bring your break-even point down.

Handy resources

Advisor directory

You can search for experts in our advisor directory

How to increase revenue

Find out how businesses grow their sales income.

Get more on break-even point

Learn more about break-even point and how to reduce yours.

Disclaimer

This glossary is for small business owners. The definitions are written with their requirements in mind. More detailed definitions can be found in accounting textbooks or from an accounting professional. Xero does not provide accounting, tax, business or legal advice.