Gearing ratio: what it is, how to calculate it, and why it matters

Learn what a gearing ratio is, how to calculate it, and what it means for your business's financial health.

Written by Shaun Quarton—Accounting & Finance Content Writer and Growth Marketer. Read Shaun's full bio

Published Friday 15 May 2026

Table of contents

Key takeaways

- A gearing ratio measures how much of your business is funded by debt and equity, helping you understand your financial risk at a glance.

- Lenders and investors use gearing ratios to assess whether your business can handle additional borrowing or represents a sound investment.

- A ratio below 25% is generally considered low gearing, 25–50% is moderate, and anything above 50% signals high gearing, though the right level depends on your industry.

- You can improve your gearing ratio by paying down high-interest debt, retaining more profits, or attracting new equity investment.

What is a gearing ratio?

A gearing ratio is a financial metric that compares your business's debt to its equity, showing how much of your funding comes from borrowing versus ownership. In simple terms, it tells you the balance between money you've borrowed and money you or your shareholders have invested directly.

Lenders look at your gearing ratio to decide whether your business can take on more borrowed funds safely. A higher ratio suggests you're already carrying significant debt, which may make further lending riskier. Investors use it too; they want to know how much financial risk they'd be taking on by backing your business.

Your gearing ratio also gives you a clear picture of your own financial position. It helps you understand whether your business relies too heavily on debt or has a healthy balance of funding sources.

Why does your gearing ratio matter?

Your gearing ratio affects several important business decisions, from how you fund growth to how others see your financial stability. Here's why it's worth tracking.

When you approach a bank or lender for a loan, your gearing ratio is one of the first things they'll check. A lower ratio generally means you're more likely to secure funding at favourable terms, while a higher ratio could limit your options or increase your interest rates.

Investors also pay close attention to gearing. If you're looking to attract outside investment, a moderate gearing ratio signals that you're managing your finances responsibly without over-relying on debt. This builds confidence that their capital won't be swallowed up by repayments.

From a planning perspective, knowing your gearing ratio helps you make smarter choices about how to fund new projects or expansion. It also plays a role in cash flow management; high debt repayments can squeeze your cash flow, making it harder to cover day-to-day expenses.

Finally, your gearing ratio is a useful risk indicator. Tracking it over time helps you spot trends early and adjust your financial strategy before problems build up.

Types of gearing ratios

There are several ways to measure gearing, and each ratio highlights a slightly different aspect of your financial structure. Here are the most commonly used types.

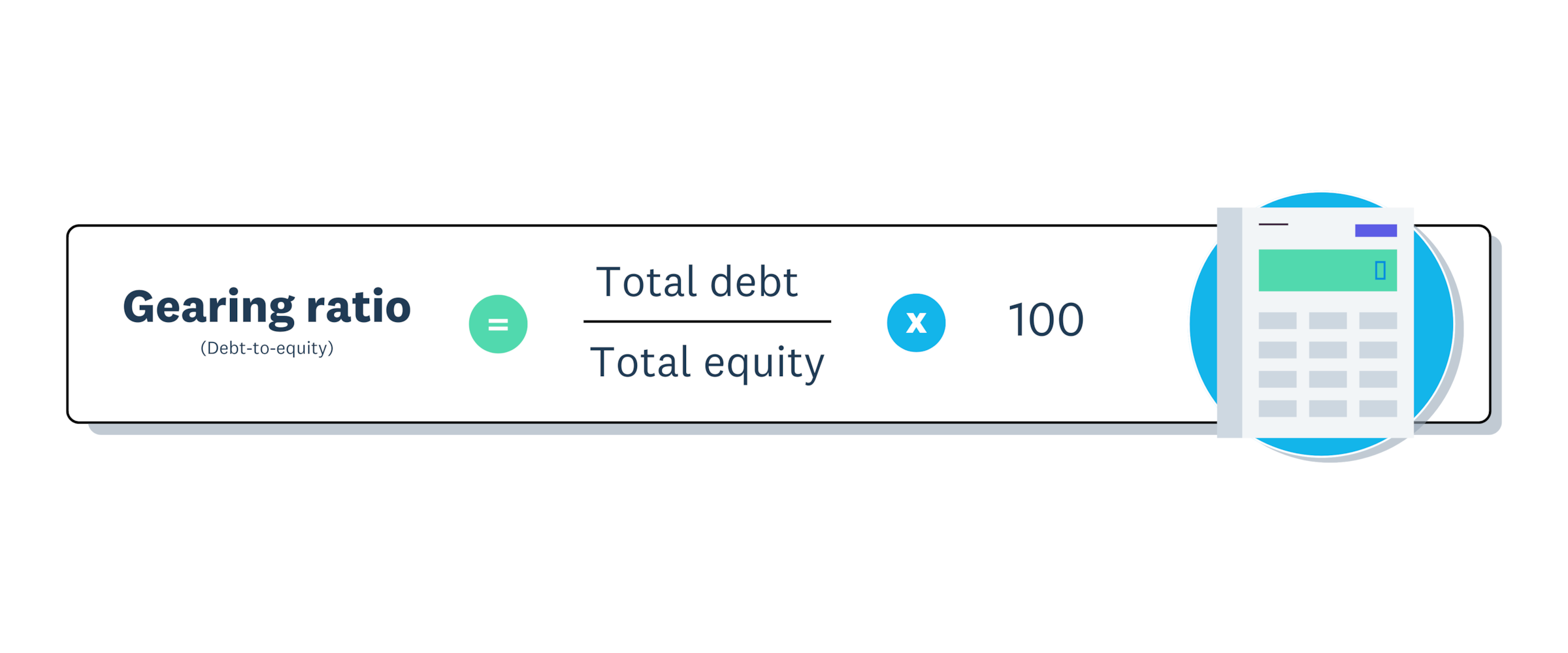

The debt-to-equity ratio (D/E) is the most widely recognised gearing measure. It divides your total debt by total equity, giving you a direct comparison of borrowed funds against ownership capital.

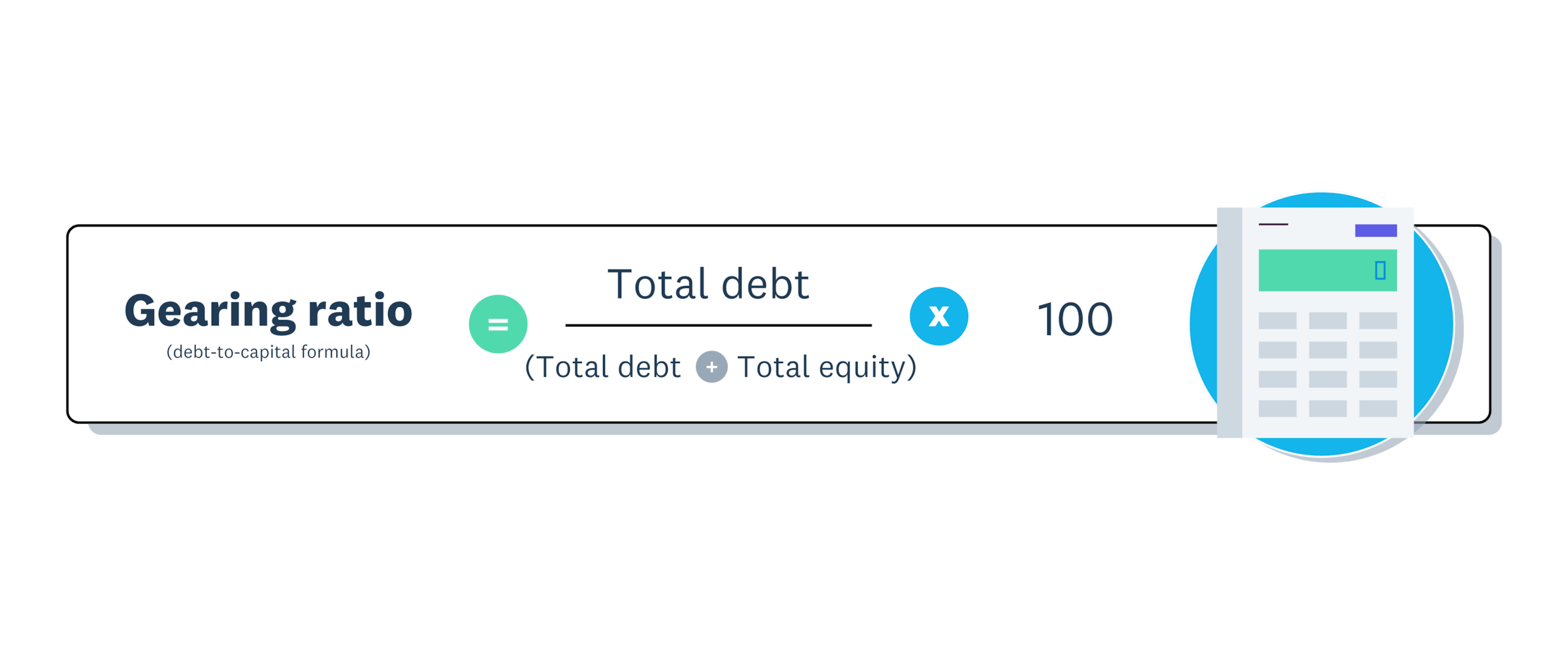

The debt-to-capital ratio takes a broader view. It divides your total debt by the sum of debt plus equity, showing what proportion of your total capital comes from borrowing.

The equity ratio measures the flip side. It divides total equity by total assets, telling you what share of your assets is funded by owners rather than creditors.

The times interest earned ratio (TIE) focuses on your ability to meet interest payments from your earnings. It divides your earnings before interest and tax (EBIT) by your total interest expense. The Association of Chartered Certified Accountants (ACCA) includes TIE in its standard ratio analysis framework, making it a well-established measure for assessing debt sustainability.

How to calculate the gearing ratio

Calculating your gearing ratio is straightforward once you have the right figures from your financial statements. Follow these four steps to work out your debt-to-equity ratio.

- Identify your total debt. Add up all short-term and long-term liabilities, including loans, overdrafts, and any other borrowing.

- Identify your total equity. Find your shareholders' equity on your balance sheet. This includes share capital, retained earnings, and any reserves.

- Apply the formula. Divide your total debt by your total equity. The formula is: gearing ratio = total debt / total equity.

- Convert to a percentage. Multiply the result by 100 to express your gearing ratio as a percentage.

For example, if your business has £50,000 in total debt and £100,000 in equity, your D/E gearing ratio would be 50% (£50,000 / £100,000 x 100).

Example gearing ratio calculations

Seeing the formulas in action makes them easier to understand. Here are two worked examples using different gearing ratios.

Example 1: debt-to-equity ratio

A small retail business has £50,000 in total debt and £100,000 in total equity. Using the debt-to-equity formula, you'd calculate this as follows.

Gearing ratio = £50,000 / £100,000 = 0.5, or 50%.

This means the business has 50p of debt for every £1 of equity. At 50%, it sits at the upper end of moderate gearing.

Example 2: debt-to-capital ratio

The same business can also calculate its debt-to-capital ratio. Total debt is still £50,000, and total capital is £150,000 (£50,000 debt + £100,000 equity).

Debt-to-capital ratio = £50,000 / £150,000 = 0.33, or 33%.

This tells you that 33% of the business's total funding comes from debt, while the remaining 67% comes from equity.

How to interpret your gearing ratio

Your gearing ratio only becomes useful when you understand what the numbers mean for your specific situation. Here's a general breakdown of what different levels indicate.

Low gearing (below 25%) means your business is mainly funded by equity. This suggests lower financial risk because you have fewer debt repayments to meet. However, it could also mean you're not making the most of available financing to grow.

Moderate gearing (25–50%) is often seen as a healthy balance. You're using some debt to fund growth while keeping repayments manageable. Many lenders and investors view this range positively.

High gearing (above 50%) indicates a heavier reliance on borrowing. While this isn't always a problem, particularly in capital-intensive industries, it does carry more risk. If your revenue drops, high debt repayments could put pressure on your cash flow.

Keep in mind that "good" gearing varies by industry. A construction company will naturally carry more debt than a consultancy. You can check how your ratio compares to others in your sector using resources like Industry Watch.

Factors that influence your gearing ratio

Several factors can push your gearing ratio higher or lower, and not all of them are within your direct control. Understanding these influences helps you plan ahead.

Economic conditions play a significant role. During periods of low interest rates, borrowing becomes cheaper, and many businesses take on more debt. When rates rise, the cost of servicing that debt increases, which can shift your gearing ratio and strain your cash flow.

Capital allocation decisions directly affect your balance of debt and equity. Choosing to fund a new project through a loan rather than retained profits will increase your gearing. Similarly, distributing large dividends reduces your equity base and pushes the ratio up.

Industry norms shape what's considered an acceptable level of gearing. Manufacturing, property, and infrastructure businesses typically carry higher debt because they need expensive assets. Service-based businesses usually operate with lower gearing because they have fewer capital requirements.

Your business lifecycle stage also matters. Start-ups and early-stage companies often have higher gearing because they haven't yet built up significant retained earnings. As a business matures and accumulates profits, its equity base grows and gearing tends to fall.

High versus low gearing: what's the difference?

The difference between high and low gearing comes down to how much of your business is funded by debt compared to equity. Two businesses in different situations can illustrate this clearly.

High gearing example: a retail store

A retail store takes out a large loan to open a second location. Its total debt rises to £200,000 against equity of £100,000, giving it a gearing ratio of 200%. The shop now relies heavily on monthly repayments. If sales dip during a quiet season, meeting those repayments becomes a real challenge.

Low gearing example: a local cafe

A local cafe funds its refurbishment using retained profits and a small personal investment from the owner. Its total debt is just £10,000 against equity of £80,000, giving it a gearing ratio of 12.5%. The cafe has very little debt pressure. It can weather a slow month without worrying about loan repayments, though it may miss out on faster growth that additional funding could provide.

What gearing ratios won't tell you

Gearing ratios are a helpful snapshot, but they don't give you the full picture of a business's financial health. It's worth knowing their limits.

A gearing ratio doesn't account for market position or competitive advantage. A company with a strong monopoly or dominant market share might sustain high gearing comfortably because its revenue streams are more predictable. The ratio alone won't reflect that stability.

Capital-intensive industries can appear riskier than they are. Businesses in sectors like utilities, transport, or manufacturing naturally carry higher debt to fund essential infrastructure. Comparing their gearing to a service-based business without considering this context would be misleading.

Gearing ratios also don't capture timing or the quality of debt. A business with mostly long-term, low-interest debt is in a different position from one with short-term, high-interest borrowing, even if both show the same ratio. You should always look at gearing alongside other measures, like your cash flow and profitability, for a more complete view.

How to manage your gearing ratio

If your gearing ratio is higher than you'd like, there are practical steps you can take to bring it down over time. The two main approaches are reducing your debt and increasing your equity.

Reduce your debt

Bringing your debt levels down is the most direct way to lower your gearing ratio. Here are some strategies to help you manage debt effectively:

- Prioritise paying off high-interest loans first, as these cost you the most over time

- Refinance existing debts to secure lower interest rates or longer repayment terms

- Avoid taking on new borrowing unless it's essential for growth or operations

- Use surplus cash to make extra repayments where your loan terms allow it

Increase your equity

Building your equity base is the other side of the equation. A stronger equity position naturally brings your gearing ratio down:

- Retain more profits in the business instead of distributing them as dividends

- Attract new investors who can contribute fresh capital

- Issue additional shares if your business structure allows it

- Focus on growing revenue and profitability, which increases retained earnings over time

A balanced approach that combines reducing debt with growing equity tends to produce the best long-term results.

Keep your business finances healthy with Xero

Tracking your gearing ratio is just one part of managing your business finances well. Staying on top of your debt levels, equity position, and cash flow helps you make smarter decisions and keeps your business in a strong position for growth.

Xero's accounting software makes it simple to monitor your financial health with real-time reporting and clear insights. You can track your income, expenses, and cash flow all in one place, giving you the visibility you need to stay in control.

Ready to get started? Get one month free and see how Xero can help you keep your finances on track.

FAQs on gearing ratio

Here are some frequently asked questions about gearing ratio to help you understand this metric better.

How often should you review your gearing ratio?

Review your gearing ratio at least quarterly, ideally alongside your other financial reports. If your business is going through a period of significant change, such as taking on new debt or raising investment, check it monthly to stay on top of any shifts.

Is there a minimum gearing ratio to aim for?

There's no universal minimum, but extremely low gearing might suggest you're missing growth opportunities that affordable borrowing could unlock. Speak with your accountant about finding the right balance for your specific circumstances.

How does taking out a new loan affect your gearing ratio?

A new loan increases your total debt, which pushes your gearing ratio higher. Before borrowing, calculate how the new debt will change your ratio relative to your existing equity so you can plan accordingly.

Do gearing ratio benchmarks vary across industries?

Yes, they vary significantly, so always compare your ratio to similar businesses in your sector. Trade associations and industry reports often publish average financial ratios that make this comparison straightforward.

How can service businesses keep their gearing ratio stable?

Service businesses can stabilise their gearing by building up retained earnings and avoiding unnecessary borrowing. Since service businesses generally have lower capital requirements, maintaining a healthy cash reserve and reinvesting profits back into the business is usually enough to keep gearing at a comfortable level.

Get one month free

Purchase any Xero plan, and we will give you the first month free.