Revenue-based financing: Is it right for your business?

Revenue-based financing is when you take loans that you repay with a portion of your revenue. Let's look at the options.

Written by Kari Brummond—Content Writer, Accountant, IRS Enrolled Agent. Read Kari's full bio

Published January 13 2026

Table of contents

Key takeaways

- Revenue-based financing refers to loans that are repaid based on revenue.

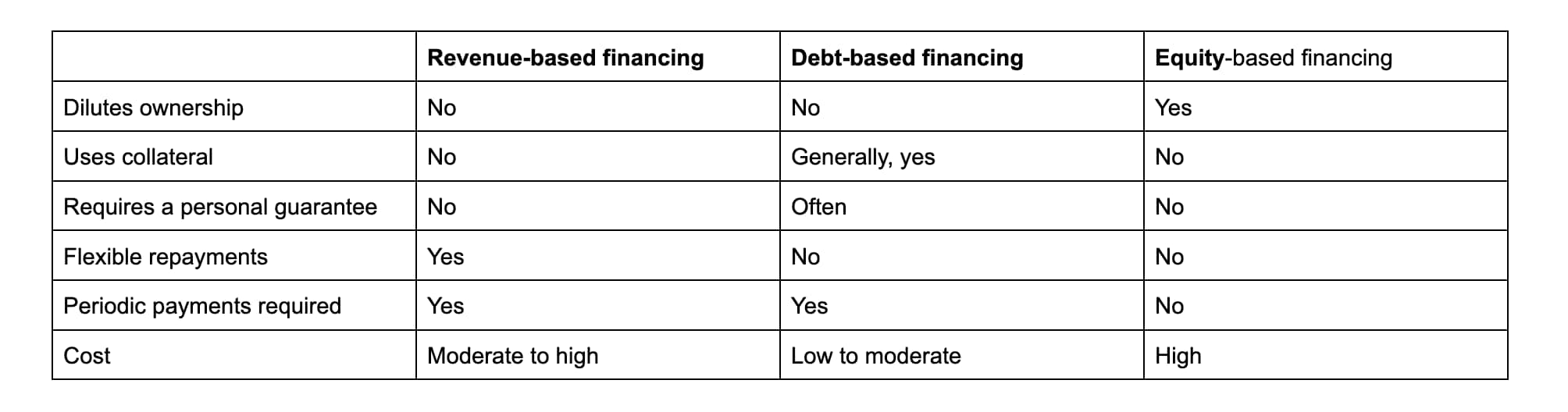

- You don't have to give up shares in the company or use assets as collateral, like you do with equity- or debt-based financing.

- One advantage of revenue-based financing is its flexibility. Repayments are based on revenue, which allows you to make lower payments when revenue drops. Repayments can also be daily or monthly.

- The downside is that these loans often have high fees – so read the fine print carefully.

What is revenue-based financing?

Revenue-based financing refers to small business loans based on revenue. These loans – also called royalty-based financing or recurring revenue loans – provide companies with cash up front and flexible repayments based on revenue.

How does revenue-based financing work?

With revenue-based funding, businesses receive upfront capital – the loan's value is based on the business's historic revenue, its recurring annual revenue, or its anticipated future revenue.

The repayment amount is typically the loan value times a multiplier, or the loan plus a fee – for example, a revenue-based loan for $1 million with a 1.5 multiplier means the business repays $1.5 million.

Repayments are always based on revenue, but the repayment structure depends on the loan's terms. For example, a revenue-based financing company focused on tech startups typically requires companies to repay a percentage of their monthly revenue. In contrast, a merchant advance – a type of revenue-based financing often used by retailers – typically asks for a daily percentage of credit card sales for repayment.

Pros and cons of revenue-based financing

Like all other types of business financing, revenue-based loans offer benefits – and a few drawbacks:

Benefits of revenue-based financing

- Cheaper than equity-based financing: Revenue-based loans often cost 10% to 50% of the loan's original value. Angel investments and similar types of equity financing, however, often end up costing between 10 and 20 times the original investment.

- Non-dilutive: You don't have to give up any ownership shares, as you do with equity-based financing.

- No personal guarantees required: Banks often ask for personal guarantees for small business loans, but revenue-based financing rarely requires a personal guarantee.

- Flexible payments: Payments are based on revenue, meaning they go up or down as your sales rise and fall.

- Fast funding: Funding ranges from instantaneous to 4 weeks, but it typically arrives sooner than most equity or debt-based loans.

Drawbacks of revenue-based financing

- Revenue required: You generally can't get revenue-based financing for startups or small businesses if you don’t already have a revenue stream.

- Periodic payments required: Revenue-based financing requires regular periodic payments; unlike equity-based financing.

- Relatively short repayment terms: Most revenue-based loans have much shorter repayment terms than most debt-based financing.

Revenue-based financing vs other options

Let's check out how revenue-based financing compares to debt vs equity-based financing:

Is revenue-based financing right for your business?

Revenue-based financing might be a good fit for you if you:

- need capital quickly

- have a proven track record or earning revenue – or have a significant amount of recurring revenue set up already

- don't want to dilute ownership

- don't qualify for debt-based financing, or don't want to deal with collateral or personal guarantees

- are comfortable with the repayment terms

As with any type of financing, it’s a good idea to consult your accountant. They can help you crunch the numbers and help you decide which type of financing is best for your business.

How to prepare your numbers and apply

Here are the basic steps to get your numbers ready and to apply for revenue-based financing:

1. Figure out how much funding you need. Then determine how much you can afford to repay as a percentage of your revenue – for a quick estimate, think about how much you have left after expenses during your lowest revenue month to date.

2. Divide that number into your monthly revenue – the result is the highest percentage you can commit to paying, without creating a loss during any month.

For example, if your lowest earning month has $100,000 in revenue and you have $10,000 left after expenses, you can afford a loan that requires up to 10% of your revenue as repayment.

3. Identify the type of lender you want to work with. The most popular options are:

- Traditional revenue-based financing: Provides a lump sum in advance; it requires repayment of the loan times a multiplier, with payments based on a percentage of sales

- Subscription-based revenue financing: Repayments are based on recurring revenue.

- Revenue-trading platforms: Businesses sell future recurring revenue streams to investors.

- Accounts receivable financing: Also called invoice factoring, involves selling invoices at a percentage of their value to a factoring company.

- Merchant cash advances: Funded by payment processing companies; repayments are a percentage of payments processed.

- Hybrid revenue-based financing: Combines revenue-based financing with equity or debt-based financing.

4. Gather financial records to convince the lender to approve your request. Depending on the type of loan, you may need sales records, profit and loss statements, cash flow reports, and projections about future revenue.

Handle your financing with Xero

Xero helps you create and keep clean financial reports – perfect for applying for any type of funding. A bank feed to your Xero organization and Xero’s automated reconciliation tools give you up-to-date, accurate books so you can easily track your revenue and expenses. Then create all the financial reports you need to apply for loans with just a few taps.

FAQs on revenue-based financing

Check out the answers to some common questions on revenue-based financing:

What is an example of revenue-based financing?

Square Loans and PayPal Working Capital are two examples of revenue-based business loans. These companies offer loans to clients who use their payment processing services – these loans are based on revenue, and the repayments are a percentage of payments processed.

Another example is a revenue-based financing company like Efficient Capital Labs, which provides revenue-based funding to SaaS companies.

How is revenue-based financing different from a merchant cash advance?

Merchant cash advances are a type of revenue-based financing. Merchant cash advances are funded by payment processing companies like Square Loans or PayPal Working Capital. Revenue-based financing can also come from a company or investor willing to offer this type of financing.

There’s a difference in the repayment method: With a merchant cash advance, repayments are usually a percentage of payments processed, but with revenue-based financing, payments are typically based on monthly revenue.

How much can I raise with revenue-based financing?

There’s a wide range. Revenue-based financing for start-ups and small businesses can range from $5,000 to $50 million or more. The amount you can raise depends on your business's current revenue, anticipated future revenue, and overall financial health.

How do I record revenue-based financing in my accounting system?

When you receive revenue-based funding, record the loan as a liability in your accounting software – a short-term liability if you expect to repay it within 12 months, or long-term one if repayment will take more than a year. Calculate which portion of each payment covers the loan's principal and which portion goes to interest or fees. Then when you make a payment, split the transaction so that you classify the portion repaying the principal to the liability account and the remaining amount as an interest or fee expense.

Why choose revenue-based financing over equity?

With the revenue-based financing model, you don't have to give anyone a piece of your company, as you do with equity-based financing. Revenue-based business loans let you keep ownership control of your company, and are often easier to get.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Get one month free

Sign up to any Xero plan, and we will give you the first month free.