Interest expense for small business: formula, tax tips

Learn how to calculate, record, and deduct business interest expenses.

Written by Kari Brummond—Content Writer, Accountant, IRS Enrolled Agent. Read Kari's full bio

Published Wednesday 27 May 2026

Table of contents

Key takeaways

- Interest expenses are the costs you pay to borrow money for your business, and tracking them accurately helps you manage cash flow and maximize tax deductions.

- You can deduct interest on business loans, credit cards, mortgages, and equipment financing, but larger businesses face limits under IRS Section 163(j).

- Interest expense shows up as a non-operating cost on your income statement, while interest payable sits on your balance sheet as a liability you still owe.

- Common mistakes like mixing personal and business interest or poor documentation can cost you deductions and create compliance headaches at tax time.

What are business interest expenses?

If your business borrows money, you're paying interest. That cost is your interest expense, and it plays a bigger role in your finances than you might think.

An interest expense is the cost of borrowing funds for business purposes. It includes what you pay on business loans, lines of credit, credit cards, and any other financing arrangements. These costs directly affect your profitability and cash flow, and they determine part of your tax bill.

Tracking interest expenses matters for three key reasons:

- Tax savings. Most business interest is tax-deductible, which lowers your taxable income.

- Financial tracking. Accurate records give you a clear picture of what debt actually costs your business.

- Cash flow management. Knowing your interest obligations helps you plan payments and avoid surprises.

When you claim interest expenses depends on your accounting method. If you use cash basis accounting, you record interest when you actually make the payment. If you use accrual accounting, you record it when the interest is incurred, regardless of when you pay.

Types of interest expenses

Not all interest expenses are the same. The type depends on the borrowing arrangement, and each has its own considerations for how you track and deduct it.

Loan interest

This is the most common type for small businesses. It covers interest on term loans, SBA loans, lines of credit, and equipment financing. Loan interest is typically calculated on the outstanding principal balance and may be fixed or variable.

Credit card interest

When you carry a balance on a business credit card, you pay interest on the unpaid amount. Credit card rates tend to be higher than loan rates. For example, at a 21% annual rate, a $10,000 balance would cost you $2,100 in interest over a year.

Capitalized interest

If you borrow money to build or produce a long-term asset, the interest incurred during construction gets added to the asset's cost rather than expensed immediately. This is called capitalized interest. You'll recover it over time through depreciation.

Bond interest

Larger small businesses that issue bonds pay periodic interest to bondholders. This interest is typically paid at a fixed rate on a set schedule and is recorded as an expense each period.

Interest expense vs interest payable

These two terms sound similar, but they represent different things on your financial statements. Understanding the distinction helps you keep your books accurate.

Interest expense is the cost of borrowing during a specific period. It appears on your income statement and reduces your net income. Interest payable, on the other hand, is the amount of interest you've incurred but haven't paid yet. It sits on your balance sheet as a current liability.

Here's a quick example. Say you have a loan with $500 in interest due on the 15th of next month. On the last day of this month, you'd record $500 as interest expense on your income statement (because you've incurred the cost) and $500 as interest payable on your balance sheet (because you haven't paid it yet). Once you make the payment, the interest payable balance drops to zero.

How to calculate interest expenses

Calculating interest expense is straightforward. Getting it right helps you budget accurately and avoid surprises on your financial statements.

1. Use the basic interest formula

The formula is: interest expense = principal x interest rate x time period.

Say you take out a $35,000 business loan at a 10% annual interest rate. Your annual interest expense would be:

$35,000 x 0.10 x 1 = $3,500 per year

To find the monthly interest expense, divide by 12:

$3,500 / 12 = $291.67 per month

2. Factor in changing balances

With most loans, the principal balance decreases over time as you make payments. That means your interest expense also decreases with each payment, since it's calculated on the remaining balance.

3. Use your lender's tools for precision

The formula gives you a solid estimate, but real-world calculations can be more complex. Factors like compounding frequency, variable rates, and amortization schedules all affect the final number.

For accuracy, consider using an online loan interest calculator, your lender's amortization schedule, or the interest figures from your loan statements. When it's time to file taxes, you'll report interest expenses on the appropriate IRS form: Schedule C for sole proprietors, Form 1065 for partnerships, Form 1120S for S corporations, or Form 1120 for C corporations.

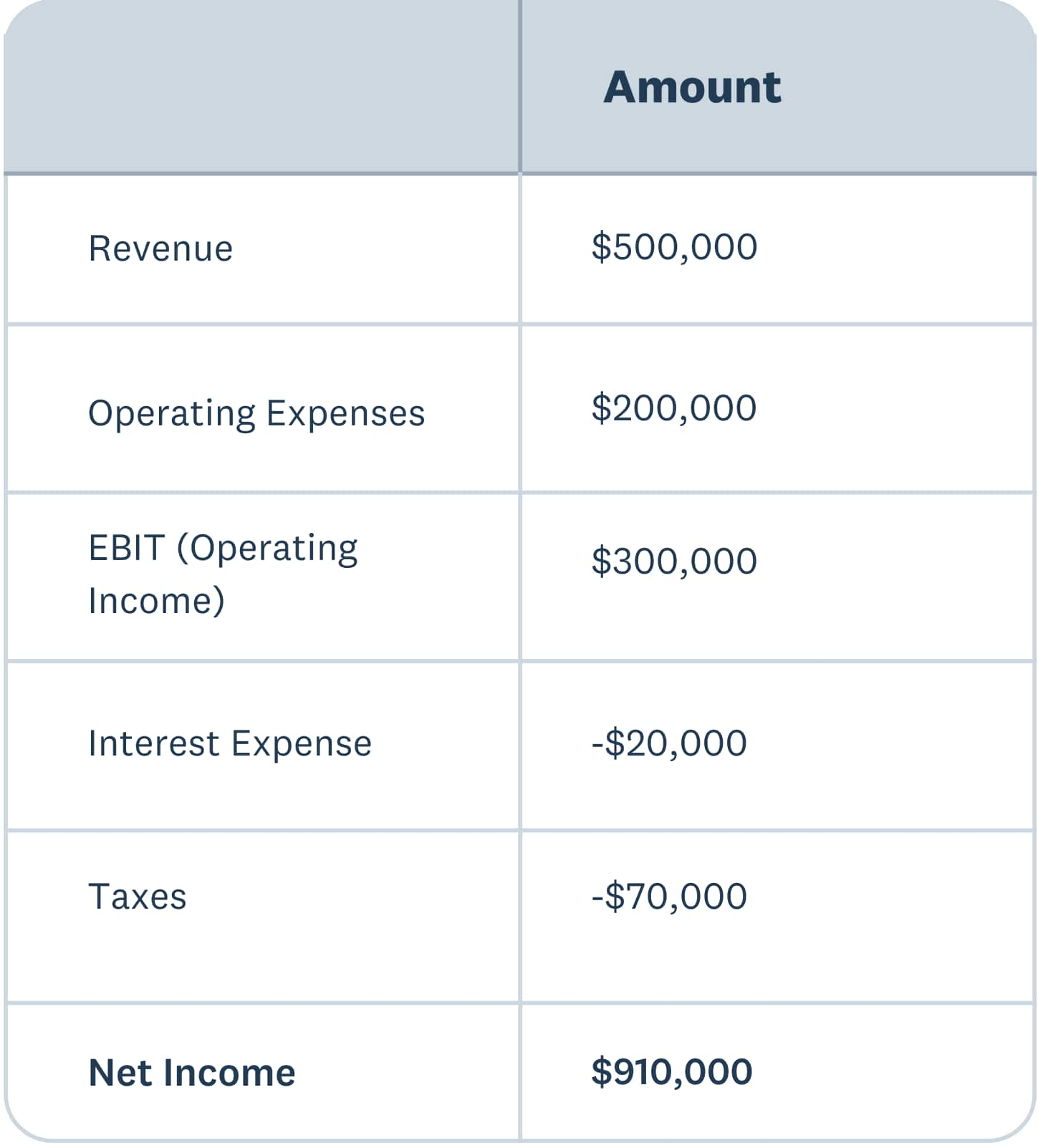

Interest coverage ratio

Your interest coverage ratio tells you how comfortably your business can pay its interest obligations from operating earnings. It's a useful indicator of financial health, especially if you're carrying significant debt.

The formula is:

Interest coverage ratio = EBIT / interest expense

EBIT stands for earnings before interest and taxes. Let's say your business earns $120,000 in EBIT and pays $20,000 in interest expense. Your interest coverage ratio would be:

$120,000 / $20,000 = 6.0

A ratio of 6.0 means you earn six times more than you need to cover your interest payments. Generally, a ratio above 3.0 is considered healthy for small businesses. A ratio below 1.5 signals that you may struggle to meet interest obligations, which could make it harder to qualify for additional financing.

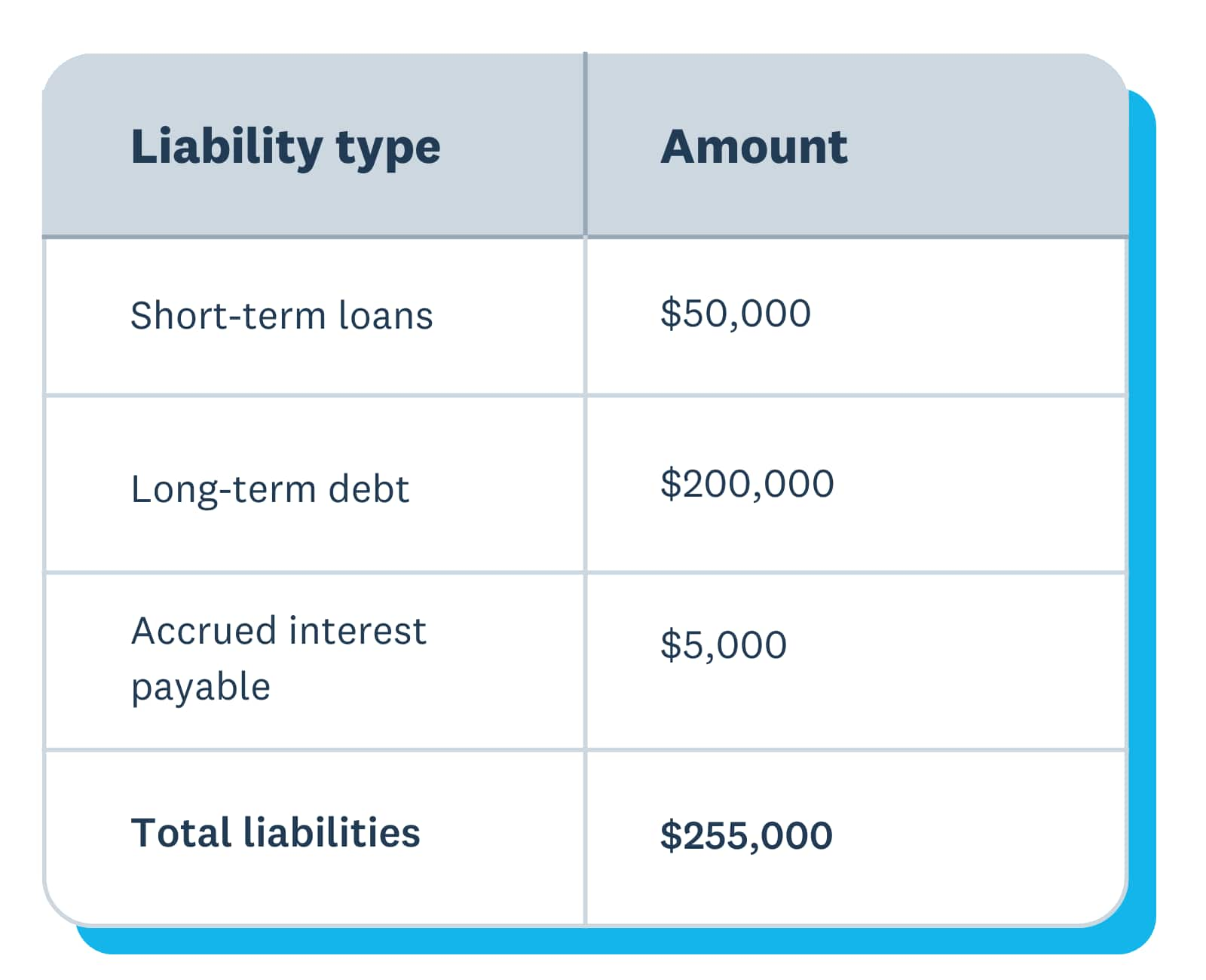

How interest expenses appear on your financial statements

Interest expenses show up across multiple financial statements. Knowing where to look and what to record keeps your books in good shape and your tax filings accurate.

On your profit and loss statement (income statement), interest expense appears as a non-operating expense below your operating income. It reduces your pre-tax profit but is listed separately from day-to-day business costs like rent and payroll.

On your balance sheet, you'll see interest-related items in the liabilities section. Accrued interest (interest you've incurred but not yet paid) shows up as a current liability. For example, a business might report a $200,000 long-term loan balance, $5,000 in accrued interest payable, and $50,000 in short-term loan obligations.

Your cash flow statement captures interest payments in the operating activities section. Here's where the split between interest and principal matters.

Say you make a $2,000 monthly loan payment. If $500 goes to interest and $1,500 goes to principal, only the $500 interest portion appears as an operating cash outflow. The $1,500 principal repayment shows up under financing activities.

This distinction is important because it affects how your cash flow looks to lenders and investors. Your total cash goes down by $2,000, but each portion is categorized differently on the statement.

Is interest expense an operating expense?

Interest expense is not an operating expense. This is a common point of confusion, but the distinction matters for financial reporting.

Operating expenses are the costs directly related to running your core business: rent, wages, supplies, marketing, and similar items. Interest expense, by contrast, is a financing cost. It results from how you fund your business, not from how you operate it.

On your income statement, interest expense appears below the operating income line. This placement makes it clear that it's separate from the costs of your daily operations. It reduces your net income but doesn't affect your operating profit.

One exception worth noting: banks and financial institutions treat interest expense as an operating cost because lending and borrowing are their core business activities. For most small businesses, though, interest remains a non-operating expense.

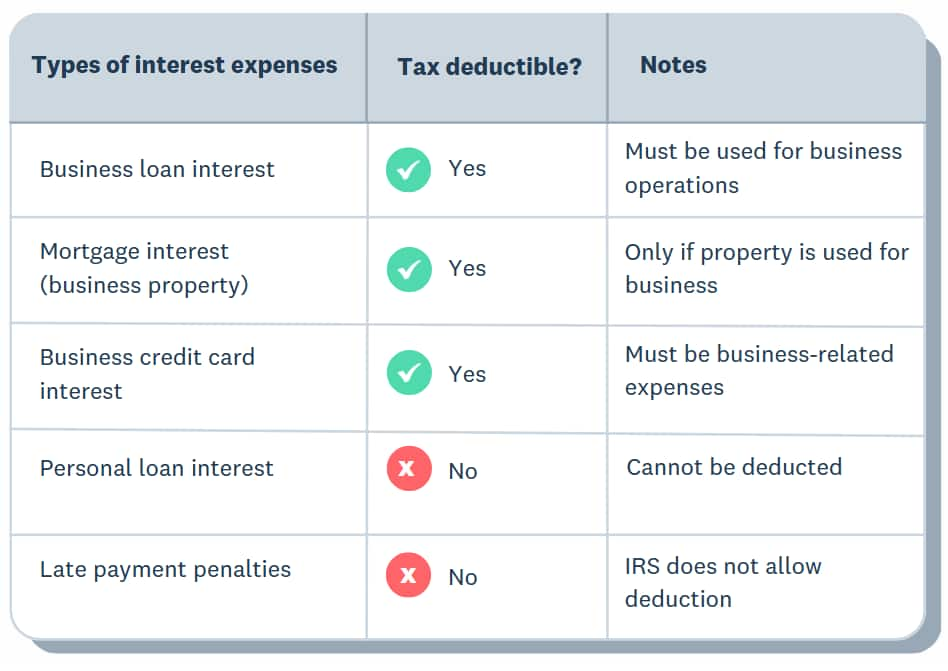

Which interest expenses you can claim as tax deductions

Deducting interest expenses can meaningfully lower your tax bill. The key is knowing what qualifies and staying within the limits the IRS sets.

You can generally deduct interest on borrowing used for business purposes, including:

- Business term loans: includes lines of credit

- Commercial mortgages: on business property

- Business credit cards: only the portion used for business expenses

- Equipment financing: includes capital leases

- SBA loans: and other government-backed business lending

Personal interest, such as your home mortgage or personal credit card debt, isn't deductible as a business expense. If you use a credit card for both personal and business purchases, only the business portion of the interest qualifies.

For most small businesses, there's no cap on how much interest you can deduct. However, larger businesses face limits under IRS Section 163(j). This rule limits the business interest deduction to 30% of adjusted taxable income (ATI) for businesses with average annual gross receipts exceeding $32 million in 2026 ($31 million for 2025).

For tax years beginning after December 31, 2024, the One Big Beautiful Bill Act restored the EBITDA-based calculation for ATI. This means businesses can once again add back depreciation, amortization, and depletion when calculating their deduction limit. The stricter EBIT-based rules that applied from 2022 through 2024 no longer apply for current tax years.

Understanding the broader economic context can help you anticipate how interest expenses may shift. The Federal Reserve held its target rate at 3.5% to 3.75% as of early 2026, following rate cuts in late 2025. For small businesses carrying variable-rate debt, these rate changes directly affect how much interest expense you can expect to pay and deduct.

To maximize your interest deductions, keep these tips in mind:

- Keep clear records. Save loan agreements, statements, and payment receipts.

- Separate personal and business borrowing. Mixed-use debt complicates your deduction.

- Time your payments strategically. If you're on cash basis, paying interest before year-end increases your current-year deduction.

- Review variable-rate loans regularly. Rate changes can shift your interest costs and deduction amounts.

Avoid common mistakes with interest expenses

Even experienced business owners make errors with interest expenses. Avoiding these five common mistakes will save you time, money, and potential issues with the IRS.

Incorrect classification

Recording interest expense in the wrong category throws off your financial statements. If you've classified it as an operating expense, that inflates your operating costs and distorts profitability ratios, which can affect lending decisions.

Poor documentation

Without proper records, you risk losing deductions entirely. Keep copies of loan agreements, interest statements, and payment confirmations. If the IRS questions a deduction and you can't back it up, you'll lose it.

Ignoring deduction limits

If your business is approaching the Section 163(j) gross receipts threshold, you need to pay attention to the 30% ATI limitation. Claiming more than you're allowed can trigger penalties and interest on the underpayment. Work with a tax professional if your gross receipts are near $31 million (2025) or $32 million (2026).

Paying too much interest

Accepting the first loan offer you receive can cost you thousands in unnecessary interest. Shop around for competitive rates, consider refinancing high-interest debt, and negotiate terms with your lender. Even a small rate reduction on a large balance adds up significantly over time.

Mixing personal and business interest

Using a personal credit card or loan for business expenses creates a messy situation at tax time. You can only deduct the business portion, and proving that split without clear records is difficult. Keep separate accounts for business and personal borrowing to make tracking expenses and deductions straightforward.

Take control of your interest expenses

Staying on top of interest expenses helps you make smarter borrowing decisions and claim every deduction you're entitled to. The right tools make this easier by tracking your expenses automatically and giving you a clear view of what debt is costing your business.

Xero's accounting software helps you manage interest expenses alongside the rest of your finances, so you always know where you stand. Try it out and get one month free.

FAQs on interest expenses

Here are answers to frequently asked questions about interest expenses.

How do interest expenses affect my cash flow?

Interest payments reduce the cash available for other business needs like inventory, payroll, and growth investments. When interest rates rise or you take on more debt, your monthly cash outflows increase, so monitoring interest costs against incoming revenue helps you avoid cash crunches.

Is interest expense a debit or a credit?

When you record interest expense, it's a debit to the interest expense account (increasing the expense) and a credit to either cash (if you paid it) or interest payable (if it's accrued but unpaid). This follows standard double-entry bookkeeping principles.

How do different loan structures affect interest expenses?

Fixed-rate loans lock in predictable interest costs, while variable-rate loans fluctuate with market conditions, potentially raising or lowering your expense. When choosing a loan structure, consider how long you plan to carry the debt and how much payment variability your cash flow can handle.

Can I carry forward interest expenses to future tax years?

Yes, if your business interest deduction is limited under Section 163(j), the disallowed portion carries forward indefinitely to future tax years. You can deduct the carried-forward amount in any year when you have enough adjusted taxable income capacity, so a limitation in one year doesn't permanently eliminate the deduction.

What is accrued interest and how should I record it?

Accrued interest is interest that has built up on a loan but hasn't been paid yet. If you use accrual accounting, record it as an adjusting entry at the end of each period (debit interest expense, credit interest payable), then reverse the payable when you make the payment.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Get one month free

Sign up to any Xero plan, and we will give you the first month free.