NOPAT: formula, meaning and examples for small businesses

Learn what NOPAT shows about your profit and how it helps you make smarter business decisions.

Written by Kari Brummond—Content Writer, Accountant, IRS Enrolled Agent. Read Kari's full bio

Published Wednesday 22 April 2026

Table of contents

Key takeaways

- Calculate NOPAT by multiplying your operating profit by (1 minus your tax rate) to get a clear picture of how much profit your core business activities generate after taxes, excluding any interest on debt.

- Use NOPAT to compare your business fairly against competitors, as it removes the distorting effect of different debt levels and financing structures that can make net profit misleading.

- Apply NOPAT to calculate Economic Value Added (EVA) by subtracting your total capital costs from NOPAT, which tells you whether your invested capital is generating returns above what it costs to fund the business.

- Track operating income and expenses systematically, excluding non-operating items like investment gains or rental income, to make sure your NOPAT calculations stay accurate over time.

Key takeaways

Here are the key points about NOPAT:

- Calculate NOPAT by multiplying operating profit by (1 - tax rate) to measure core business performance after taxes

- Compare businesses fairly using NOPAT regardless of debt levels or financing structures

- Apply NOPAT to EVA calculations to determine whether invested capital generates returns above its cost

- Track operating income and expenses systematically to ensure accurate NOPAT calculations over time

Now that you know the key points, let's explore NOPAT in detail.

What is NOPAT?

Net Operating Profit After Tax (NOPAT) measures how much profit your core business operations generate after taxes but before interest expenses. It excludes non-operating income like investment gains and focuses only on your main business activities.

NOPAT helps you evaluate operational performance by:

- excluding non-operating income: removes stock gains, investment returns, and side business revenue

- excluding financing costs: removes interest on loans, credit cards, and debt payments

- including tax obligations: reflects real-world tax burden on operations

UK businesses using the cash basis method have a maximum claim for interest and related costs of £500 under current tax rules.

NOPAT also links directly to how you value a business, as it feeds into methods such as purchase price allocation.

Why is NOPAT important?

NOPAT reveals true operational efficiency by removing financing structure bias from your profit calculations. This metric helps you:

- compare businesses fairly: evaluate companies regardless of debt levels or tax jurisdictions

- assess core performance: focus on operational success rather than financing decisions

- make investment decisions: understand returns from actual business activities

Reveals true business performance

NOPAT isolates operational performance from financing decisions. It shows how well your business generates profit from core activities while accounting for tax obligations.

This metric is especially useful for evaluating businesses with complex financial structures. Valuation experts Stern Stewart have noted that some companies require 160 adjustments to accounting profits to arrive at NOPAT. Understanding your operational profits helps you identify areas for improvement and plan for long-term growth.

Helps to standardise comparisons

NOPAT standardises comparisons between companies regardless of their location or capital structure. Even when a business has debt that reduces net profit and tightens cash flow, NOPAT reveals how strong its core operations are.

This metric also helps you compare how tax rules in different areas affect profitability. For example, UK businesses can earn up to £1,000 in miscellaneous income tax-free under the trading income allowance.

Here's how NOPAT reveals operational strength that net profit alone might miss:

- Company A: £100,000 net profit

- Company B: £80,000 net profit (but £120,000 NOPAT)

Company B's higher NOPAT reveals stronger operational performance despite lower net profit due to debt payments. This insight helps you evaluate the business's true earning potential.

Make better decisions

NOPAT enables Economic Value Added (EVA) calculations to measure whether your invested capital generates returns above its cost. Stern Stewart & Co identified 164 performance measurement issues in calculating EVA from published accounts.

EVA formula: NOPAT - (total invested capital × cost of capital)

Here's a practical example showing how to calculate EVA using NOPAT:

- Start with NOPAT: £50,000

- Calculate total invested capital: £100,000 in loans + £100,000 owner investment = £200,000

- Determine average cost of capital: loans at 6% interest, blended rate of 3%

- Subtract capital cost from NOPAT: £50,000 - £6,000 = £44,000 EVA

This means the £200,000 invested in this company generates £44,000 per year above its cost. EVA becomes especially important when multiple shareholders need to see how well their investments are performing. Check out EVA calculation examples for more detail.

NOPAT formula explained

Use this formula to calculate NOPAT for your business.

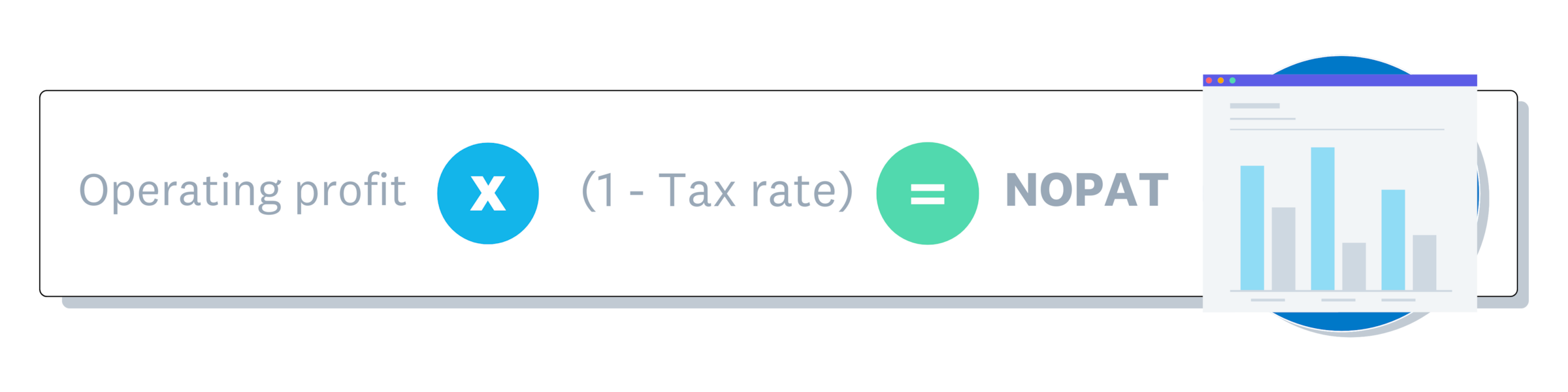

NOPAT = operating profit × (1 - tax rate)

Here's how the calculation breaks down:

- Start with operating profit: revenue minus all operating expenses (including depreciation and amortisation)

- Calculate tax impact: multiply by (1 - tax rate) to find after-tax profit

- Result: operating profit adjusted for taxes but excluding interest

For example, if your tax rate is 20%, multiply operating profit by 0.80 to get NOPAT.

A note on operating profit vs EBIT: These terms are often used interchangeably, but there's a slight difference. EBIT includes all income sources, while operating profit only includes income from your main line of business.

How to calculate NOPAT

Follow these steps to calculate NOPAT for your business.

1. Determine operating profit

Calculate operating profit using these formulas:

- Gross profit: revenue - cost of goods sold

- Operating profit: gross profit - operating expenses

Exclude any non-operating income like investment gains or asset sales.

2. Find the tax rate

Tax rate = income tax paid ÷ operating profit

For example: £20,000 tax ÷ £100,000 operating profit = 20% tax rate

If you expect higher earnings this year, your effective tax rate may increase. If your gross income exceeds £1,000, you must register for Self Assessment by 5 October in the following tax year. Check Business taxes on GOV.UK to estimate your rates.

3. Apply the formula

Here's an example using sample figures:

- Operating profit: £50,000

- Tax rate: 25%

NOPAT = £50,000 × (1 - 0.25) = £37,500

This means your business generates £37,500 in after-tax operational profit, excluding any financing costs or non-operating income.

NOPAT examples for small businesses

Seeing NOPAT in action helps you understand how it applies to your own business. Let's look at a practical example of a small retail shop.

Imagine you run a boutique clothing store. Your total revenue for the year is £200,000, and your operating expenses (like rent, wages, and inventory) are £150,000. This leaves you with an operating profit of £50,000.

You also have a small business loan that costs you £5,000 in interest each year, and your tax rate is 20%.

To find your NOPAT, you ignore the £5,000 interest payment. You simply take your £50,000 operating profit and multiply it by 0.80 (which is 1 minus your 20% tax rate). Your NOPAT is £40,000.

This £40,000 shows exactly how much profit your shop's core operations generated after taxes, giving you a clear picture of your retail success without the distraction of your loan costs.

NOPAT vs net income

NOPAT and net income measure different aspects of profitability. Net income shows your total bottom line, while NOPAT focuses only on core operational profit.

Here are the key differences between NOPAT and net income:

- Net income: includes all income, expenses, taxes, and financing costs

- NOPAT: excludes interest expenses and non-operating items

Net income accounts for everything: operational expenses, interest, depreciation, amortisation, taxes, and income from side activities or investments (such as gross rental income, which may have its own tax-free allowances). NOPAT strips away interest and non-operating items to reveal only your core business performance.

Here's how to calculate NOPAT from net income using a bakery example:

- Start with net income: £100,000

- Subtract non-operating income: £12,000 rental income from car park (not a core bakery activity)

- Add back interest expense: £8,000 in loan interest

- Result: NOPAT of £96,000

NOPAT focuses on operational efficiency, while net income includes everything. If a business has no debt or other income streams, its NOPAT and net income will be the same.

Operating profit vs NOPAT

These two metrics are closely related but have an important distinction.

Operating profit and NOPAT both measure core operational earnings but differ in their treatment of taxes:

- Operating profit: before taxes and interest

- NOPAT: after taxes but before interest

To convert NOPAT to operating profit: add the tax back in.

For example, if NOPAT is £80,000 and tax liability is £16,000, operating profit equals £96,000.

NOPAT vs EBIT

NOPAT and EBIT both help you measure your operating profitability, but they look at taxes differently.

Here's what each metric measures:

- EBIT: Earnings before interest and taxes

- NOPAT: Net operating profit after tax

EBIT shows you how much money your business makes from its core operations before you pay any taxes or interest. It's a great way to see your raw earning power.

NOPAT takes EBIT one step further by subtracting your tax obligations. This gives you a more realistic view of the cash your operations actually generate, as taxes are an unavoidable cost of doing business.

NOPAT vs EBITDA

Earnings before interest, taxes, depreciation, and amortisation (EBITDA) is another popular metric, but it serves a different purpose than NOPAT.

Here's how they differ:

- EBITDA: Ignores taxes, interest, and the wear and tear on your assets

- NOPAT: Includes depreciation and amortisation, and accounts for taxes

EBITDA is often used to quickly estimate cash flow because it adds back non-cash expenses like depreciation. However, it doesn't reflect the real cost of replacing your equipment or paying your tax bill.

NOPAT gives you a more accurate picture of your true operational profitability. By including depreciation and taxes, NOPAT shows you what's actually left over to reinvest in your business or pay your investors.

Streamline your NOPAT analysis with Xero

Xero simplifies NOPAT analysis by automatically tracking the financial data you need. The platform helps you:

- track operating income and expenses: automate categorisation for accurate calculations

- generate financial reports: access profit and loss statements instantly to prepare for evolving compliance standards, such as the FRS 102 requirement for small entities to provide disclosure about related party transactions starting in 2026

- monitor tax obligations: keep tax rate calculations current and accurate

Get one month free to streamline your financial analysis and make NOPAT calculations effortless.

FAQs on NOPAT

Here are answers to common questions about calculating and using NOPAT.

Is NOPAT the same as EBIT?

No. NOPAT is operating profit after taxes, while EBIT is operating profit before taxes. Use NOPAT when you need to see profitability with tax obligations factored in.

How do you convert EBIT to NOPAT?

NOPAT = EBIT × (1 - tax rate). Multiply your EBIT by one minus your tax rate to find your net operating profit after tax.

What's the difference between NOPAT and FCFF?

NOPAT measures operating profit after tax, while FCFF (Free Cash Flow to the Firm) shows the actual cash available to all investors after accounting for capital investments. NOPAT is the starting point for calculating FCFF.

Is NOPAT the same as ROIC?

No, they measure different things. NOPAT is a pound value showing your after-tax operating profit. Return on invested capital (ROIC) is a percentage that measures how efficiently you use your capital to generate that profit. You actually use NOPAT to calculate ROIC by dividing your NOPAT by your invested capital.

When should small businesses use NOPAT?

Use NOPAT when you need to:

- compare your core operational performance against competitors without debt financing effects

- evaluate potential investments based on operational efficiency

- assess how well your business runs before interest costs

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Get one month free

Purchase any Xero plan, and we will give you the first month free.