Accumulated depreciation: what it is and how to calculate

Learn what accumulated depreciation means, how to calculate it, and how it helps you track asset value.

Written by Lena Hanna—Trusted CPA Guidance on Accounting and Tax. Read Lena's full bio

Published Tuesday 21 April 2026

Table of contents

Key takeaways

- Recognize that accumulated depreciation is a contra asset, not a liability or expense, meaning it reduces your asset's book value on the balance sheet without representing money you owe or need to repay.

- Calculate accumulated depreciation using the straight-line formula (asset cost minus salvage value, divided by useful life) to build a depreciation schedule that shows exactly how much value your assets have lost each year.

- Track depreciation expenses to reduce your taxable income, keeping more cash in your business while supporting accurate financial reporting for lenders and planning future asset replacements.

- Record each depreciation entry by debiting Depreciation Expense and crediting Accumulated Depreciation, then remove the accumulated depreciation from your balance sheet when you sell the asset to calculate any gain or loss.

What is accumulated depreciation?

Accumulated depreciation is the total amount an asset has depreciated since you bought it. It tracks how much value your asset has lost over time and shows your asset's book value, or what it's actually worth today.

The formula: asset cost minus accumulated depreciation equals current book value.

For example:

- Office furniture costing $5,000 with $1,000 depreciation each year (assuming a five-year useful life and no salvage value). After three years, accumulated depreciation is $3,000 and the book value is $2,000.

- Machinery costs $25,000, with $2,500 depreciation each year (assuming a 10-year useful life and no salvage value). After six years it has depreciated by $15,000, leaving a book value today of $10,000.

Why understanding accumulated depreciation matters for small businesses

Tracking accumulated depreciation helps you make smarter decisions about your assets and finances. Here are three key benefits:

- Better planning: Track asset values to plan replacements and budget for maintenance

- Tax savings: Depreciation expenses may reduce taxable income where tax law allows deductions, such as rules allowing businesses to claim 20% of the cost of new assets upfront, keeping more cash in your business

- Easier financing:Updated fixed asset records can help support financial reporting and lender discussions

Is accumulated depreciation an asset or a liability?

Accumulated depreciation is a contra asset, not an asset, liability, or expense. A contra asset account works like a negative number that offsets your asset's original cost, showing its realistic current value.

This means:

- It's a contra asset: It reduces the value of assets on your balance sheet

- It isn't a liability: You don't owe money or have an obligation to repay it

- It isn't an asset: It doesn't add value to your business

- It differs from depreciation expense: Depreciation expense appears on your income statement each period

On your balance sheet, you'll see accumulated depreciation listed under assets with a negative value, giving you a more realistic view of what your assets are actually worth.

Depreciation vs accumulated depreciation

Depreciation is a periodic expense; accumulated depreciation is the running total. They work together but serve different purposes:

- Depreciation: Records the expense each period (monthly or yearly) showing how much value an asset lost

- Accumulated depreciation: Tracks the running total of all depreciation expenses since you bought the asset

Depreciation is like a monthly payment, while accumulated depreciation is your total payments to date.

Here's more information about depreciation.

How accumulated depreciation affects your financial statements

Accumulated depreciation appears on three key financial statements. Each statement uses it differently to show your business's financial position.

Accumulated depreciation on the balance sheet

Accumulated depreciation reduces an asset's book value on the balance sheet. Your balance sheet shows the asset's original purchase price, and accumulated depreciation reduces this amount to show what the asset is worth today.

Accumulated depreciation on the income statement

Depreciation expense reduces your taxable income on the income statement. As a non-cash expense, it lowers your profits without affecting cash flow.

Accumulated depreciation on the cash flow statement

Depreciation is added back to net income on the cash flow statement because it doesn't affect actual cash. This adjustment reflects that depreciation is an accounting expense, not a cash outflow.

Journal entries for accumulated depreciation

The journal entry for accumulated depreciation debits Depreciation Expense and credits Accumulated Depreciation. This entry moves numbers between two accounts each time you record depreciation.

To record depreciation in your books, you'll make a journal entry. Each time you record depreciation, you:

- Debit Depreciation Expense: Increases your expenses for the period, reducing your taxable income

- Credit Accumulated Depreciation: Increases the total depreciation for the asset on your balance sheet

For example, if your annual depreciation is $180, your journal entry would look like this:

- Depreciation Expense: Debit $180

- Accumulated Depreciation: Credit $180

This entry keeps your financial statements accurate and up to date.

How to calculate accumulated depreciation

Calculate accumulated depreciation by adding up all the depreciation expenses you've recorded since buying the asset. This shows you exactly how much value your assets have lost over time.

While the straight-line method is the simplest approach for many small businesses, tax authorities also specify other methods, such as applying a diminishing value (DV) rate for certain assets.

The straight-line depreciation calculation

The straight-line method uses this formula to calculate annual depreciation:

Annual depreciation expense = (Asset cost − Salvage value) ÷ Useful life

This gives you the same depreciation amount each year until the asset reaches its estimated residual value. Check official guidelines, as historic depreciation rates may apply to assets acquired in previous years, and rules frequently change—for example, the depreciation rate for non-residential buildings returned to 0% for the 2025 income year.

Each component affects your calculation:

- Cost of asset: The original purchase price

- Salvage value: The estimated resale or scrap value when the asset is no longer usable

- Useful life: The estimated years the asset will function before becoming unusable or obsolete

When you understand how each component affects your calculation, you can estimate depreciation accurately:

- Shorter useful life: Increases annual depreciation because the same total spreads over fewer years

- Higher salvage value: Decreases annual depreciation because there's less total value to depreciate

- Higher asset cost: Increases annual depreciation because there's more total value to depreciate

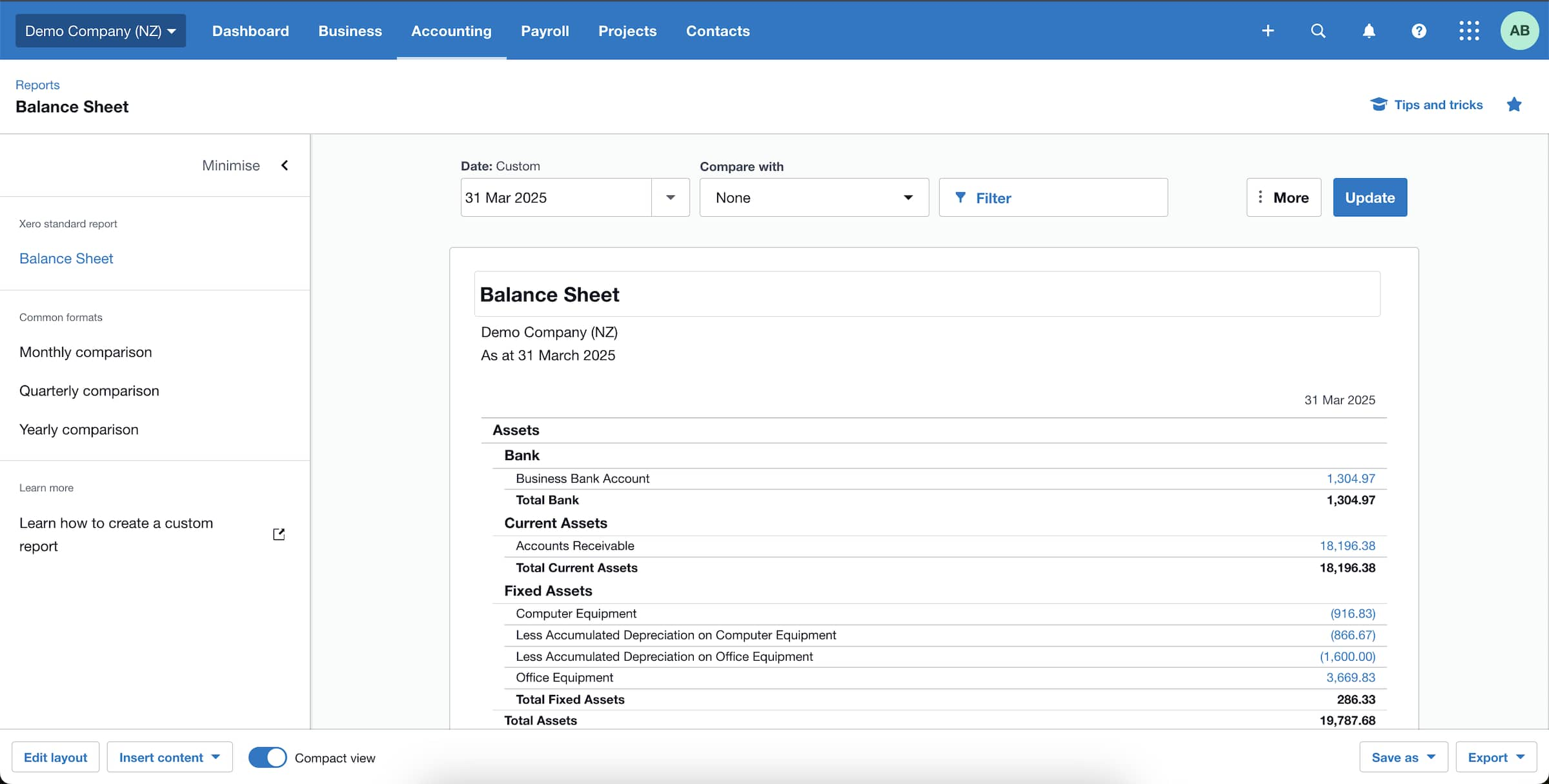

Example: balance sheet with accumulated depreciation

This example shows how accumulated depreciation changes an asset's net book value on your balance sheet.

Calculate straight-line depreciation

Let's calculate accumulated depreciation using the straight-line depreciation method. In this example, our asset cost $1,000, has a useful life of five years, and a salvage value of $100.

- Calculate the annual depreciation expense

Using our formula above, our example gives us:

($1,000 – $100) ÷ 5 = $180 per year

- Track accumulated depreciation each year

Create a depreciation schedule to track how accumulated depreciation increases each year. In our example:

- Year 1: 1 × $180 = $180

- Year 2: 2 × $180 = $360

- Year 3: 3 × $180 = $540

- Year 4: 4 × $180 = $720

- Year 5: 5 × $180 = $900

- Calculate the asset's book value at a point in time

Use the formula:

Book value = initial cost – accumulated depreciation

In our example, after three years, the asset's book value is:

$1,000 – $540 = $460

Simplify your accounting with Xero

Managing depreciation can get complicated as your business grows. Xero simplifies these tasks by making your accounting processes easier and helping you track your assets.

Create detailed depreciation schedules that give you a clear view of fixed asset values and make your financial reporting more accurate. Get one month free.

FAQs on accumulated depreciation

Here are some of the most commonly asked questions about accumulated depreciation.

How does accumulated depreciation affect cash flow?

Accumulated depreciation has no direct effect on cash flow because it's a non-cash expense. Your cash stays in your business when you record it.

However, it improves cash flow indirectly by reducing your taxable income. This means you keep more cash in your business.

What happens to an asset's accumulated depreciation when you sell it?

Accumulated depreciation is removed from the balance sheet when you sell the asset. The asset's book value at disposal (asset cost minus accumulated depreciation) is compared with the sale price to determine a net gain or loss.

Do I record accumulated depreciation as a debit or a credit?

Record accumulated depreciation as a credit on your balance sheet.

Accumulated depreciation is a contra asset that reduces your asset's value. Since assets normally have debit balances, you credit accumulated depreciation to offset and reduce the asset's book value over time.

Is accumulated depreciation a current liability?

Accumulated depreciation is a contra asset, not a current liability. It reduces the value of an asset on your balance sheet.

Current liabilities are short-term debts due within 12 months. Accumulated depreciation lowers an asset's book value over time and isn't an amount you owe or need to repay.

Here's more about current and non-current liabilities.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Get one month free

Purchase any Xero plan, and we will give you the first month free.