Working capital: formula, ratio and why it matters

Learn what working capital shows, how to calculate it, and why it matters for your cash flow.

Written by Jotika Teli—Certified Public Accountant with 24 years of experience. Read Jotika's full bio

Published Tuesday 21 April 2026

Table of contents

Key takeaways

- Calculate your working capital by subtracting your current liabilities from your current assets — a positive result means you can cover short-term bills and still have funds left to grow your business.

- Aim for a working capital ratio between 1.5 and 2.0, but check your industry benchmark, as service businesses can operate healthily at 1.2 while manufacturers may need up to 2.5.

- Speed up cash coming in by invoicing immediately after completing work, shortening payment terms, and following up on overdue invoices on the due date rather than weeks later.

- Forecast your cash flow at least three to six months ahead so you can spot shortfalls early and keep enough cash on hand to cover two to three months of expenses.

Components of the working capital formula

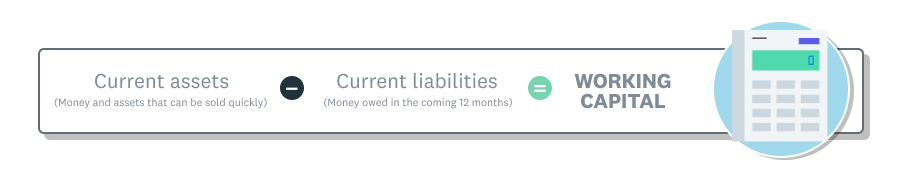

Working capital is the difference between what your business owns in the short term and what it owes in the short term. It shows whether you have enough cash and liquid assets to cover upcoming bills and expenses.

The working capital formula has two main parts: current assets and current liabilities. Understanding what goes into each helps you calculate your working capital accurately, which is essential when preparing annual audited financial statements.

Current assets

Current assets are anything your business owns that you can convert into cash within 12 months. Think of them as your short-term resources.

Common examples of current assets include the following:

- Cash: Funds in bank accounts and petty cash

- Accounts receivable: Money owed to you by customers

- Inventory: Stock, raw materials, and finished goods

- Short-term investments: Assets you can liquidate quickly

- Prepaid expenses: Rent or insurance paid in advance

Current liabilities

Current liabilities are debts or payments your business needs to make within the next 12 months. These are your short-term financial obligations.

Common examples of current liabilities include the following:

- Accounts payable: Money you owe to suppliers

- Short-term loans: Loan payments and interest due within 12 months

- Accrued expenses: Wages, taxes, and bank fees not yet paid

- Deferred revenue: Payments received for work you haven't completed

How to calculate working capital

Calculate working capital by following these steps:

- Find your current assets: Add up cash, accounts receivable, inventory, and prepaid expenses from your balance sheet or accounting software.

- Find your current liabilities: Add up accounts payable, short-term loans, accrued expenses, and deferred revenue.

- Subtract liabilities from assets: Use the formula below.

Working capital formula:

Working capital = Current assets − Current liabilities

Example: If your business has $50,000 in current assets and $30,000 in current liabilities, your working capital is $20,000. This means you have $20,000 available to cover short-term needs and invest in growth.

What is a good working capital ratio?

The working capital ratio (also called the current ratio) shows whether your business has enough short-term assets to cover short-term debts. It's a quick way to check if your working capital position is healthy.

How to calculate working capital ratio

Divide your current assets by your current liabilities to find your ratio.

Working capital ratio = Current assets ÷ Current liabilities

For example, if you have $50,000 in current assets and $30,000 in current liabilities, your ratio is 1.67. This means you have $1.67 in assets for every $1 you owe.

Industry benchmarks for working capital

What counts as a good ratio depends on your industry. Here are some common benchmarks:

- Service businesses: 1.2 to 1.5 is typically healthy as there are lower inventory needs

- Retail businesses: 1.5 to 2.0 works well to account for stock turnover

- Manufacturing businesses: 1.8 to 2.5 is common due to higher inventory and receivables

- Construction businesses: 1.5 to 2.0 helps manage project-based cash flow

A ratio below 1.0 means you may struggle to pay bills. A ratio above 2.5 could mean you're holding too much cash that could be working harder for your business.

The importance of working capital in business

Working capital matters because it reveals whether your business can survive and grow. A healthy working capital position means you can handle the unexpected without scrambling for cash.

Strong working capital helps you in the following ways:

- Pay bills during slow periods: Cover expenses when revenue dips.

- Handle unexpected costs: Manage emergencies without borrowing.

- Invest in opportunities: Fund growth when the timing is right.

- Access funding: Lenders and investors check working capital before approving loans to ensure you operate a viable business that will be able to pay its debts when invoiced in the coming months.

Positive vs negative working capital

Your working capital number tells you where your business stands financially. Different positions indicate different financial situations:

- Positive working capital: Current assets exceed current liabilities. You can pay your bills and debts, with surplus to reinvest in the business.

- Negative working capital: Current liabilities exceed current assets. You may struggle to meet debts without borrowing or raising funds. If this continues, the business could be in financial trouble.

- Neutral working capital: Current assets and liabilities are roughly equal. This works if sales are steady, but leaves little buffer for unexpected expenses or reinvestment.

- Very high working capital: You may be holding more cash than needed instead of investing in growth or innovation.

How to improve your working capital

If your working capital is lower than you'd like, there are practical steps you can take. Focus on getting cash in faster and slowing cash going out.

Speed up your invoicing and collections

The faster you get paid, the more cash you have available. Here are some tips to speed up payments:

- Invoice immediately: Send invoices as soon as work is complete, not at month end.

- Shorten payment terms: Move from 30-day to 14-day terms where possible.

- Offer early payment incentives: A small discount for fast payment can be worth it.

- Chase overdue invoices: Follow up on the due date, not weeks later.

Negotiate better payment terms with suppliers

Extending how long you have to pay improves your cash position. Here are some approaches to consider:

- Ask for longer terms: Request 45 or 60 days instead of 30.

- Build relationships: Reliable customers often get better terms.

- Time your payments: Pay on the due date, not before.

Optimise your inventory levels

Cash tied up in stock is cash you can't use elsewhere. Here are some steps to manage your inventory:

- Review slow-moving items: Discount or clear stock that isn't selling.

- Order more frequently: Smaller, regular orders reduce cash tied up in inventory.

- Track what sells: Focus stock investment on your best performers.

Control your expenses

Reducing outgoings directly improves working capital. Here are some tips to keep expenses in check:

- Review subscriptions: Cancel software or services you don't use.

- Renegotiate contracts: Suppliers may offer better rates to keep your business.

- Delay non-essential spending: Postpone purchases that aren't urgent.

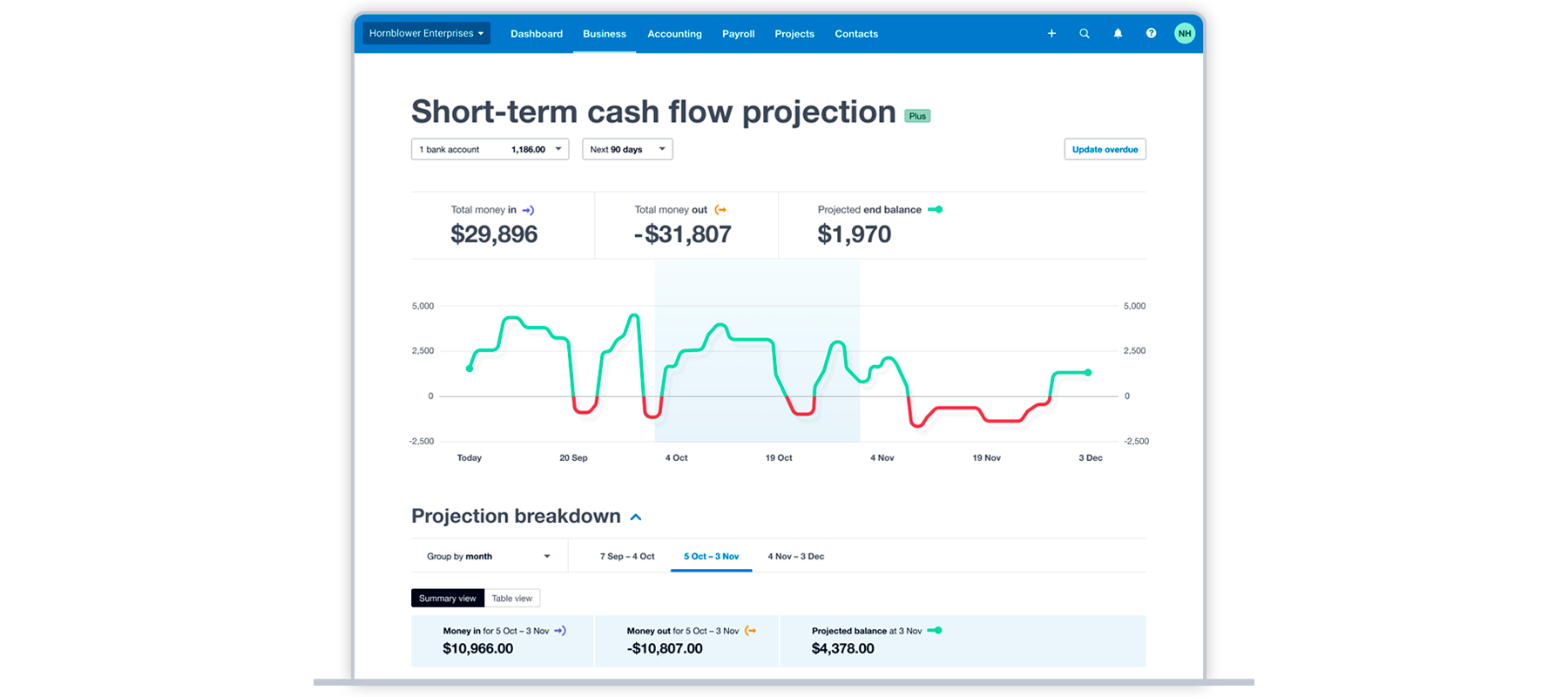

Forecast your cash flow

Planning ahead helps you avoid working capital crunches. Here are some actions to stay prepared:

- Project income and expenses: Map out the next three to six months.

- Identify gaps early: Spot potential shortfalls before they become problems.

- Build a buffer: Aim to keep enough cash to cover two to three months of expenses.

How Xero helps you manage working capital

Keeping track of working capital manually takes time you could spend on your business. Accounting software automates the heavy lifting and gives you real-time visibility into your financial position.

Xero helps you manage working capital in the following ways:

- Track cash flow in real time: See exactly where your money is going and when payments are due.

- Automate invoicing: Send invoices faster and set up payment reminders to get paid sooner.

- Monitor accounts receivable: Identify overdue invoices and follow up before cash flow becomes an issue.

- Generate financial reports: View your current assets and liabilities instantly to calculate working capital on demand.

- Forecast cash flow: Use cash flow projections to plan ahead and avoid shortfalls.

FAQs on working capital

Here are answers to some frequently asked questions about working capital.

What is working capital?

Working capital is the difference between your current assets (what you own) and your current liabilities (what you owe) within a 12-month period. It measures your ability to pay short-term debts and expenses.

Why is working capital important?

Working capital shows whether your business has enough cash and liquid assets to cover day-to-day expenses and unexpected costs. Positive working capital means you can operate without constantly borrowing or struggling to pay bills.

What is a good working capital ratio?

A ratio between 1.5 and 2.0 is generally considered healthy for most businesses. However, the ideal ratio varies by industry. Service businesses may operate well with lower ratios (1.2 to 1.5), while manufacturing businesses often need higher ratios (1.8 to 2.5).

Can you have too much working capital?

Yes. While positive working capital is good, having too much (a ratio above 2.5) may mean you're holding excess cash that could be invested in growth, equipment, or other opportunities to improve your business.

How often should I calculate working capital?

Calculate your working capital monthly or quarterly to monitor your business's financial health. More frequent calculations help you spot trends early and make adjustments before cash flow problems arise.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Get one month free

Purchase any Xero plan, and we will give you the first month free.