What is accumulated depreciation? Formula and examples

Learn what accumulated depreciation is, how to calculate it, and how it affects your small business.

Written by Jotika Teli—Certified Public Accountant with 24 years of experience. Read Jotika's full bio

Published Monday 20 April 2026

Table of contents

Key takeaways

- Recognize that accumulated depreciation is a contra asset account, not a liability — it sits on your balance sheet alongside your assets and reduces their value from the original purchase price to show a realistic book value.

- Use the straight-line depreciation formula — (cost of asset minus salvage value) divided by useful life — to calculate your annual depreciation expense and build a schedule that tracks how your asset's book value changes each year.

- Apply depreciation expenses to lower your taxable income, which reduces your tax bill and keeps more cash in your business, while remembering that depreciation is a non-cash expense that gets added back on your cash flow statement.

- Choose a depreciation method that matches how your asset loses value — use straight-line for assets that wear evenly over time, and declining balance or double-declining balance for technology or equipment that loses value faster in its early years.

What is accumulated depreciation?

Accumulated depreciation is the total amount an asset has decreased in value since you bought it. It shows the cumulative wear, tear, and ageing of your business assets over time.

This tracking helps you understand the carrying amount of your assets on your financial statements, which is the amount recognised after deducting any accumulated depreciation and impairment losses.

The calculation is simple:

Book value = asset cost – accumulated depreciation

Here are some examples:

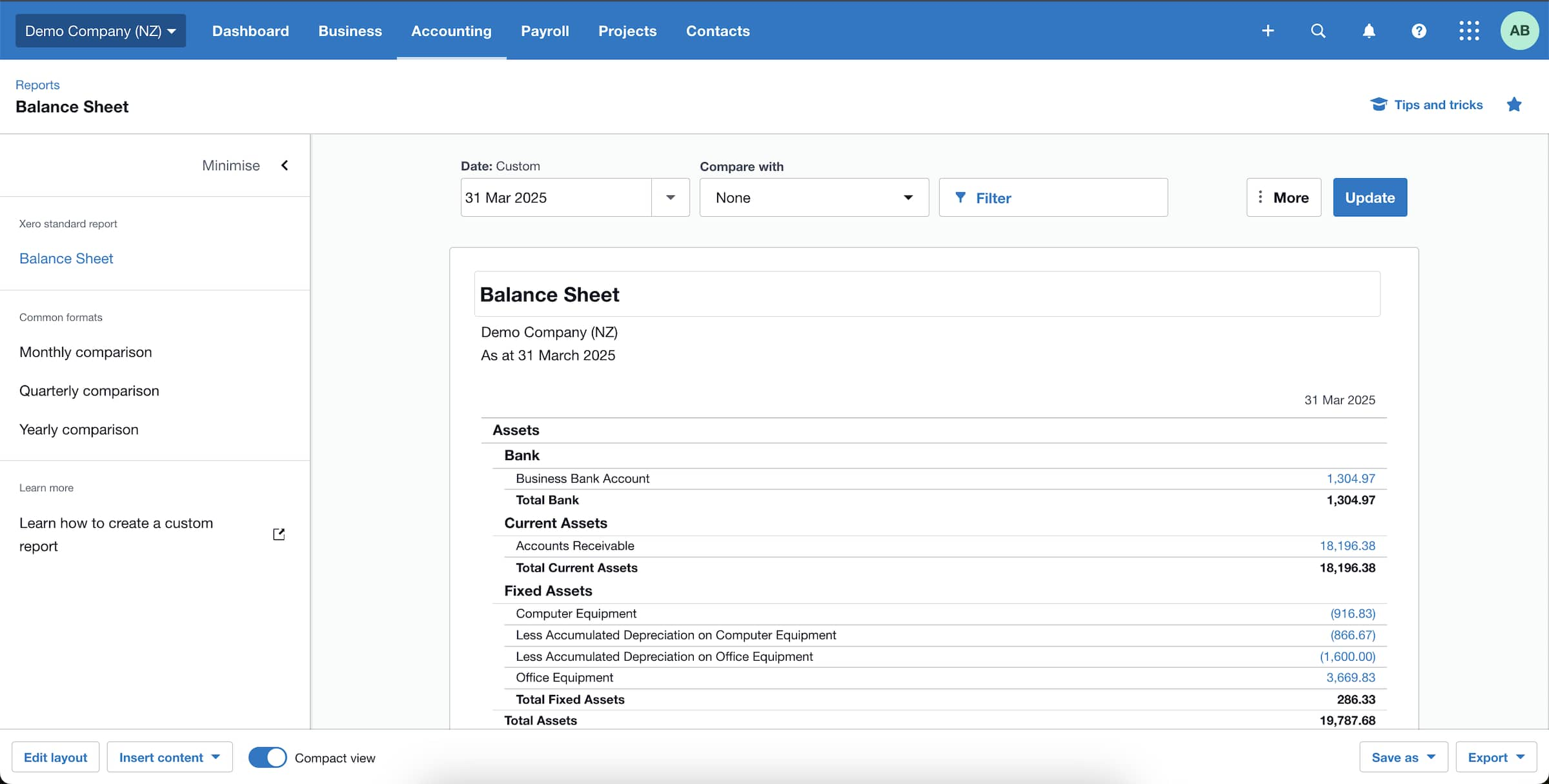

- Office furniture: Costs $5,000 and depreciates by $1,000 each year. After three years, accumulated depreciation totals $3,000, leaving a book value of $2,000.

- Machinery: Costs $25,000 and depreciates by $2,500 each year. After six years, accumulated depreciation totals $15,000, leaving a book value of $10,000.

Depreciation vs accumulated depreciation

Understanding the difference between these two terms is essential for accurate financial reporting.

Depreciation and accumulated depreciation are related but distinct concepts.

Depreciation is the annual expense showing how much an asset loses value each year. Accumulated depreciation is the running total of all depreciation expenses for that asset since you bought it.

The key difference:

- Depreciation: Records the annual expense on your income statement

- Accumulated depreciation: Tracks the cumulative total on your balance sheet

Is accumulated depreciation an asset or a liability?

Many business owners wonder how to classify accumulated depreciation on their balance sheet.

Accumulated depreciation is neither an asset nor a liability – it's classified as a contra asset account.

Here's why it's not a liability:

- Liabilities represent money you owe or obligations to fulfil

- Accumulated depreciation doesn't create a debt to repay

- It simply tracks how much value your asset has lost over time

Contra asset accounts work differently from regular assets. They have three key characteristics:

- Reduce asset totals with negative values

- Show realistic asset values rather than original purchase prices

- Appear alongside assets on the balance sheet but subtract from their value

While you record the contra asset alongside your other assets, it always has a credit balance, showing how accumulated depreciation reduces an asset's value from its original cost. This gives you the asset's carrying amount or book value.

Why understanding accumulated depreciation matters for a business

Tracking accumulated depreciation provides valuable insights for business planning and financial management.

Understanding accumulated depreciation helps you:

- Plan ahead: Track asset values over time to schedule replacements, upgrades and maintenance

- Reduce taxes: Lower your taxable income with depreciation expenses, as eligible businesses may be able to claim an immediate or accelerated deduction, which can reduce your tax bill and keep more cash in your business

- Access finance: Show lenders and investors the value of your assets to improve your chances of getting approved

How does accumulated depreciation affect financial statements?

Accumulated depreciation appears on three key financial statements, each serving a different purpose.

Accumulated depreciation on the balance sheet

Accumulated depreciation reduces an asset's book value on the balance sheet. Although your balance sheet lists the asset's original cost, accumulated depreciation adjusts this value downwards to arrive at the asset's carrying amount under the cost model.

Accumulated depreciation on the income statement

You record depreciation as an expense on your income statement, which reduces your taxable income. For tax purposes, deductions depend on tax rules and may differ from accounting depreciation. As a non-cash expense, depreciation does not directly use cash, although it can affect cash flow indirectly through tax.

Accumulated depreciation on the cash flow statement

You add depreciation back to net income on the cash flow statement because it doesn't involve actual cash leaving your business. This adjustment reflects that depreciation is an accounting expense, not a cash outflow.

Learn more about how the ATO treats depreciation

How to calculate accumulated depreciation

Several methods exist for calculating accumulated depreciation. Here's the most common approach for small businesses.

Straight line depreciation spreads an asset's depreciable amount evenly across its useful life. It's the simplest method for small businesses to calculate accumulated depreciation.

The straight line depreciation calculation

Formula: Annual depreciation expense = (cost of asset − salvage value) / useful life

Key terms explained:

- Cost of asset: The purchase price and directly attributable costs necessary to bring the asset into use

- Salvage value: The estimated resale or scrap value when the asset is no longer useful

- Useful life: The expected years the asset will function before becoming obsolete

To maintain accuracy, Australian Accounting Standards require you to review an asset's useful life and residual value at least annually, specifically at each financial year-end.

For example, an asset with a short useful life spreads depreciation over fewer years, resulting in a higher annual depreciation expense.

If an asset holds its value well and has a relatively high salvage value, it will depreciate less each year, leading to a lower annual depreciation expense.

Calculate straight line depreciation

Here's how to calculate accumulated depreciation using the straight line method. In this example, an asset costs $1,000, has a useful life of five years, and a salvage value of $100.

Other depreciation methods

While the straight-line method is popular for its simplicity, other methods might suit your business better. This is especially true for assets that lose value faster in their early years.

Accounting standards require you to use a depreciation method that reflects how you consume the asset's future economic benefits.

Declining balance method

This method applies a constant depreciation rate to the asset's book value each year. It results in higher depreciation expenses in the early years and lower expenses later on.

Use this method for assets that are more productive when they're new.

Double-declining balance method

This approach doubles the straight-line depreciation rate, making it a more accelerated version of the declining balance method. It significantly speeds up depreciation in the first few years.

Use this method for technology or equipment that quickly becomes outdated.

Simplify your accounting with Xero

Managing depreciation, adjusting entries, and calculating accumulated depreciation quickly gets complicated, especially as your business grows.

You can simplify these tasks with Xero, which streamlines your accounting processes and helps you manage and track your assets. You can create detailed depreciation schedules that give you a clear view of fixed asset values and make your financial reporting more accurate.

Learn how Xero supports your business or get one month free to see how easily you can track assets.

FAQs on accumulated depreciation

Find answers to common questions about accumulated depreciation below.

How does accumulated depreciation affect cash flow?

Accumulated depreciation doesn't directly affect cash flow because it's a non-cash expense. No money actually leaves your business.

However, it improves your cash position indirectly. Here's how the tax benefits work:

- depreciation expenses reduce your taxable income

- lower taxable income results in lower tax bills

- lower taxes keep more cash in your business

What happens to an asset's accumulated depreciation when you sell it?

When you sell an asset, you remove its accumulated depreciation from the balance sheet. This aligns with accounting standards stating that depreciation of an asset ceases when you classify it as held for sale or derecognise it. Depreciation stops at the earlier of the date you classify the asset as held for sale or the date you derecognise it from the books.

You compare the asset's book value at disposal (asset cost minus accumulated depreciation) with the sale price to determine a gain or loss.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Start using Xero for free

Access Xero features for 30 days, then decide which plan best suits your business.