Margin of safety formula: how to calculate your buffer

Learn the margin of safety formula and how to calculate yours for smarter business decisions.

Written by Shaun Quarton—Accounting & Finance Content Writer and Growth Marketer. Read Shaun's full bio

Written by Shaun Quarton—Accounting & Finance Content Writer and Growth Marketer. Read Shaun's full bio

Published Wednesday 22 April 2026

Table of contents

Key takeaways

- Calculate your margin of safety by subtracting your break-even sales from your current sales, then dividing by your current sales — a result of 20% or higher is generally a healthy buffer, though this varies by industry.

- Monitor your margin of safety monthly or quarterly so you can spot changes in sales or costs early and act before your business dips into a loss.

- Use your margin of safety to guide key decisions such as setting sales targets, adjusting pricing, controlling costs, and assessing whether a new product launch is financially viable.

- Combine your margin of safety with other financial metrics like cost-volume-profit analysis and profitability ratios to get a fuller picture of your business risk, rather than relying on one measure alone.

Key takeaways

- Calculate your margin of safety using the formula (Current sales - Break-even sales) ÷ Current sales to determine what percentage your sales can drop before reaching break-even, with 20% or higher generally considered a healthy buffer.

- Monitor your margin of safety monthly or quarterly to stay on top of your financial health and react quickly to changes in sales or costs that could affect your business risk.

- Use your margin of safety to guide critical business decisions including setting realistic sales targets, adjusting pricing strategies, controlling costs, and evaluating new product launches based on their impact on your financial buffer.

- Combine margin of safety calculations with cost-volume-profit analysis and other financial metrics to get a complete view of your business risk and profit potential rather than relying on this single measure alone.

What is the margin of safety?

Margin of safety is the percentage your sales can drop before your business reaches break-even. It measures your financial buffer against revenue declines or cost increases. The wider your margin of safety, the lower your business risk, though required buffers vary by industry. For instance, a cafe may only need 10 to 15 per cent of working capital per dollar of sales, while a manufacturer may require 20 to 25 per cent.

Why margin of safety matters for your small business

Margin of safety protects your business from financial risk by showing how much sales can drop before you make a loss. External shocks like supplier price increases push up your break-even point. This risk grows if you rely on one supplier that provides 30 per cent or more of your total product requirements.

Knowing your margin of safety gives you a clear advantage when making business decisions:

- Protects against forecasting errors: Sales forecasts are never perfect. Your margin of safety gives you a cushion if your projections are too optimistic.

- Reduces financial risk: It shows you exactly how much sales can dip before you start losing money, helping you avoid cash flow problems.

- Supports confident decisions: When you know your financial buffer, you can make choices about pricing, costs, and growth with less stress.

- Improves long-term stability: Consistently monitoring your margin of safety helps you build a more resilient business that can weather economic ups and downs.

What is the margin of safety formula?

The margin of safety formula calculates the percentage buffer between your current sales and break-even point:

(Current sales – Break-even sales) ÷ Current sales = Margin of safety

The formula requires two key figures:

- Current sales: your total revenue over a specific period

- Break-even sales: the minimum revenue needed to cover all costs

Here's a quick margin of safety example. A business has current sales of $50,000 and needs $30,000 in sales to break even.

Margin of safety = ($50,000 – $30,000) ÷ $50,000 = 0.4 (40%)

This means sales could drop by 40% before hitting the break-even point. Any further drop would result in a loss.

How to calculate margin of safety

Use these three steps to work out your margin of safety and see your business's financial buffer.

1. Find your current sales

Start by determining your current sales using either actual figures or forecasts. Current sales figures are available through your existing sales tools.

If you need to forecast, four common methods include:

- Historical data: Analyse your financial reports for past sales trends and seasonal patterns. You might find these in your point of sale (POS) system (which can reveal granular details, such as 86 per cent of overall sales occurring after 11.00am), ecommerce platform, or accounting software like Xero.

- Market research: Study your target market, industry trends, and competitor performance.

- Qualitative forecasting: Ask your sales team or industry experts for their insights.

- Quantitative forecasting: Use statistical methods to analyse your historical and market data to predict future sales more accurately.

The best approach depends on your business type and the data available to you.

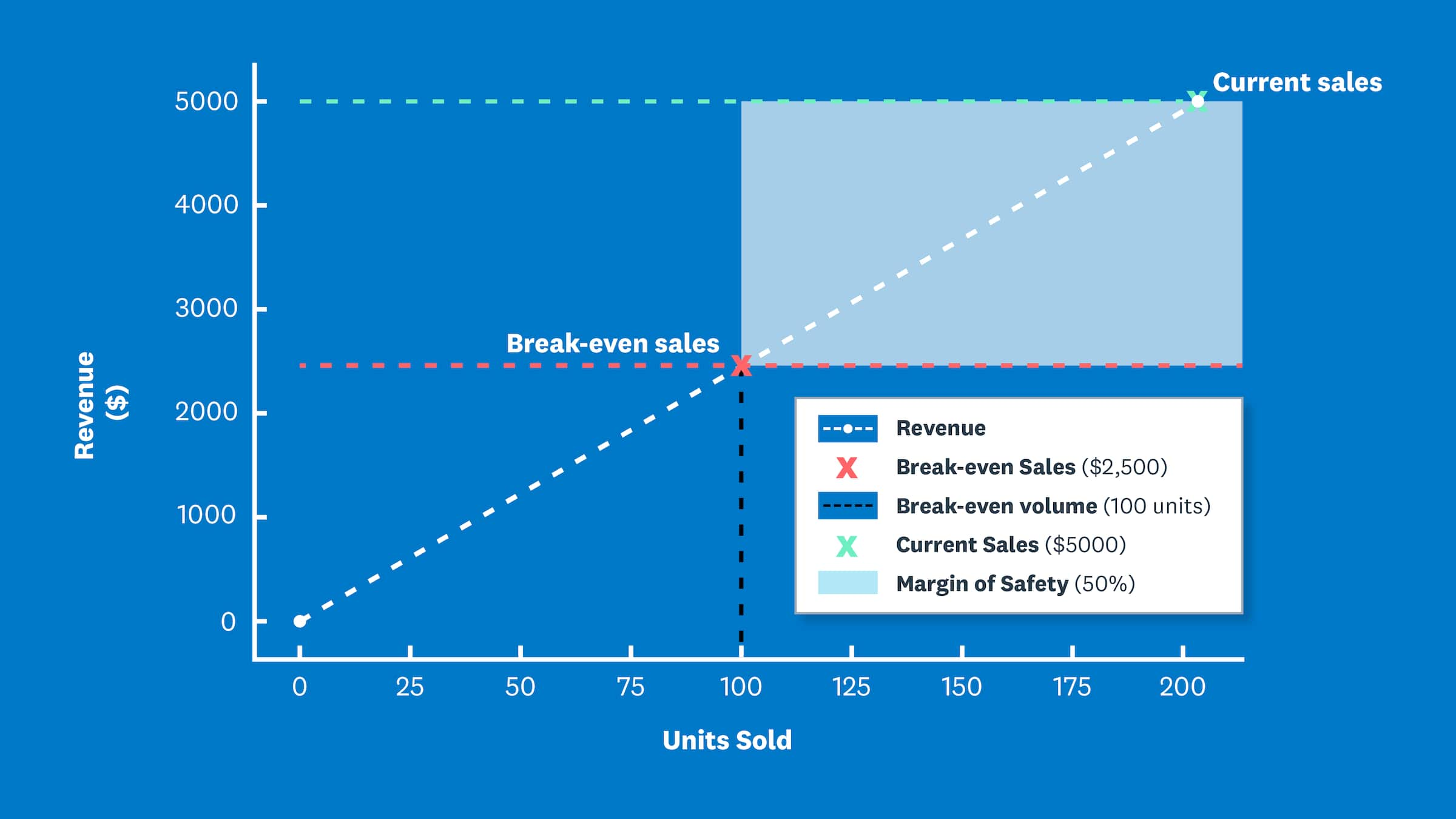

For example, a craft business uses a point of sale (POS) system to track monthly sales. Last month, sales were $5,000. This figure is used in the following steps.

2. Calculate your break-even sales revenue point

Calculate your break-even sales revenue using this formula:

Fixed costs ÷ ((Sales price – Variable cost) ÷ Sales price) = Break-even sales

In the formula:

- Fixed costs: Expenses that stay the same regardless of sales volume, such as salaries and rent. For some businesses, salary expenses can significantly exceed the industry benchmark of 20 to 25 per cent, making them a critical fixed cost to manage.

- Variable costs: Expenses that change with sales volume, such as raw materials and sales commission.

Here's more info on variable costs and how they differ from fixed costs. Your accountant can also help you distinguish between them.

To demonstrate, a craft business has:

- fixed costs of $2,000

- variable costs of $5 per unit

- a sales price of $25 per unit

Therefore:

2,000 ÷ ((25 – 5) ÷ 25) = 2,000 ÷ (20 ÷ 25) = 2,000 ÷ 0.8 = $2,500

With a sales price of $25, you need revenue of $2,500 (100 sales units) to break even.

3. Apply the margin of safety formula

Apply the margin of safety formula:

(Current sales – Break-even sales) ÷ Current sales = Margin of safety

The result is your margin of safety ratio: the percentage by which sales can fall before your business starts operating at a loss.

Let's apply the formula to the craft business example, where current sales are $5,000 and the break-even point for sales revenue is $2,500:

($5,000 – $2,500) ÷ $5,000 = 2,500 ÷ 5,000 = 0.5 = 50%

The craft business has a 50% margin of safety, meaning sales could fall by half before they reach the break-even point.

How the margin of safety supports your business decisions

Margin of safety guides key business decisions across four areas:

- Performance targets: Set achievable sales goals based on your break-even point.

- Pricing strategy: Adjust prices when your margin shrinks to ensure adequate cost coverage.

- Cost control: Reduce expenses when low margins signal financial risk.

- Product launches: Evaluate how new offerings affect your safety buffer before launch.

Other metrics work with the margin of safety in your accounting analysis

Margin of safety works best when combined with other financial metrics, keeping in mind that organisations can heavily prioritise financial tracking, with one reviewed company using 88 metrics to measure financial risks compared to just 14 for non-financial risks. Pairing it with profitability ratios, cash flow analysis, and break-even tracking gives you a more complete view of your business health.

Margin of safety and cost-volume-profit (CVP) analysis

Cost-volume-profit (CVP) analysis models how changes in costs, sales volume, and pricing affect profitability. It's a forward-looking tool that complements margin of safety calculations, especially since alternative models like Activity-Based Costing (ABC) have been attempted by 60% of US organisations but sustained by only 20%.

Research shows 80% of organisations still use traditional costing methods, though more modern approaches can improve business management.

Here's how the two tools differ:

- Margin of safety: Shows your current financial buffer.

- CVP analysis: Projects how business changes will affect future profitability.

Together, these tools provide a complete view of business risk and profit potential. Learn more about decision-making.

Simplify your margin of safety calculations

Automated margin of safety calculations save time and improve accuracy. Traditional methods require:

- tracking down financial figures across multiple sources

- updating spreadsheets manually

- piecing together reports from different systems

You can automate margin of safety calculations with up-to-date financial data in one place using Xero. You can make decisions faster with clear reports and current numbers. Get one month free to start tracking your margin of safety with real-time data.

FAQs on margin of safety

Here are answers to some common questions about margin of safety.

What is a good margin of safety percentage?

A margin of safety of 20% or higher is generally considered healthy, though this varies by industry. This buffer helps absorb unexpected costs like shrinkage of stock, which can represent a significant percentage of the cost of goods sold.

How often should I calculate my margin of safety?

Many businesses review margin of safety regularly, often monthly, quarterly, or whenever pricing, cost structure, or sales conditions change.

What does it mean if my margin of safety is negative?

A negative margin of safety means your business is operating below its break-even point and is currently making a loss. Use this as a prompt to review your pricing, sales volume, and costs quickly. A prolonged negative margin, like one company that remained outside its risk appetite for 30 consecutive months, signals urgent action is needed.

How does margin of safety compare to other financial ratios?

Margin of safety focuses on break-even risk, while profitability ratios measure how efficiently you turn revenue into profit. Using them together gives you a more complete picture of your business's financial health.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Get one month free

Purchase any Xero plan, and we will give you the first month free.