Break-even point formula: how to calculate it for your business

Calculate the sales you need to cover all costs and start making a profit.

November 2023 | Published by Xero

Published Thursday 23 July 2026

Table of contents

Key takeaways

- Your break-even point is the sales level where total revenue equals total costs, meaning you're not making a profit or a loss.

- The break-even point formula uses your fixed costs and contribution margin to show exactly how much you need to sell to cover all expenses.

- Recalculating your break-even point regularly helps you make informed decisions about pricing, product launches and business growth.

- Understanding both the revenue and volume break-even formulas gives you flexibility to plan whether you sell products, services or a mix of both.

What is break-even point?

The break-even point is the level of sales at which your total revenue exactly equals your total costs. At this point, your business isn't making a profit or a loss.

Knowing your break-even point gives you a clear target. Once you pass it, every additional sale contributes directly to profit. Below it, you're operating at a loss.

For small business owners, this number is one of the most practical financial benchmarks you can calculate. It tells you the minimum your business needs to earn before it starts paying for itself.

How to calculate revenue break even point

Why break-even point matters for your business

Your break-even point isn't just a textbook formula. It's a practical tool that shapes some of the biggest decisions you'll make as a business owner.

Here are some of the ways break-even analysis helps your business:

- Pricing strategy: it shows you the minimum price you need to charge to cover costs, so you can set prices with confidence.

- Attracting investors: showing a clear path to profitability makes your business case stronger when speaking with lenders or investors.

- Marketing decisions: knowing how many sales you need to break even helps you work out whether a marketing campaign is worth the spend.

- Business planning: it gives you a concrete sales target to build your forecasts around, rather than guessing.

How to calculate volume break even point

Market conditions also play a role. Xero Small Business Insights data from the December quarter of 2025 shows that sales growth varied widely across industries, from +9.5% in construction to +3.5% in hospitality. These differences highlight why it's worth revisiting your break-even point regularly, especially when market conditions in your industry shift.

When to use break-even analysis

Break-even analysis is useful at several key moments in your business journey. Here are some common scenarios where it can guide your decisions.

- Starting a new business: before you launch, a break-even calculation shows how much revenue you need to cover your setup and ongoing costs.

- Launching a new product or service: adding to your offering changes your cost structure. Running the numbers first helps you assess whether the new line will be profitable.

- Changing your pricing: if you're considering a price increase or discount, break-even analysis shows you how the change affects the sales volume you need.

- Restructuring your business model: switching from retail to online, taking on a lease, or hiring staff all shift your fixed and variable costs. Recalculating your break-even point helps you plan for those changes.

Understanding your costs: fixed and variable

Before you can calculate your break-even point, you need to separate your business costs into 2 categories: fixed costs and variable costs.

Fixed costs stay the same regardless of how much you sell. These are expenses you pay whether you make 1 sale or 1,000. Common examples include:

- Rent or lease payments

- Insurance premiums

- Salaries for permanent staff

- Software subscriptions

- Loan repayments

Variable costs change in proportion to your sales volume. The more you sell, the higher these costs go. Examples include:

- Raw materials or stock purchases

- Packaging and shipping

- Sales commissions

- Casual or contract labour

- Payment processing fees

Some costs sit between the 2 categories. Electricity, for example, has a fixed base charge plus usage that rises with production. For break-even purposes, allocate these as best you can based on your business activity.

According to Xero Small Business Insights, wages for Australian small businesses grew 2.0% year-on-year in the December quarter of 2025, a reminder that variable costs like labour shift over time, making regular break-even recalculations essential.

What is contribution margin?

Contribution margin is the amount each sale contributes toward covering your fixed costs. Once your total contribution margin exceeds your fixed costs, you've reached your break-even point.

The formula is straightforward:

Contribution margin = Selling price per unit − Variable cost per unit

For example, if you sell a product for $50 and the variable cost to produce it is $20, your contribution margin is $30 per unit. That $30 goes toward paying off your fixed costs.

You can also express contribution margin as a ratio by dividing it by the selling price. In this case, $30 ÷ $50 = 0.6, or 60%. This ratio is useful when calculating your revenue break-even point.

Break-even point formula

The break-even point formula tells you exactly how much you need to sell before your business covers all its costs. There are 2 main approaches, depending on whether you want the answer in dollars or units.

Revenue break-even point = Fixed costs ÷ Contribution margin ratio

This gives you the total dollar amount of sales you need.

Volume break-even point = Fixed costs ÷ Contribution margin per unit

This gives you the number of units you need to sell.

Both formulas rely on the contribution margin, which is why understanding that concept first makes the calculation much simpler. The following sections walk you through each approach with step-by-step detail.

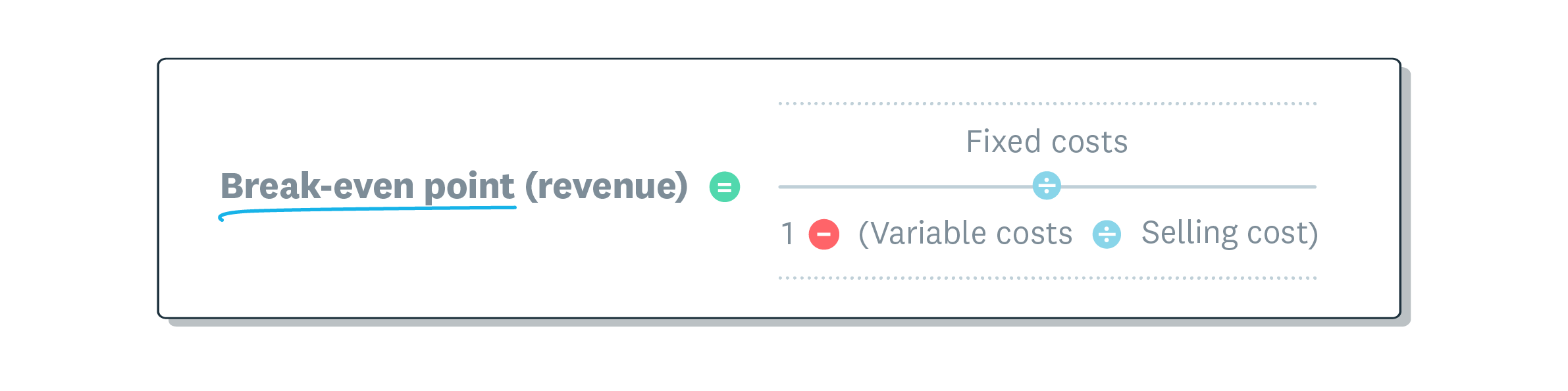

Revenue break-even point formula

The revenue break-even formula tells you the total sales dollars your business needs to cover all costs. It's especially useful for service-based businesses or when you sell at different price points.

Revenue break-even point = Fixed costs ÷ Contribution margin ratio

The contribution margin ratio is your contribution margin per unit divided by the selling price per unit. This gives you the percentage of each dollar of revenue that goes toward covering fixed costs.

How to calculate revenue break-even point

Follow these steps to find your revenue break-even point.

- Add up all your fixed costs for the period (for example, monthly or yearly).

- Calculate your contribution margin per unit: selling price minus variable cost per unit.

- Divide the contribution margin per unit by the selling price to get the contribution margin ratio.

- Divide your total fixed costs by the contribution margin ratio.

The result is the amount of revenue you need to generate before your business breaks even.

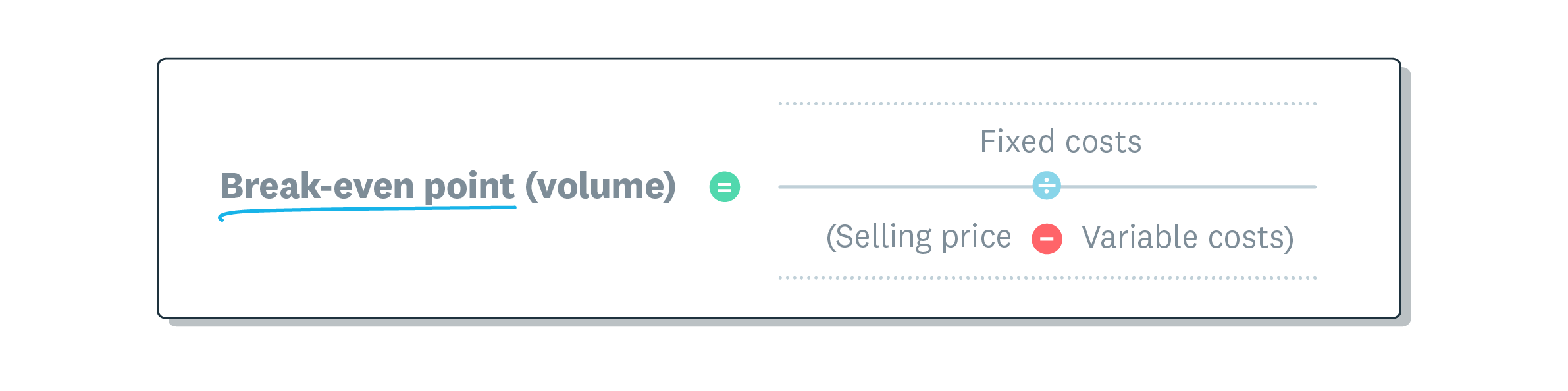

Volume break-even point formula

The volume break-even formula shows you the number of units you need to sell to cover all your costs. It's a good fit for product-based businesses with a consistent unit price.

Volume break-even point = Fixed costs ÷ Contribution margin per unit

You'll recall that contribution margin per unit is the selling price minus variable cost per unit. Dividing your fixed costs by this figure tells you the exact number of units needed to break even.

Break-even for multiple products or services

Most businesses sell more than 1 product or service. When you have a mixed offering, a single contribution margin won't reflect your full picture. Instead, you'll use a weighted-average contribution margin.

Here's how it works:

- Calculate the contribution margin for each product or service.

- Determine the sales mix: what percentage of total sales each product represents.

- Multiply each product's contribution margin by its sales mix percentage.

- Add the results together to get the weighted-average contribution margin.

- Divide your total fixed costs by the weighted-average contribution margin to find the combined break-even point.

For example, say you sell 2 products. Product A has a contribution margin of $40 and makes up 70% of sales. Product B has a contribution margin of $20 and makes up 30%.

Your weighted-average contribution margin would be ($40 x 0.7) + ($20 x 0.3) = $28 + $6 = $34. If your fixed costs are $17,000 per month, your break-even point is $17,000 ÷ $34 = 500 units.

Examples of calculating the break-even point

Seeing the formulas in action helps bring them to life. Here are 2 examples: 1 product-based and 1 service-based.

Product-based example: kombucha brewery

Imagine you run a small kombucha brewery in Melbourne. Here are your numbers:

- Selling price per bottle: $5.00

- Variable cost per bottle (ingredients, label, packaging): $1.50

- Fixed costs per month (rent, equipment lease, insurance): $5,000

First, calculate the contribution margin per bottle: $5.00 − $1.50 = $3.50.

Then divide your fixed costs by the contribution margin: $5,000 ÷ $3.50 = 1,429 bottles (rounded up).

You need to sell at least 1,429 bottles per month to break even. Any sales above that number contribute directly to profit.

To find the revenue break-even point, calculate the contribution margin ratio first: $3.50 ÷ $5.00 = 0.70 (70%). Then divide fixed costs by that ratio: $5,000 ÷ 0.70 = $7,143 in revenue per month.

Service-based example: graphic designer

Now picture a freelance graphic designer in Sydney. Their numbers look like this:

- Average project fee: $2,000

- Variable costs per project (stock images, printing, subcontractors): $400

- Fixed costs per month (studio rent, software, insurance): $4,000

Contribution margin per project: $2,000 − $400 = $1,600.

Volume break-even point: $4,000 ÷ $1,600 = 2.5 projects. Since you can't do half a project, you'd need to complete 3 projects per month to break even.

For the revenue break-even: contribution margin ratio = $1,600 ÷ $2,000 = 0.80 (80%). Revenue break-even = $4,000 ÷ 0.80 = $5,000 in revenue per month.

Margin of safety

Once you know your break-even point, the margin of safety tells you how much breathing room your business has. It measures the gap between your actual (or expected) sales and your break-even sales.

Margin of safety = Actual sales − Break-even sales

You can express this in dollars, units or as a percentage. A higher margin of safety means your business can absorb a dip in sales without falling into a loss.

For example, if your break-even revenue is $7,143 and you're currently selling $10,000 per month, your margin of safety is $2,857. That's a 28.6% buffer before you'd start losing money.

Limitations of break-even analysis

Break-even analysis is a valuable planning tool, but it does rely on some simplifying assumptions. Keeping these limitations in mind helps you use the results more effectively.

- It assumes your selling price stays constant, but in practice, you might offer discounts, run promotions or adjust prices over time.

- It treats the relationship between costs and production as linear. In reality, bulk purchasing discounts or overtime rates can change your variable cost per unit.

- It doesn't account for market changes, competitor activity or shifts in customer demand.

- It works best as a snapshot. Your break-even point can shift as costs, prices or your product mix change.

These limitations don't reduce the usefulness of break-even analysis. They simply mean it's best used alongside other financial tools and regular reviews of your actual numbers.

Take control of your business finances with Xero

Understanding your break-even point is a strong first step towards making confident financial decisions. With the right tools, you can track your costs, revenue and profitability in real time, so you always know where your business stands. Xero accounting software gives you the reporting and insights to stay on top of your numbers and plan for what's next. Get one month free.

FAQs on break-even point

Here are some frequently asked questions about break-even point.

How often should I recalculate my break-even point?

It's a good idea to recalculate whenever your costs, prices or product mix change. At a minimum, review it quarterly or when you're planning a significant business decision.

Can my break-even point change?

Yes. Any shift in your fixed costs, variable costs or selling price will move your break-even point. For example, a rent increase raises your fixed costs and pushes the break-even point higher.

What should I do once I reach my break-even point?

Reaching break-even means you've covered all your costs. From here, focus on growing your margin of safety by increasing sales, reducing costs or both, so your business builds a sustainable profit buffer.

What's the difference between break-even point and profit?

The break-even point is where revenue equals total costs, resulting in zero profit or loss. Profit only begins once your sales exceed the break-even threshold.

Handy resources

Advisor directory

You can search for experts in our advisor directory

How to increase revenue

Find out how businesses grow their sales income.

Stay on top of your numbers with Xero

Accounting software tracks your performance while you sleep.

Disclaimer

This glossary is for small business owners. The definitions are written with their requirements in mind. More detailed definitions can be found in accounting textbooks or from an accounting professional. Xero does not provide accounting, tax, business or legal advice.