Solvency vs liquidity: key differences and ratios explained

See how solvency and liquidity affect your business, and learn how to measure both with confidence.

Written by Jotika Teli—Certified Public Accountant with 24 years of experience. Read Jotika's full bio

Published Monday 20 April 2026

Table of contents

Key takeaways

- Monitor both solvency and liquidity ratios regularly to get a full picture of your financial health: aim for a solvency ratio of 20% or above and a current ratio of 1.5 or higher.

- Recognize that solvency and liquidity measure different things: solvency looks at your ability to meet long-term debts over years, while liquidity focuses on paying short-term bills within the next 12 months.

- Improve solvency by attracting investors, restructuring debt, and cutting costs; boost liquidity by tracking cash flow closely, sending invoices promptly, and building a cash reserve covering three to six months of expenses.

- Use accounting software to track your cash, assets, and liabilities in real time, so you can make informed decisions about daily operations and long-term financial planning.

What does liquidity mean in business?

Liquidity measures your business's ability to pay bills and loan repayments in the short term, typically within 12 months. A business with strong liquidity can cover its immediate expenses without selling long-term assets or taking on new debt.

Liquidity ratios compare current liabilities (debts due within a year) against current assets (cash, inventory, receivables, and quickly sellable assets). The most common ratios include the cash ratio, quick ratio, and current ratio.

Other liquidity ratios

Small businesses commonly use three liquidity ratios:

- Current ratio: Measures all current assets divided by current liabilities. A ratio of 1.5 or higher indicates good short-term financial health.

- Quick ratio (acid test): Measures only assets convertible to cash within three months (cash, short-term investments, and receivables) divided by current liabilities. A ratio below 1.0 signals that current liabilities exceed easily convertible assets.

- Cash ratio: Measures cash and cash equivalents divided by current liabilities. This is the most conservative liquidity measure.

Learn more in the guide on liquidity ratios.

How liquid are your assets?

Asset liquidity refers to how quickly you can convert an asset to cash without losing value.

Most liquid assets convert to cash within days. These include the following:

- Cash: Includes physical currency and immediately accessible bank funds.

- Accounts receivable: Includes outstanding invoices, though liquidity decreases with longer payment terms that can signal issues with cashflow.

Less liquid assets take weeks or months to sell. These require more time to find buyers:

- Physical assets: Includes buildings, equipment, and machinery that require time to find buyers.

Liquidity vs other financial concepts

Liquidity measures your ability to cover short-term costs using available assets. While related to other financial metrics, liquidity focuses specifically on your capacity to pay immediate obligations.

Liquidity relates to several other financial metrics. Related concepts include:

- Cash flow: Tracks money moving in and out of your business over time.

- Working capital: Shows money remaining after covering short-term obligations, with ideal targets for working capital per dollar of sales varying from 10% for cafes to over 20% for manufacturers.

- Free cash flow: Represents cash remaining after capital investments.

How does liquidity affect business growth?

Strong liquidity supports business growth in several ways. It helps you:

- Seize opportunities quickly: Launch new products or hire staff without waiting for external funding.

- Handle unexpected costs confidently: Cover emergency repairs or equipment failures from existing reserves.

- Maintain operational stability: Avoid scrambling for cheaper suppliers or emergency financing when cash runs low.

What is solvency?

Solvency measures your business's ability to meet its long-term financial obligations. It shows whether your total assets are greater than your total liabilities over the long haul.

While liquidity looks at the cash you need for the next few months, solvency looks years ahead. A solvent business has a strong foundation and can sustain operations, even during economic downturns.

Solvency ratios

Solvency ratios help you evaluate your long-term financial health. They focus on your long-term debt compared to your assets or equity, with a healthy debt-to-asset ratio generally being less than 1 to indicate that total assets can adequately finance all debt.

By calculating these ratios, you can see how much of your business is funded by debt versus what you actually own. This gives you a clear picture of your financial stability.

Why solvency matters for long-term stability

Table of the difference between solvency and liquidity

Maintaining good solvency is essential for the survival and growth of your business. It builds credibility with lenders and investors, showing them you manage debt responsibly.

When your business is solvent, you have the resilience to weather tough times. It provides a solid base so you can confidently plan to expand in the future.

The main differences between solvency and liquidity

Solvency measures your ability to meet long-term financial obligations, while liquidity measures your ability to pay short-term bills. Both metrics matter, but they answer different questions about your financial health.

Solvency ratio formula

The key differences are:

- Timeframe: Solvency looks at years ahead; liquidity looks at the next 12 months.

- Focus: Solvency compares total assets to total debts; liquidity compares current assets to current liabilities.

- Risk indicator: Poor solvency signals bankruptcy risk; poor liquidity signals cash flow problems.

The comparison below outlines these differences in detail.

Table of the difference between solvency and liquidity

How to measure solvency and liquidity in your business

Measuring solvency and liquidity helps you track financial health and make informed decisions about borrowing, investing, and daily operations.

Use solvency ratios when assessing long-term stability or preparing to apply for loans. Use liquidity ratios when managing cash flow or evaluating short-term payment capacity.

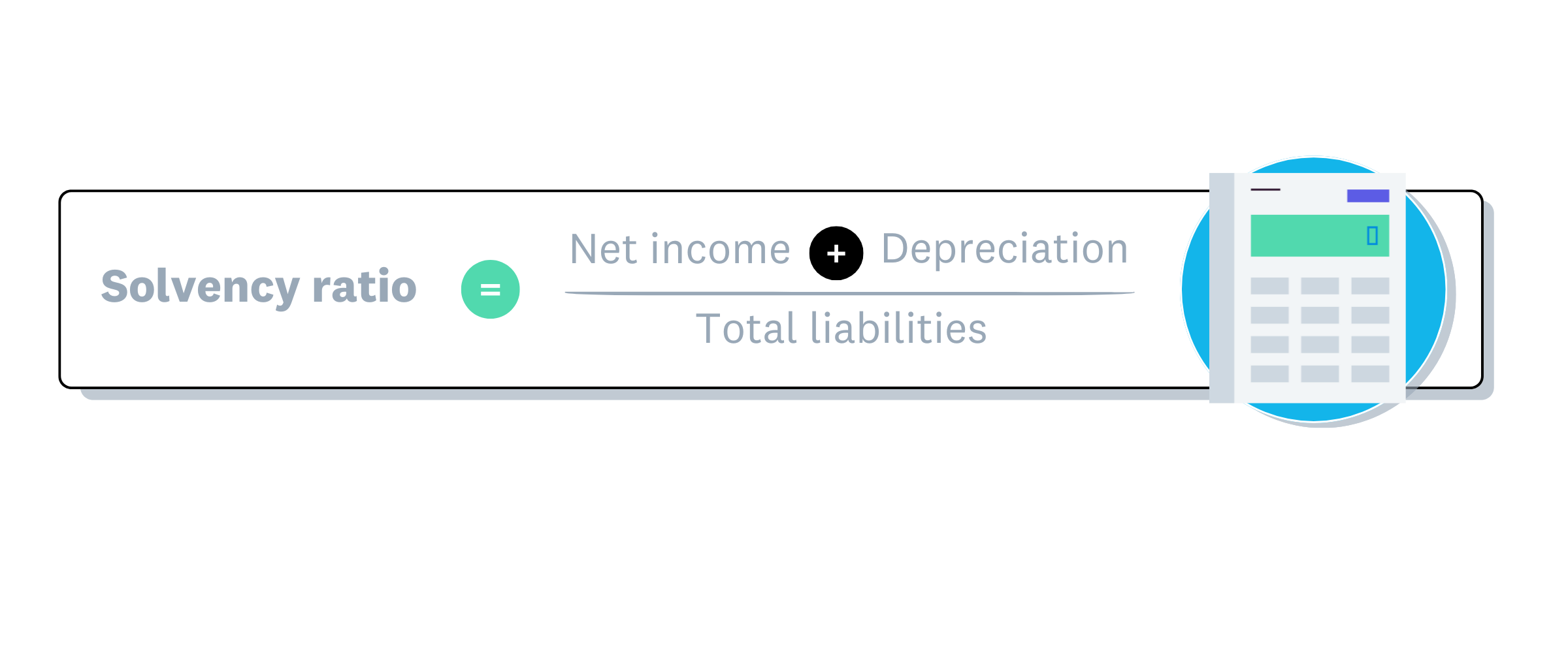

Solvency ratio formula

Solvency ratio formula

Example: Calculating a solvency ratio

Martha owns a cafe with these figures:

- Net income: $50,000

- Asset depreciation: $10,000

- Total liabilities: $300,000

Calculation: ($50,000 + $10,000) ÷ $300,000 = 20%

Result: Martha's 20% solvency ratio meets the benchmark many lenders consider healthy. Her business has a good chance of paying its debts over time.

\Depreciation represents the decrease in asset value from normal wear and tear, recorded on your balance sheet by deducting from the asset's value.*

Liquidity ratio formula

There are several liquidity ratios, including the cash ratio, quick ratio, and working capital ratio. Each one gives you a slightly different view of your short-term financial position.

Working capital ratio formula:

Example: Calculating a liquidity ratio

Sadiq runs a sports shop with these figures:

- Current assets: $120,000

- Current liabilities: $80,000

Calculation: $120,000 ÷ $80,000 = 1.5

Result: Sadiq's current ratio of 1.5 indicates he can likely meet his short-term financial commitments. While a ratio of 2.0 is often cited as ideal, acceptable current ratios depend on the industry, making 1.5 a healthy result for most small businesses.

Why solvency and liquidity matter for your small business

Understanding both metrics helps you spot problems early and make better decisions.

Signs of poor financial health:

- Poor liquidity creates immediate payment problems, such as missing payroll or supplier payments due to slow customer collections.

- Poor solvency indicates long-term financial trouble and increases bankruptcy risk when total debts exceed assets, though eligible businesses with under $1 million in debt may choose to restructure.

Benefits of strong financial health:

- Strong liquidity provides cash to pay suppliers and staff while protecting against unexpected costs.

- Strong solvency builds credibility with lenders and supports sustainable growth.

For more information on insolvency, see Australian government information on insolvency.

Tips to improve your financial solvency and liquidity

You can take several steps to strengthen your solvency and liquidity.

Improve your solvency:

- Attract investors: Bring in equity capital to strengthen your asset-to-liability ratio.

- Restructure debt: Renegotiate or refinance existing loans for better terms and lower interest rates.

- Optimise operations: Reduce costs by improving efficiency and eliminating waste.

Improve your liquidity:

- Track cash flow: Monitor daily cash movements to identify patterns and prevent shortfalls.

- Speed up collections: Send invoices promptly and follow up on overdue payments.

- Maintain reserves: Build a cash buffer to cover three to six months of operating expenses.

FAQs on solvency and liquidity

Here are answers to common questions about solvency and liquidity.

What's the difference between solvency and liquidity?

Solvency measures your ability to meet long-term financial obligations by comparing total assets to total liabilities. Liquidity measures your ability to pay short-term bills within 12 months by comparing current assets to current liabilities.

What is a good solvency ratio?

A solvency ratio of 20% or above is generally considered healthy. This shows you have sufficient earnings and assets to cover your long-term debts.

What is a good liquidity ratio?

A current ratio of 1.5 or higher indicates good liquidity for most small businesses. However, acceptable ratios vary by industry, with some sectors operating successfully at lower levels.

How can I improve my business's solvency?

Improve solvency by attracting investors to increase equity, restructuring debt for better terms, reducing operational costs, and increasing profitability through improved sales or pricing strategies.

How can I improve my business's liquidity?

Enhance liquidity by tracking cash flow closely, speeding up invoice collections, negotiating better payment terms with suppliers, maintaining cash reserves, and reducing unnecessary inventory.

Can a business be solvent but not liquid?

Yes. A business can have more assets than liabilities (solvent) but lack enough cash to pay immediate bills (illiquid). This often happens when assets are tied up in inventory or property that can't be quickly converted to cash.

Get one month free

Purchase any Xero plan, and we will give you the first month free.