Cash vs accrual accounting: differences, pros and cons

Learn how cash and accrual accounting differ and which method fits your small business.

Published Thursday 23 July 2026

Table of contents

Key takeaways

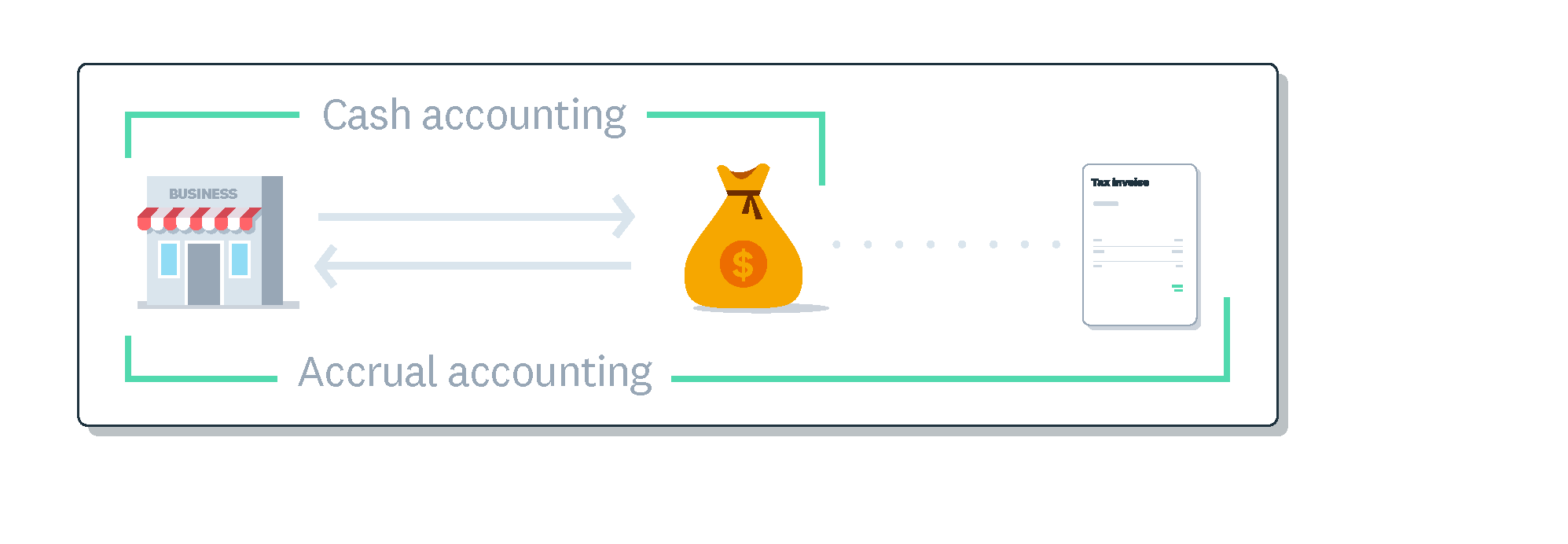

- Cash basis accounting records income and expenses when money changes hands. Accrual accounting records them when they're earned or owed, regardless of payment timing.

- Small businesses with under $30 million in average annual gross receipts can generally choose either method for IRS tax purposes.

- Cash accounting is simpler and shows your real-time cash position, while accrual accounting gives a more complete picture of your financial health over time.

- If your business is growing, carries inventory, or needs financing, accrual accounting is usually the better long-term fit.

What is cash basis accounting?

Cash basis accounting records revenue when you receive payment and expenses when you pay them. It's the simpler of the two methods and focuses on actual cash flowing in and out of your business.

Most freelancers, sole proprietors, and small service businesses start with cash basis accounting. It's straightforward and doesn't require tracking unpaid invoices or bills separately. If you're just getting started, the small business accounting guide covers the essentials.

Here's a quick example. Say you're a freelance designer and you finish a $5,000 project in March. Your client pays you in April. With cash accounting, you'd record that $5,000 as April income, because that's when the money hit your bank account.

The same logic applies to expenses. If you buy $500 in software in June but pay the bill in July, you'd record the expense in July.

What is accrual accounting?

Accrual accounting records revenue when you earn it and expenses when you incur them, even if no money has changed hands yet. It gives you a fuller picture of your financial commitments at any point in time.

Growing businesses, companies that carry inventory, and any business that needs to follow Generally Accepted Accounting Principles (GAAP) typically use accrual accounting. It's also the method most investors and lenders expect to see.

Using the same example: you finish a $5,000 design project in March and get paid in April. With accrual accounting, you'd record the $5,000 as March income, because that's when you earned it. The payment date doesn't change when the revenue is recognized.

For expenses, that $500 software purchase in June gets recorded in June, even if you don't pay until July. Your books reflect the obligation as soon as it exists. You can learn more about how this works in the recording accounting transactions guide.

Cash vs accrual accounting: key differences

Cash accounting focuses only on cash changing hands, not outstanding bills or invoices.

The core difference between cash and accrual accounting comes down to timing. Here's how they compare across four key areas.

Timing of revenue and expense recognition

The biggest difference is when each method records a transaction.

- Cash basis records transactions when money is received or paid

- Accrual basis records transactions when they're earned or incurred

- This timing gap can create very different financial snapshots of the same business

Financial accuracy

Each method paints a different picture of how your business is performing.

- Cash basis shows your actual bank balance but may miss money you're owed or bills you haven't paid

- Accrual basis gives a more complete view of profitability by matching revenue with the expenses that created it

- Accrual is generally seen as more accurate for measuring business performance over time

Complexity

The two methods require different levels of bookkeeping effort.

- Cash basis is simpler to set up and maintain, especially for small businesses without an accountant

- Accrual basis requires tracking accounts receivable and accounts payable, plus adjusting entries

- Cloud accounting software like Xero makes accrual accounting much easier to manage day to day

GAAP compliance

Your choice of method also affects whether your financials meet reporting standards.

- Cash basis is not GAAP compliant

- Accrual basis is the only method that meets GAAP standards

- Businesses seeking outside investment or loans often need GAAP-compliant financials

Pros and cons of cash accounting

Cash accounting has clear strengths for small and simple businesses, but it also has limits that can hold you back as you grow.

Advantages of cash accounting

Cash accounting keeps things simple for day-to-day operations.

- Simple to set up and maintain with minimal bookkeeping knowledge

- Shows exactly how much cash you have right now

- Gives you some flexibility on tax timing by controlling when you receive payments or pay bills

- Works well for businesses with straightforward, pay-as-you-go transactions

Disadvantages of cash accounting

The simplicity of cash accounting comes with some trade-offs.

- Doesn't show money your customers owe you or bills you haven't paid yet

- Can make profitable months look unprofitable (and vice versa) depending on payment timing

- Not accepted under GAAP, which can limit your options for financing or partnerships

- Harder to plan ahead because your books don't reflect future financial commitments

Pros and cons of accrual accounting

Accrual accounting gives you a more detailed financial picture, but it does come with added complexity.

Advantages of accrual accounting

Accrual accounting offers benefits that support long-term growth.

- Matches revenue with the expenses that generated it, giving a truer view of profitability

- Meets GAAP standards, which investors, lenders, and partners often require

- Makes it easier to spot trends and plan for the future

- Scales with your business as transactions get more complex

Disadvantages of accrual accounting

Accrual accounting does require more hands-on management.

- More complex to set up and maintain, especially without accounting software

- Your profit and loss statement might show strong revenue while your bank balance is low

- Requires tracking receivables and payables, plus period-end adjustments

- May need professional help to manage correctly, adding to your costs. A small business bookkeeper can handle the complexity for you

How to choose the right accounting method

The right method depends on your business today and where you want it to go. Think about these five factors before you decide.

Business size and growth plans

If you're a freelancer or sole proprietor with simple finances, cash basis is often enough. But if you're planning to hire, expand, or take on bigger projects, accrual gives you a stronger foundation.

Inventory

If your business buys and sells products, the IRS generally requires you to use accrual accounting to track inventory costs properly. The developing an accounting system guide walks through how to set this up. This is one of the clearest triggers for switching methods.

IRS revenue thresholds

The IRS allows most small businesses to use cash accounting as long as your average annual gross receipts are $30 million or less over the prior three tax years. Once you cross that threshold, you'll need to switch to accrual.

Financing and investor expectations

Banks and investors typically want to see accrual-based financial statements. If you're planning to apply for a loan, seek funding, or bring on partners, accrual accounting makes your financials more credible.

GAAP compliance

If your industry or business structure requires GAAP-compliant reporting, accrual is your only option. This applies to publicly traded companies and many businesses working with government contracts.

When to switch from cash to accrual accounting

Many small businesses start with cash accounting and switch to accrual as they grow. Here are a few signs it might be time to make the change.

Signs you've outgrown cash accounting

Watch for these indicators that cash accounting no longer fits your needs.

- You're carrying inventory and need to track cost of goods sold

- Your revenue is approaching the $30 million IRS threshold

- You're applying for business loans or looking for investors

- Your cash flow timing makes it hard to see true profitability

- You need GAAP-compliant financials for contracts or partnerships

How to make the switch

To change your accounting method with the IRS, you'll need to file Form 3115, Application for Change in Accounting Method. This form notifies the IRS and helps you adjust for any income or expenses that would otherwise be counted twice or missed entirely.

Plan your switch at the start of a new tax year to keep things clean. Work with an accountant or find an advisor to calculate your Section 481(a) adjustment, which accounts for the differences between your old and new methods. Cloud accounting software like Xero can make the transition smoother by automatically tracking receivables and payables from day one.

Track your finances with confidence using Xero

Whether you use cash or accrual accounting, the right software makes managing your books faster and easier. Xero gives you real-time visibility into your finances, automates everyday tasks like bank reconciliation and invoicing, and grows with your business as your needs change. Get one month free.

FAQs on cash vs accrual accounting

Here are answers to frequently asked questions about cash vs accrual accounting.

Is GAAP accounting accrual or cash basis?

GAAP requires accrual accounting. Under GAAP, revenue and expenses must be recorded when they're earned or incurred, not when cash changes hands. If your business needs GAAP-compliant financial statements, you'll need to use the accrual method.

Can you switch from cash to accrual accounting?

Yes, you can switch from cash to accrual accounting. You'll need to file IRS Form 3115 to request the change. It's best to make the switch at the start of a new tax year and work with an accountant to handle the transition smoothly.

What is modified cash basis accounting?

Modified cash basis is a hybrid method that blends elements of both cash and accrual accounting. It typically records day-to-day transactions on a cash basis but uses accrual methods for longer-term items like fixed assets and loans. It's not GAAP compliant, but some small businesses find it a practical middle ground.

Does the IRS require accrual accounting?

The IRS doesn't require all businesses to use accrual accounting. Most small businesses with average annual gross receipts of $30 million or less can choose either method. However, businesses that carry inventory or exceed the $30 million threshold generally must use accrual.

Do banks prefer cash or accrual accounting?

Banks generally prefer accrual accounting when reviewing loan applications. Accrual-based financials give a more complete picture of your revenue, expenses, and overall financial health. If you're planning to apply for financing, having accrual-based statements can strengthen your application.

Related terms

Explore more accounting terms and definitions in the Xero glossary.

Learn more about small business accounting

Dive deeper into accounting and bookkeeping with these Xero guides.

Handy resources

Advisor directory

You can search for experts in our advisor directory

Xero Small Business Guides

Discover resources to help you do better business

Financial reporting

Keep track of your performance with accounting reports

Disclaimer

This glossary is for small business owners. The definitions are written with their requirements in mind. More detailed definitions can be found in accounting textbooks or from an accounting professional. Xero does not provide accounting, tax, business or legal advice.