Cash flow forecasting: what it is and how to do it

Learn how to forecast cash flow, spot shortfalls early and keep your business finances on track.

Written by Jotika Teli—Certified Public Accountant with 24 years of experience. Read Jotika's full bio

Published Monday 29 June 2026

Table of contents

Key takeaways

- Update your cash flow forecast at least monthly, or weekly if cash is tight, by recording your starting balance, estimating money coming in, scheduling payments going out and calculating your running balance to stay ahead of any shortfalls.

- Use the direct method for short-term, day-to-day cash management because it tracks actual transactions by date and gives you a clear picture of your cash position without needing advanced accounting knowledge.

- Avoid common pitfalls like over-optimistic revenue projections, ignoring seasonal patterns and confusing profit with cash flow, all of which can make your forecast unreliable.

- Use both a cash flow forecast and a budget together; your forecast tells you whether you'll have enough cash to pay bills on time, while your budget keeps your spending and income targets on track.

What is a cash flow forecast?

A cash flow forecast predicts when money will move in and out of your business over a set period. It shows your future financial position so you can make confident decisions about spending, investments and growth.

Understanding the differences between related terms helps you choose the right tool for your needs.

- Cash flow forecast: predicts future money movements over weeks or months

- Cash flow statement: records past transactions that have already occurred. See the guide to cash flow statements for more detail

- Cash flow projection: extends predictions further into the future, often a year or more

How does cash flow forecasting work?

Cash flow forecasting tracks expected money movements over a set period. It calculates your running cash balance to predict your future financial position.

The process follows this cycle:

- Record your starting cash balance from your bank accounts.

- Estimate incoming cash based on outstanding invoices, expected sales and other income. Keep in mind that many businesses operate payment terms ranging from 30 to 90 days before invoices are paid. Data from Xero Small Business Insights shows UK small businesses wait an average of 29 days to be paid, with invoices arriving 8.2 days late on average. These delays can quickly create cash gaps if your forecast doesn't account for them.

- Schedule outgoing payments including bills, payroll, loan repayments and planned purchases.

- Calculate your ending balance by adding income and subtracting expenses from your starting balance.

- Review and adjust as actual results come in.

Most businesses repeat this cycle weekly or monthly, rolling the forecast forward as each period completes. The more consistently you update your forecast, the more accurate your predictions become.

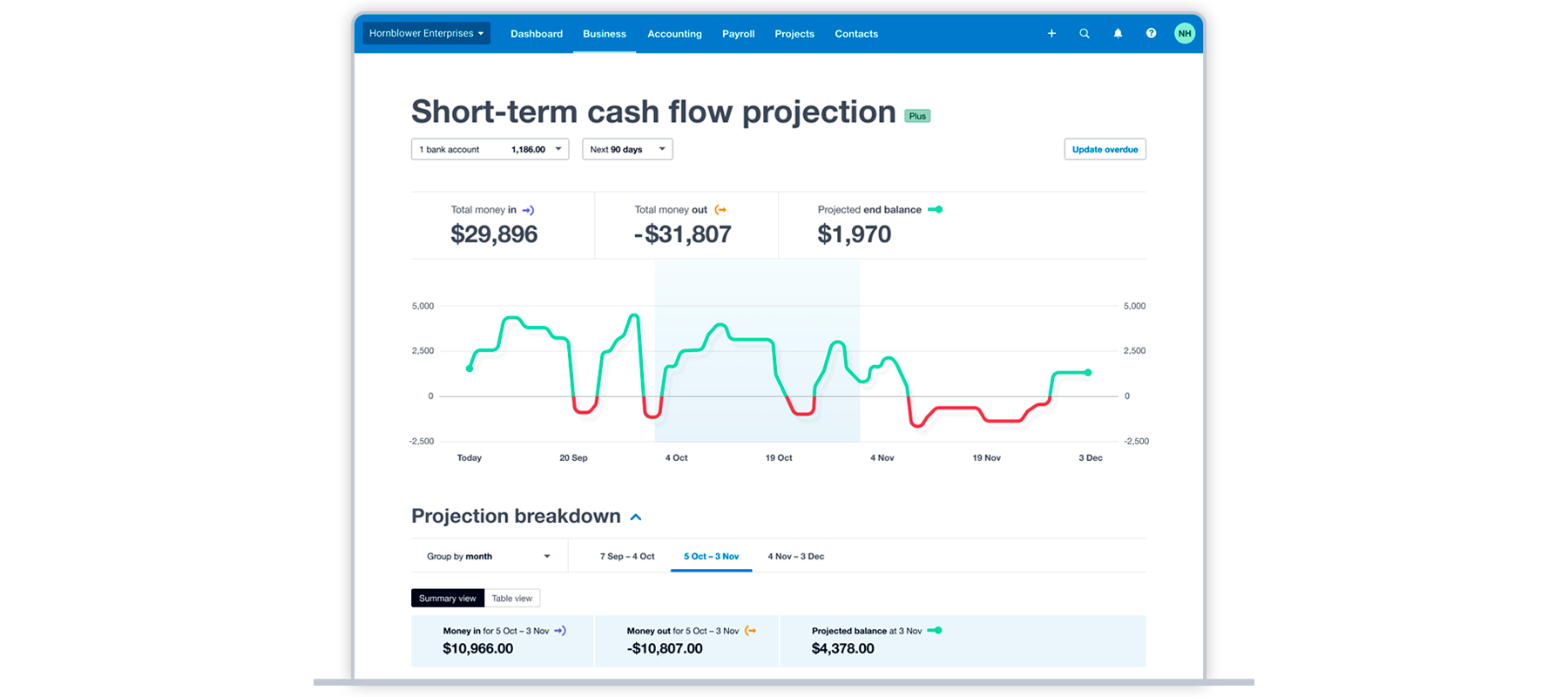

A cash flow dashboard shows how cash balances will rise and fall in response to expected transactions.

Why is cash flow forecasting important?

Cash flow forecasting helps you avoid financial surprises by showing exactly when money will arrive and when bills are due. This visibility lets you pay bills on time, ensure you can pay yourself and spot potential shortages before they become problems. This practice is supported by ongoing improvements in liquidity risk reporting, as highlighted in recent FRC reviews of smaller listed companies.

During uncertain times, forecasting becomes even more valuable.

- Anticipate how rising costs will affect your cash position

- Identify financial gaps weeks or months before they occur. According to Xero Small Business Insights, UK small business sales growth has slowed to just 2.9% year-on-year, the smallest rise in two years

- Make proactive decisions about spending and investments

Benefits of a cash flow forecast

Cash flow forecasting gives you financial control by revealing your future cash position before problems arise. Effective financial management starts with knowing what's coming. Here are the main advantages of keeping a regular forecast.

- Spot shortages early: identify cash gaps weeks or months ahead, giving you time to secure funding or negotiate payment terms

- Plan for growth: determine if you can afford new equipment, staff or expansion without risking your cash position. Read more about avoiding cash flow problems

- Protect your pay: ensure you can consistently pay yourself while covering business expenses

- Identify trends: recognise rising expenses or declining income before they threaten your business

- Find hidden problems: uncover issues like slow-paying customers, poor payment terms or seasonal gaps. For example, Xero Small Business Insights data from 440,000 UK small businesses shows invoices are paid an average of 8.2 days late. That pattern is hard to spot without a forecast tracking expected versus actual payment dates

- Build contingency plans: prepare responses for predicted cash flow dips

Types of cash flow forecasting

Small businesses typically choose between two main forecasting methods, depending on their needs and the level of detail required.

Direct method (receipts and disbursements)

The direct method tracks actual cash transactions as they happen. You list specific incoming payments and outgoing expenses by date.

This method offers these advantages:

- Best for short-term forecasts (weekly or monthly)

- Gives precise visibility into your daily cash position

- Ideal for managing immediate cash needs

Indirect method

The indirect method starts with your profit and loss statement, then adjusts for non-cash items like depreciation and changes in working capital.

This method has these characteristics:

A cash flow dashboard shows how cash balances will rise and fall in response to expected transactions.

- Better suited for longer-term forecasts

- Useful for strategic planning and investor reporting, as the majority of companies now disclose key liquidity information such as availability of cash and undrawn borrowing facilities

- Requires more accounting knowledge to set up

Which method should you use?

Most small businesses find the direct method easier and more practical for day-to-day cash management. The indirect method becomes more useful as your business grows. It's particularly helpful when you need forecasts for loan applications or investor discussions.

Cash flow forecasts vs budgets: what's the difference?

Cash flow forecasts and budgets are both essential financial tools, but they serve different purposes. Understanding how they work together gives you a stronger foundation for business planning.

A cash flow forecast focuses on the timing of money moving in and out of your business. Its purpose is ensuring you have sufficient cash to pay bills and avoid shortfalls. You'd typically forecast weekly or monthly for the next three to 12 months. The key question it answers: will you have enough money when you need it?

A budget, on the other hand, focuses on planned earnings and spending over a period. Its purpose is setting financial goals and controlling spending. You'd usually set an annual budget with monthly or quarterly reviews. The key question it answers: are you staying on track with your financial goals?

You need both tools working together. Budgets help you set financial targets, while cash flow forecasts ensure you can pay your bills on time.

What are the key components of a cash flow forecast?

Every cash flow forecast includes five essential components that track your money from start to finish.

- Starting balance: the cash you have at the beginning of the forecast period

- Money coming in: expected income from sales, loans, grants or asset sales

- Money going out: planned expenses including bills, payroll, loan payments and purchases

- Net cash flow: the difference between money in and money out for the period

- Ending balance: the cash you'll have at the end of the period

How to create a cash flow forecast

Creating a cash flow forecast helps you plan your finances with confidence. Here's how to build one for any period, from a week to a year.

Follow these four steps:

- Estimate when you'll receive payments from customers.

- List when bills and expenses are due.

- Calculate your running cash balance day by day or month by month.

- Track everything using spreadsheets or accounting software.

For longer forecasts, review previous quarters or years to make your estimates more accurate.

Creating a cash flow forecast spreadsheet

A spreadsheet is one of the simplest ways to start forecasting. Here's how to build your forecast step by step.

- Choose your forecast period and record your starting balance. You can forecast for a month or a year.

- List and date all expected cash income. Include sales receipts, grants, loan proceeds and any other money coming in.

- List and date all expected cash outflows. Include rent, payroll, supplier payments, loan repayments, taxes and other expenses.

- Calculate your running balance. Start with your opening balance, add income, subtract expenses and track your balance for each period.

- Review and update regularly. Compare actual results with your forecast and adjust future projections based on what you learn.

Cash flow forecast example

Seeing the numbers in action makes cash flow forecasting easier to understand. Here's a simple one-month forecast for a small business.

Start with your opening balance. In this example, you begin the month with 5,000 pounds in the bank.

Next, add up your expected cash inflows for the month:

- Customer payments from invoices: 8,000 pounds

- Other income (for example, a small grant): 500 pounds

- Total cash in: 8,500 pounds

Then list your expected cash outflows:

- Rent: 1,200 pounds

- Salaries: 3,500 pounds

- Supplier payments: 2,000 pounds

- Other costs (utilities, insurance, subscriptions): 800 pounds

- Total cash out: 7,500 pounds

Now calculate your net cash flow and closing balance:

- Net cash flow: 8,500 pounds in minus 7,500 pounds out = 1,000 pounds positive

- Closing balance: 5,000 pounds opening + 1,000 pounds net = 6,000 pounds

This tells you the business will end the month with 6,000 pounds in the bank. If that closing balance were negative, you'd know to take action now, whether that means chasing outstanding invoices, delaying a purchase or arranging a short-term facility.

Cash flow forecasting best practices

A cash flow forecast is only useful if you keep it accurate and up to date. These tips will help you get the most from your forecasting.

- Update regularly: review and refresh your forecast at least monthly. If cash is tight, switch to weekly updates so you can react quickly to changes

- Use realistic assumptions: base your income estimates on actual payment patterns rather than best-case scenarios. If your customers typically pay in 30 days, don't assume they'll pay in 14

- Track actuals against your forecast: compare what actually happened with what you predicted each month. This helps you spot where your assumptions are off and improve future accuracy

- Plan for different scenarios: create best-case, worst-case and most-likely versions of your forecast. This prepares you for unexpected changes in income or costs

- Involve your accountant or bookkeeper: they can help you spot patterns, validate assumptions and ensure nothing important is missing from your forecast

- Use accounting software: tools like Xero connect to your bank accounts, track invoices automatically and give you a real-time view of your cash position, saving hours of manual work

- Understand your cash flow drivers: identify which customers, products or seasons have the biggest impact on your cash position so you can focus your attention where it matters most

Common cash flow forecasting mistakes to avoid

Even a well-structured forecast can lead you astray if you fall into these common traps. Knowing what to watch for helps you keep your forecast reliable.

- Over-optimistic revenue projections: it's tempting to forecast based on your best month, but this can give you a false sense of security. Use conservative estimates and adjust upward only when you have confirmed orders or contracts

- Ignoring seasonal patterns: many small businesses see predictable dips and peaks throughout the year. If you don't factor in quieter months, you may be caught short when expenses stay steady but income drops

- Confusing profit with cash flow: your business can be profitable on paper and still run out of cash. A sale isn't cash until the customer pays, so always forecast based on when money actually arrives, not when you issue the invoice

- Not updating the forecast: a forecast you created three months ago and never revisited is little more than guesswork. Set a recurring reminder to review and adjust your numbers at least monthly

- Overlooking payment delays: if your customers regularly pay late, your forecast needs to reflect that. Build in realistic payment timelines rather than assuming everyone will pay on the due date. Strategies like automated payment reminders can help speed up collections

Manage your cash flow with confidence using Xero

Cash flow forecasting doesn't have to be complicated or time-consuming. With the right tools, you can stay on top of your finances and focus on growing your business.

Xero's cloud accounting software connects directly to your bank, tracks invoices and expenses in real time and gives you a clear picture of your cash position at any moment. Whether you're forecasting for the next month or planning a full year ahead, Xero helps you make confident financial decisions; get one month free.

FAQs on cash flow forecasting

Here are answers to frequently asked questions about cash flow forecasting.

How often should I update my cash flow forecast?

Update at least monthly, or weekly if cash is tight or your business is seasonal. Trigger an extra update whenever something unexpected happens, such as losing a major client, receiving a large order or facing an unplanned expense.

What's the ideal timeframe for a cash flow forecast?

Most small businesses use a 13-week rolling forecast for day-to-day cash management, while a 12-month view suits investment planning or finance applications. New businesses often start with four to six weeks and extend as their data grows.

Can I create a cash flow forecast without accounting software?

Yes, a spreadsheet works for simple forecasts, though you'll need to update figures manually and watch for formula errors. Accounting software pulls live bank data automatically, keeping your forecast current without the manual work.

What is the difference between a cash flow forecast and a cash flow statement?

A forecast looks forward, estimating money coming in and going out over the weeks or months ahead, while a cash flow statement records what actually happened in a past period. Used together, they help you compare predictions against reality and sharpen your forecasting over time.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Get one month free

Purchase any Xero plan, and we will give you the first month free.