Cost of sales: what it is and how to calculate yours

Learn what cost of sales is, how to calculate it, and how to use it to protect your profit margins.

Written by Lena Hanna—Trusted CPA Guidance on Accounting and Tax. Read Lena's full bio

Published Wednesday 27 May 2026

Table of contents

Key takeaways

- Cost of sales covers only the direct costs of delivering your products or services, such as raw materials, production labour, and shipping. Keeping it separate from overheads gives you a true profit baseline.

- The universal formula for most businesses is: beginning inventory + purchases during the period, minus ending inventory. Service businesses swap inventory values for direct labour and delivery costs.

- Consistent categorisation is essential. If you change how you classify borderline costs like freight or commissions, your financial reports become unreliable and harder to compare over time.

- Regularly reviewing your cost of sales helps you set accurate prices, spot rising expenses early, and make confident decisions about suppliers, processes, and product lines.

What is cost of sales?

Understanding your cost of sales is one of the most practical steps you can take to protect your profit margins. It tells you exactly how much it costs to deliver what you sell.

Cost of sales is the total expense directly linked to producing or delivering your products or services. It includes raw materials, direct labour, packaging, and shipping.

This figure sets your minimum pricing threshold and directly affects your profit margins. It also serves as a reliable metric for predicting business turnover.

For most small businesses, cost of sales is the same as direct costs: expenses tied to the goods or services you sell. These differ from indirect costs, which are general expenses not related to production or delivery.

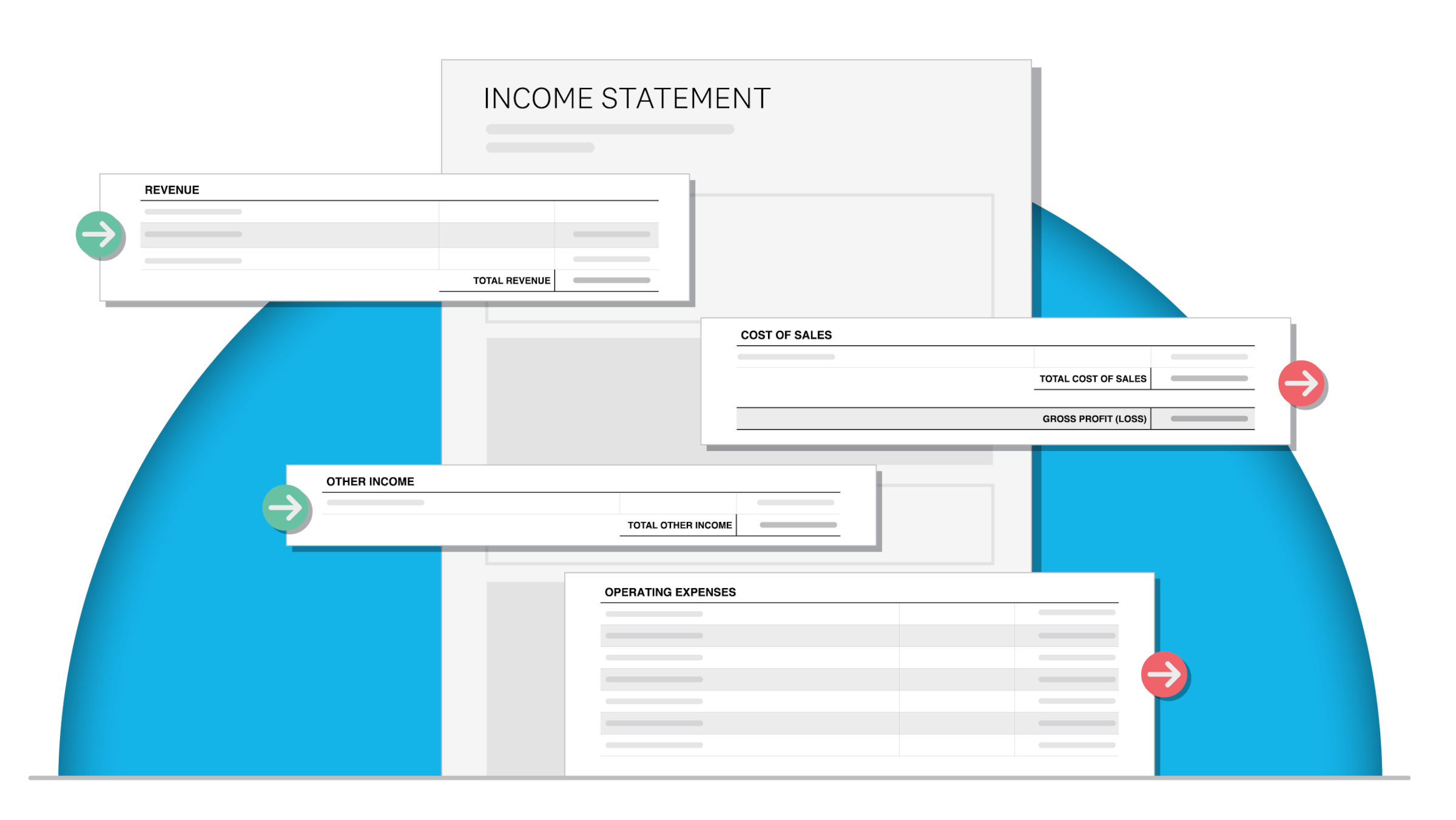

Cost of sales vs cost of goods sold (COGS)

You'll often see "cost of sales" and "cost of goods sold" (COGS) used interchangeably. In most contexts, they mean the same thing. However, there's a subtle distinction worth knowing.

COGS traditionally refers to the direct costs of producing physical goods. Cost of sales is the broader term that also covers service delivery costs, such as labour, software, and travel expenses. If you run a service business, "cost of sales" is the more accurate label.

For product-based businesses like retail or manufacturing, the two terms are effectively identical. The Australian Accounting Standards Board (AASB) uses the term "cost of inventories" under AASB 102, which aligns with COGS. Whichever term you use, the important thing is to apply it consistently across your financial reports.

Why is cost of sales important?

Cost of sales sets your profit baseline. You need to price above this figure to stay profitable, so tracking it regularly helps you make better pricing and spending decisions.

Monitoring your cost of sales helps you:

- Set accurate prices: establish your minimum viable price point so every sale covers its direct costs

- Protect profit margins: spot margin threats early, before they erode your bottom line

- Control rising costs: identify which expenses are growing fastest and take action

Labour costs, often the largest component of cost of sales, illustrate why regular monitoring matters. In the December quarter of 2025, wages across Australian small businesses grew +2.0% year-on-year. October and November averaged +2.8%, close to the long-term average of roughly 2.9%. For businesses where labour is a significant direct cost, even small wage shifts can compress margins if pricing doesn't keep pace.

If your annual cost of sales is $200,000 and you find a way to reduce it by $10,000, that saving flows straight to your gross profit. On $400,000 in revenue, your gross profit margin jumps from 50% to 52.5%, without needing to win a single new customer.

Cost of sales also affects your tax position. Because it's deducted from revenue to calculate gross profit, a higher cost of sales reduces your taxable income. Accurate tracking ensures you're claiming every legitimate deduction and not overpaying tax.

What to include in your cost of sales calculation

Getting an accurate cost of sales figure starts with knowing exactly which costs belong in the calculation and which don't.

These are the direct costs that belong in your cost of sales calculation:

- purchasing raw materials or stock

- paying wages for staff who directly make products or deliver services

- covering other direct costs, such as shipping for materials or software needed to do the work

According to Australian Accounting Standards, this covers all costs of purchase, conversion, and other expenses required to get inventory ready for sale.

You also need to know what to leave out. General business running costs, also called indirect costs or overheads, don't belong in your cost of sales.

These general business running costs should not be included in your cost of sales:

- administrative overheads

- marketing and advertising spend

- office rent and utilities

- selling costs

According to AASB 102, these costs are excluded from inventory calculations and must be recognised as expenses in the period they're incurred. Stay consistent in what you include so your reports remain reliable and support better business decisions.

Cost of sales vs. expenses

It's common to mix up cost of sales with general business expenses. They're both outgoings, but they serve different purposes in your financial reports.

Cost of sales covers only the expenses directly tied to creating and delivering your products or services. Business expenses, sometimes called operating expenses, cover everything else needed to run your company.

Cost of sales typically includes expenses like these:

- raw materials and inventory purchases

- direct labour costs

- packaging and shipping

- payment processing fees

Operating expenses, on the other hand, cover the indirect costs of running your business:

- marketing and advertising

- office rent and utilities

- administrative salaries

- professional services such as accounting and legal

To improve profit margins, focus on reducing your cost of sales first. To lower overall spending, look at your operating expenses separately.

How to calculate cost of sales

Before diving into industry-specific calculations, it helps to know the universal formula that applies to most businesses. The standard cost of sales formula is: cost of sales = beginning inventory + purchases during the period - ending inventory.

Follow these three steps to calculate your cost of sales for any given period.

1. Find your beginning inventory value

Start with the total value of stock, raw materials, or supplies you had on hand at the start of the period. For a candle-making business, this might be $8,000 in wax, wicks, and packaging.

2. Add purchases made during the period

Add the value of any new stock, raw materials, or direct costs you acquired during the period. In the candle-making example, this could be $5,000 in new supplies bought during the quarter.

3. Subtract your ending inventory value

Subtract the value of stock remaining at the end of the period. If $3,000 worth of supplies is left unsold, your cost of sales for the quarter is $8,000 + $5,000 - $3,000 = $10,000.

Service businesses use a variation of this formula. Instead of tracking inventory, you add up direct labour costs, subcontractor fees, and any tools or software required to deliver your services during the period.

Cost of sales calculations for different business types

While the core formula stays the same, the specific costs you track depend on your business type. Here's how the calculation works for service businesses, retailers, and manufacturers.

Service businesses

Service businesses don't sell physical products, so the calculation focuses on the direct costs of delivering services to clients. These typically include:

- wages for employees who deliver services

- facilities used for service delivery

- travel costs, if applicable

- equipment and software used for client work

Exclude back-office employees from your cost of sales. Travel and equipment costs only apply if you use them directly for client work.

Retailers

Retailers can use the standard cost of sales formula for inventory accounting. Australian Taxation Office (ATO) benchmarks for medium-sized retail businesses show cost of sales at an average of 52% of annual turnover. A typical retail calculation includes:

- beginning inventory value

- purchased inventory during the period

- shipping to customers

- transaction fees

Subtract your ending inventory value to calculate your cost of sales for the period.

Manufacturing

Manufacturers have raw materials and production costs to factor into their cost of sales calculations. Key costs to track include:

- raw materials

- manufacturing labour

- production overhead

- storage, if directly tied to production

- freight, if directly tied to production

You may exclude warehousing or freight if you treat them as operating expenses instead. The key is to be consistent in your approach so your reports stay comparable over time.

Cost of sales examples

Some costs are straightforward to classify, but others fall into grey areas. The test is simple: does this cost directly help you create or deliver your product or service?

For unique items, accounting standards require the specific identification of their individual costs.

Common grey areas include:

- Sales commissions: include if tied to specific sales; exclude if they're salary-based

- Equipment maintenance: include if equipment is used exclusively for production; exclude if it's shared across the business

- Freight costs: include if delivering to customers; exclude if receiving inventory

Be consistent in how you categorise these. If you change your approach mid-year, your tracking becomes unreliable.

Retail business example

Here's a practical example to show how cost of sales works in a retail setting.

Imagine you own a homeware store and want to price a new item: handmade pottery cups. Your direct costs per cup break down like this:

- Purchasing from supplier: $5 per cup

- Shipping to store: $2 per cup

- Employee labour for shelving and customer service: $3 per cup

Total cost of sales per cup: $10.

For a 50% markup, you'd set a retail price of $15 per cup. That gives you a $5 gross profit on each sale, or a gross profit margin of 33.3%.

Common mistakes when calculating cost of sales

Even small errors in your cost of sales calculation can throw off your pricing, profit margins, and tax reporting. Here are the most common mistakes to watch for.

- Including operating expenses. Rent, marketing, and admin salaries are overhead costs, not cost of sales. Mixing them in inflates your figure and distorts your gross profit margin.

- Forgetting inventory adjustments. If you don't account for opening and closing inventory values, your calculation won't reflect what you actually sold during the period.

- Misclassifying employee wages. Only include wages for staff who directly produce goods or deliver services. Back-office and administrative staff belong under operating expenses.

- Ignoring damaged or obsolete stock.Stock that can't be sold at full value needs to be written down. Leaving it at its original value overstates your inventory and understates your cost of sales.

- Categorising costs inconsistently. Changing how you classify borderline costs from one period to the next makes it impossible to compare your figures accurately. Pick a method and stick with it.

How to reduce your cost of sales

Lowering your cost of sales is one of the most direct ways to improve profitability. Every dollar you save on direct costs flows straight to your gross profit.

Here are practical strategies to consider:

- Negotiate with suppliers. Review your supplier agreements regularly. Even small discounts on bulk orders or early payment terms can add up over time.

- Reduce waste. Track where materials are being lost, damaged, or discarded during production. Tightening your processes can cut costs without affecting quality.

- Optimise inventory management. Holding too much stock ties up cash, and holding too little risks stockouts. Use inventory tracking tools to find the balance that keeps costs low and customers happy.

- Automate manual processes. Repetitive tasks like data entry, invoicing, and tracking expenses take time and introduce errors. Automating them saves labour costs and improves accuracy.

- Review your product mix. Not every product or service you offer is equally profitable. Focus on your highest-margin offerings and consider dropping or repricing low-margin lines.

Simplify your cost tracking with Xero

Business costs shift constantly, so a clear, real-time view of your finances helps you stay in control and make confident decisions.

Xero gives you a live view of your income and outgoings. With job costing in Xero Projects, you can track direct costs against specific jobs or clients. You can also run detailed profit and loss reports, monitor expense trends, and generate cash flow projections to plan ahead.

If you're ready to take the guesswork out of cost tracking, get one month free.

FAQs on cost of sales

Here are answers to frequently asked questions about cost of sales.

Is cost of sales the same as COGS?

The ATO uses "cost of sales" in its small business benchmarks and activity statements. If your accounting software uses "COGS" instead, the figures are interchangeable for tax reporting purposes.

Does cost of sales affect tax obligations?

Yes. If you miscategorise an operating expense as cost of sales, or vice versa, the ATO may query your return during a review. Keeping clear records of how you classify each cost helps you respond quickly if asked.

What's the difference between cost of sales and operating expenses?

On a profit and loss statement, cost of sales sits above the gross profit line, while operating expenses sit below it. Getting the split right matters because lenders and investors use gross profit margin to assess how efficiently you deliver your product or service.

Is cost of sales an expense or an asset?

Cost of sales is an expense. It appears on your profit and loss statement, not your balance sheet. While unsold inventory is classified as an asset, the cost transfers to cost of sales once the goods are sold.

How often should you review your cost of sales?

Monthly reviews work well for most small businesses. This gives you enough data to spot trends and react to rising costs before they significantly affect your margins.

Small business continues to adapt and grow*

Read the full report for Xero's small business insights focusing on several core performance metrics, including sales growth, jobs, time to be paid, and late payments.

AU sales:+3.7%*

Small business sales grew an average 3.7% y/y in the three months to September. Published 31 October 2024.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Start using Xero for free

Access Xero features for 30 days, then decide which plan best suits your business.