Gross pay vs net pay: what's the difference in the UK?

Learn gross pay vs net pay, and how to calculate each for clearer payroll and smarter cash flow.

Written by Jotika Teli—Certified Public Accountant with 24 years of experience. Read Jotika's full bio

Published Saturday 11 April 2026

Table of contents

Key takeaways

- Calculate your net pay by subtracting all deductions (income tax, National Insurance, pension contributions, and student loan repayments) from your gross pay to understand your actual take-home amount.

- Use gross pay figures when negotiating salaries or writing employment contracts, but base all personal financial decisions like budgeting and mortgage applications on your net pay since this reflects your actual spending power.

- Recognise that gross pay includes your base salary plus any additional earnings like overtime, bonuses, and commissions, while net pay is the actual amount deposited into your bank account after deductions.

- Utilise HMRC's income tax calculator or payroll software to accurately estimate net pay from gross pay, as the difference can be substantial (for example, £30,000 gross typically becomes around £25,000 net).

What is gross pay?

Gross pay is your total earnings before any deductions are removed. It's the figure you see in job adverts and employment contracts. Gross pay includes:

- Base salary: Your agreed annual or hourly wage

- Additional earnings: Overtime, bonuses, commissions, and allowances

- Taxable benefits: Cash allowances such as car allowances, or benefits in kind that may be taxed separately

When a job advertises £30k per annum, this refers to gross pay, not what you'll actually receive in your bank account.

What is net pay?

Net pay is the actual amount deposited into your bank account after all deductions. Also called take-home pay, it reflects your actual spending money after deductions.

The formula is straightforward:

Net pay = Gross pay − All deductions

Common deductions include:

- Income tax

- National Insurance contributions

- Pension contributions

- Student loan repayments

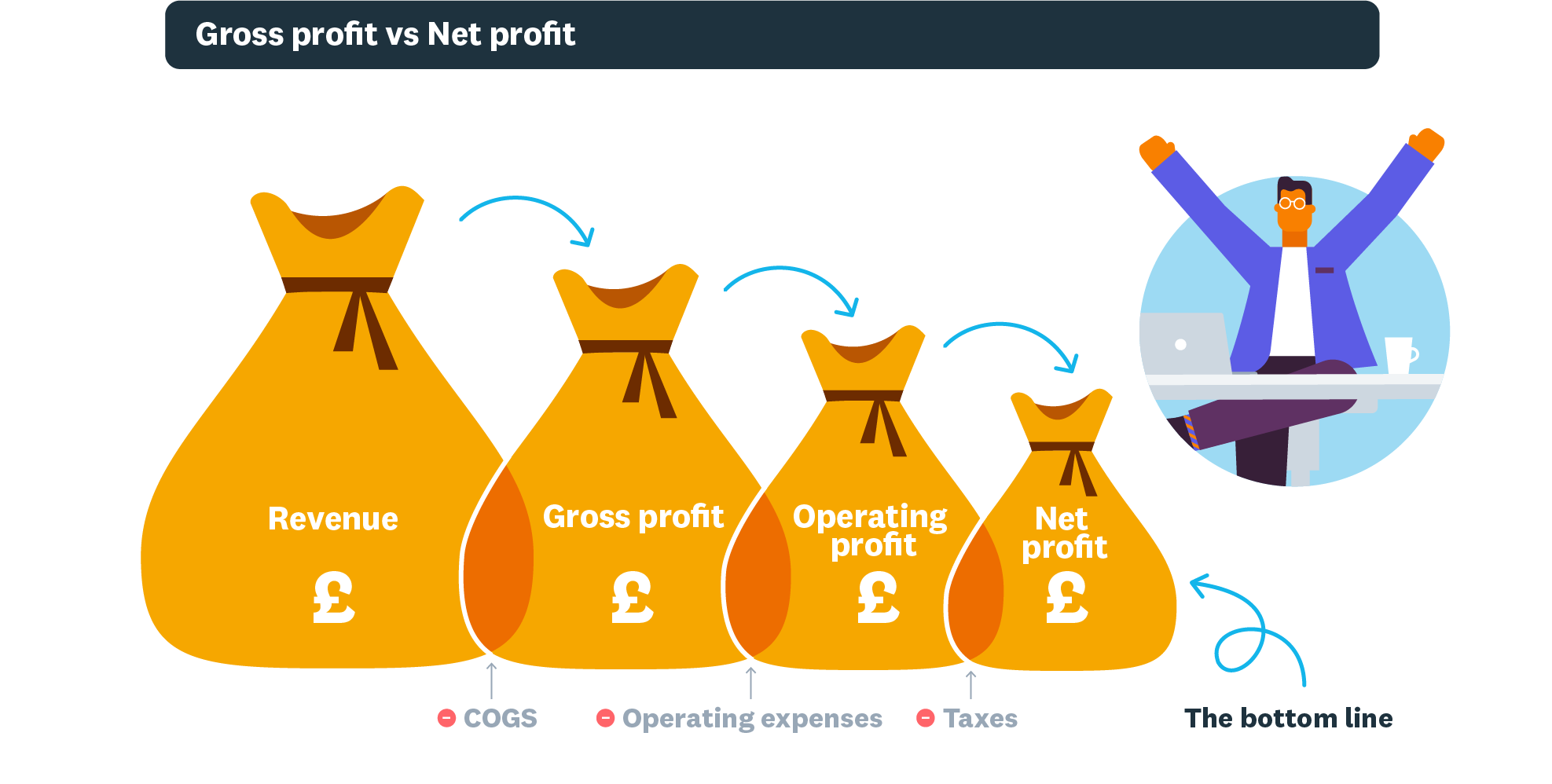

What deductions are taken from gross pay?

Deductions are amounts subtracted from your gross pay to calculate net pay. While these vary by individual circumstances, most UK employees see the following on their payslip.

Income tax

Income tax is a tax on your earnings collected by HMRC. The amount depends on how much you earn and your tax code.

Most people have a standard Personal Allowance of £12,570 per year, which is the amount of income you don't have to pay tax on. You don't pay income tax on earnings below this threshold.

National Insurance (NI)

National Insurance (NI) contributions build your entitlement to state benefits like the State Pension and Maternity Allowance. You pay National Insurance if you're an employee earning more than £242 per week from one job (2024/25 tax year). The amount depends on your employment status and earnings.

Pension contributions

Pension contributions are automatic deductions if you're enrolled in a workplace pension. Under auto-enrolment rules, the minimum contribution is 8% of qualifying earnings, with at least 3% from your employer. These deductions help you save for retirement directly from your salary.

Other deductions

You might have additional deductions depending on your circumstances:

- Student loan repayments: Deducted automatically once you earn above the threshold for your plan type

- Trade union fees: Regular payments if you're a union member

- Payroll giving: Charitable donations made before tax is calculated

- Salary sacrifice schemes: Contributions to benefits like cycle-to-work or additional pension

Calculating gross and net pay in the UK

Calculate both gross and net pay with these step-by-step examples.

How to calculate gross pay

Calculating gross pay helps you forecast payroll costs accurately and avoid cash flow surprises. The method depends on whether your employee is salaried or paid hourly.

For salaried employees: Annual salary ÷ Number of pay periods = Gross pay per period

For hourly employees: Hourly rate × Hours worked = Base gross pay

To calculate gross pay for a salaried employee:

- Divide the annual salary by 12 for monthly pay (£30,000 ÷ 12 = £2,500)

- Add any extras like commission, bonuses, or overtime

- Calculate the total gross pay (£2,500 + £100 bonus = £2,600)

For hourly employees, multiply their hourly rate by hours worked.

Example: An employee on the London Living Wage of £13.85 works an eight-hour shift. Their base gross pay is £110.80.

Next, add any additional earnings like overtime and bonuses:

- Base pay: £110.80

- Bonus: £50

- Overtime: £27.70 (two hours at £13.85)

- Total gross pay: £188.50

How to calculate net pay from gross

Calculating net pay shows you what an employee actually takes home. Subtract all deductions from gross pay to find the final figure.

Net pay = Gross pay − All deductions

UK example (2024/25 tax year):

- Gross pay: £30,000

- Income tax: −£3,486 (calculated at the 20% basic rate on income above the personal allowance)

- National Insurance: −£1,394 (based on the 8% Class 1 National Insurance rate)

- Net pay: £25,120 (approximately)

Additional deductions like pension contributions, student loans, or salary sacrifice schemes will reduce net pay further.

If you don't have the resources in-house to take care of payroll, work with a payroll professional. Or use payroll software to automate these calculations, streamlining the payroll process.

Gross pay vs net pay: Where each matters

Understanding when to use each figure helps you make better financial decisions.

Use gross pay for:

- writing employment contracts and job offers

- negotiating salaries and pay rises

- calculating pension contributions

Use net pay for:

- creating personal budgets

- applying for mortgages

- planning monthly expenses

For employers: Budget for gross salary plus employer costs like NI contributions and pension matching.

For employees: Base all financial decisions on net pay, as this reflects your actual spending power.

Example calculation:

- Gross pay: £30,000

- Deductions: £4,880 (income tax + National Insurance, approximately)

- Net pay: £25,120 (approximately)

This shows how £30k gross becomes approximately £25k net, a difference of nearly £5,000 that affects your actual spending power.

Use HMRC's income tax calculator to estimate net pay from gross pay. You need to know your gross income, as it determines your tax bracket and pension contributions. For example, the personal allowance is reduced for incomes over £100,000, and no personal allowance applies if income reaches £125,140 or more.

When hiring or offering pay rises, always state the gross salary in written offers. On payslips, show gross pay, each deduction, and net pay clearly. This transparency helps employees understand exactly what they receive and why.

Getting gross and net pay right for your business

Accurate payroll keeps you compliant with HMRC and builds employee trust. Getting it right means avoiding penalties and keeping staff satisfied.

Payroll software saves time and improves accuracy compared to manual calculations. You can focus on running your business instead of managing your books.

How Xero simplifies gross and net pay calculations

Xero's payroll software automates gross and net pay calculations, reducing errors and saving time on every pay run.

Key benefits include:

- Automatic calculations: Tax, National Insurance, and pension deductions done correctly every time

- Generating payslips: Clear breakdown showing gross pay, deductions, and net pay

- Handling compliance: Auto-enrolment and Real Time Information (RTI) submissions to HMRC

- Enabling self-service: Staff access their payslips and P60s online

Get one month free and see how Xero simplifies your finances.

FAQs on gross pay vs net pay

Below you'll find answers to common questions about gross and net pay.

Which is higher, gross pay or net pay?

Gross pay is always higher than or equal to net pay. Gross pay represents your full earnings before deductions. Net pay is what remains after tax, National Insurance, and other deductions are subtracted.

Is it better to negotiate gross or net salary?

Negotiate gross salary, as this is the standard figure used in contracts and pay reviews. Your net pay can change if tax rates or personal circumstances shift, but your agreed gross salary stays fixed.

Why is my take-home pay less than the advertised salary?

Advertised salaries show gross pay, which differs from your take-home amount. Your take-home pay reflects the amount remaining after income tax, National Insurance, and pension contributions are subtracted. For example, a £30,000 gross salary typically becomes around £25,000 net.

Do all employees pay the same deductions from gross pay?

Deductions vary by individual. For example, income tax rates differ based on location; for the 2024-2025 tax year, Scotland has six PAYE tax bands, while the rest of the UK has three. While most employees pay income tax and National Insurance, the amounts differ based on:

- your earnings level

- your tax code

- student loan repayment obligations

- pension contribution rates

Two employees with the same gross salary can have different net pay depending on their personal circumstances.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Get one month free

Purchase any Xero plan, and we will give you the first month free.