Working capital: formula, ratio and how to manage it

Working capital helps you manage cash flow and cover costs. Learn how to calculate it and keep it healthy.

Written by Lena Hanna—Trusted CPA Guidance on Accounting and Tax. Read Lena's full bio

Published Tuesday 21 April 2026

Table of contents

Key takeaways

- Calculate your working capital by subtracting your current liabilities from your current assets — the result shows how much financial cushion you have to cover day-to-day costs and unexpected expenses.

- Aim for a working capital ratio between 1.2 and 2.0, as a ratio below 1.0 can signal cash flow problems, while a ratio well above 2.0 may mean you're not putting your assets to work effectively.

- Recognise that positive working capital doesn't guarantee you'll always have cash on hand — if your money is tied up in unpaid invoices or unsold stock, you can still struggle to meet short-term payments.

- Improve your working capital by speeding up customer payments, managing stock levels carefully, and negotiating longer payment terms with suppliers to keep more cash available for daily operations.

Components of working capital

Components of working capital are the building blocks used to calculate your financial cushion. There are two main elements: current assets (what you own) and current liabilities (what you owe). Understanding both helps you see the full picture of your short-term financial health.

Current assets

Current assets are resources your business owns that can convert into cash within one year. They fund your day-to-day operations and include:

- cash and cash equivalents: money in bank accounts and liquid holdings

- accounts receivable: money customers owe you for goods or services

- inventory: stock you hold for sale

- short-term investments: assets you can sell quickly if needed

Current liabilities

Current liabilities are debts or obligations your business must pay within one year. Managing them is crucial for maintaining healthy cash flow. Current liabilities include:

- accounts payable: money you owe to suppliers

- short-term loans: borrowings due within 12 months

- accrued expenses: wages, taxes, and other costs you've incurred but not yet paid

- deferred revenue: payments received for goods or services you haven't yet delivered

The importance of working capital in business

Working capital is one indicator of short-term liquidity and your business's ability to cover short-term expenses. It matters because it helps you:

- survive seasonal fluctuations: maintain operations during slow periods

- fund growth opportunities: invest in new stock, equipment, or staff

- attract lenders: demonstrate financial stability when applying for finance

Positive versus negative working capital

Your working capital position falls into one of four categories:

- positive working capital: your assets exceed liabilities, allowing you to pay bills and reinvest in growth

- negative working capital: your liabilities exceed assets, signalling potential cash flow problems that may require borrowing

- neutral working capital: your assets and liabilities are roughly equal, leaving little buffer for unexpected expenses

- very high working capital: your assets significantly exceed liabilities, suggesting you could invest more in growth opportunities

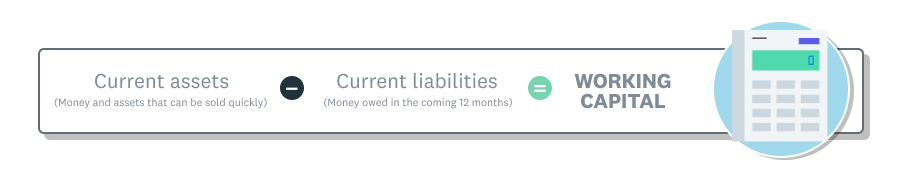

How to calculate working capital

Calculate working capital by subtracting current liabilities from current assets. The result shows how much money you have available to run your business.

Accounting software like Xero makes this simple by automatically pulling data from your balance sheets and financial reports.

The working capital formula

A working capital formula example

Here's how a retail florist calculates their working capital:

- Add up current assets: cash, receivables, and inventory total £100,000.

- Add up current liabilities: payables, loans, and accrued expenses total £75,000.

- Subtract liabilities from assets: £100,000 − £75,000 = £25,000.

The florist has £25,000 in working capital to fund daily operations.

Working capital versus working capital ratio

Working capital tells you the pound amount available after covering short-term debts. The working capital ratio (also called the current ratio) shows the relationship between assets and liabilities as a number.

For example, a ratio of 1.5 means you have £1.50 in assets for every £1 you owe. Learn more about the working capital ratio.

Working capital examples in different businesses

Working capital needs vary by industry because operating cycles, cash flow patterns, and asset structures differ across sectors. A construction firm needs more working capital than a consultancy, for example. Understanding your industry's typical requirements helps you set realistic targets for your business.

Working capital in construction and manufacturing

Construction and manufacturing businesses face irregular cash flow, long project timelines, and delayed payments. These factors create a gap between spending money and receiving payment.

Working capital bridges this gap by funding upfront costs for materials, subcontractors, and labour. Businesses in these sectors often require significant working capital investment in inventory and trade receivables.

Working capital in service businesses

Service businesses typically need less working capital because they don't hold inventory. However, they face different pressures: higher accounts receivable from client invoicing and ongoing costs for payroll, office expenses, and project delivery. Cash tied up in unpaid invoices can still strain liquidity.

Working capital in retail

Retail businesses typically need substantial working capital to fund inventory. Stock sits on shelves until it sells, tying up cash that could be used elsewhere.

Some large retailers operate with a current ratio below 1 because they sell goods and collect cash before paying suppliers. Smaller retailers must carefully balance stock levels with sales to maintain healthy working capital.

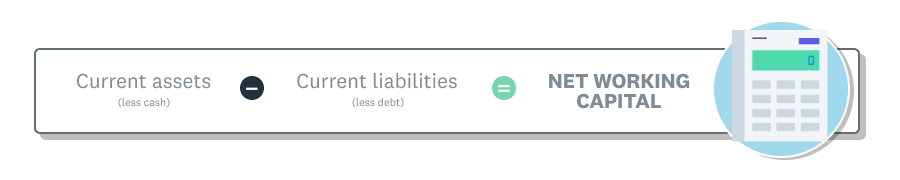

What is net working capital?

Net working capital (also called operating working capital) excludes cash and debt from the standard calculation. This focuses the measure specifically on operational efficiency rather than overall liquidity.

Use net working capital when you want to assess how efficiently your business converts inventory and receivables into cash. It's especially useful for:

- longer-term financial planning: tracking operational performance over time

- growing businesses: measuring efficiency as you scale

- low-margin industries: retail, manufacturing, and distribution where profitability depends on operational efficiency

The operating working capital formula

Let's look again at the florist. Suppose their current assets include a cash amount of £20,000, and their current liabilities include short-term interest-bearing debts of £10,000. The formula for their operating working capital is £80,000 (£100,000 – £20,000) – £65,000 (£75,000 – £10,000) = £15,000.

Working capital versus cash flow: what's the difference?

Working capital and cash flow measure different aspects of your finances:

- working capital: measures your ability to cover short-term debts and shows your financial cushion over 12 months

- cash flow: tracks money moving in and out and shows your actual cash position at any given time

You can have positive working capital but still face cash flow problems if payments arrive at the wrong time.

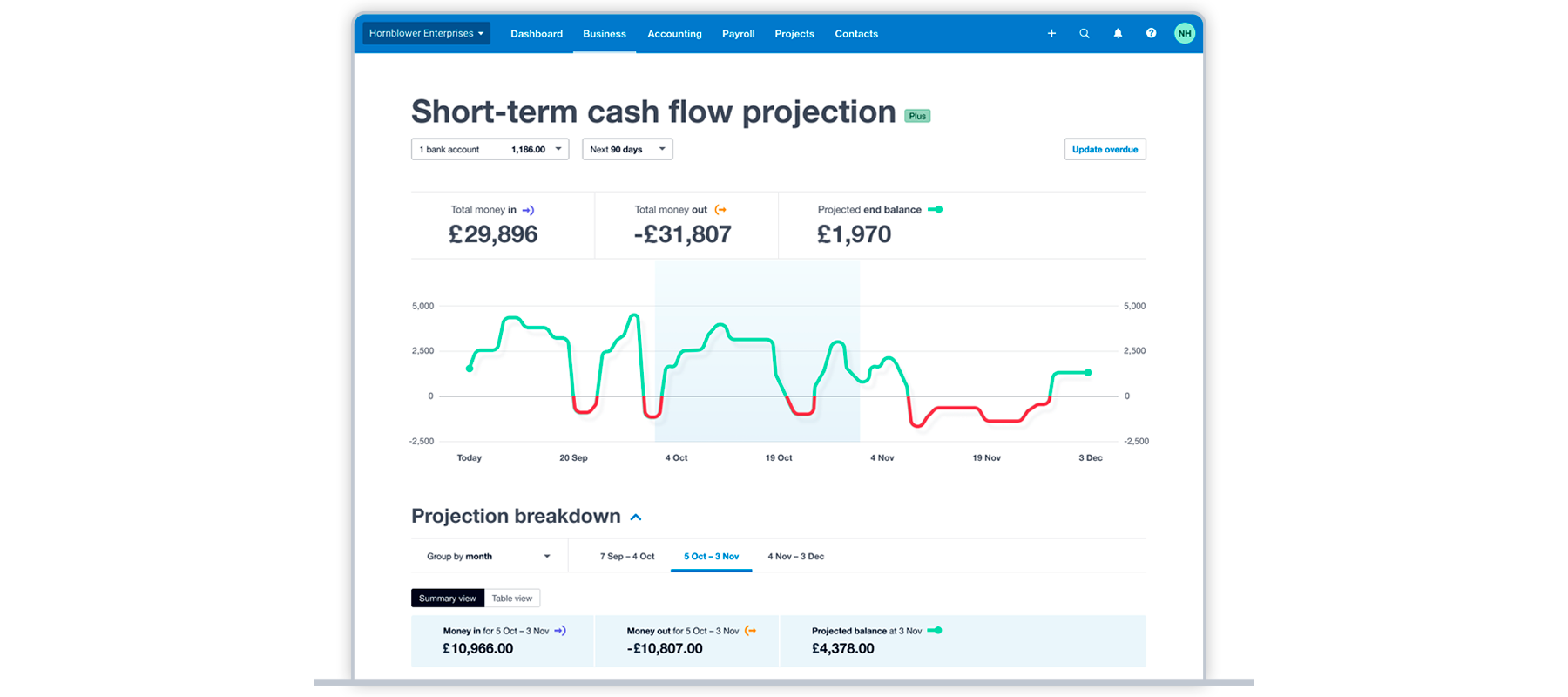

Here's an example from Xero's short-term cash flow projection. It shows the total money in and out for the next 90 days. It doesn't include liquid assets or show the whole picture of the business's health and adaptability.

How to manage your working capital

Managing working capital effectively improves your cash flow, reduces financial stress, and frees up money for growth. The following strategies help you optimise each component of your working capital.

Manage your inventory

These strategies help you keep inventory at optimal levels:

- Optimise stock levels: keep inventory balanced so you're not tying up cash in unsold goods or running short when demand changes

- Speed up turnover: offer promotions or discounts on slow-moving stock to free up cash faster

- Automate tracking: use inventory management software to monitor stock in real time and forecast demand. Check out Xero's inventory management guide and learn about Xero's inventory features

Control your expenses

Keep costs under control with these approaches:

- Review spending regularly: identify where you can reduce costs without affecting quality or operations

- Cut non-essential expenses: focus spending on activities that directly support business growth

FAQs on working capital

Here are answers to common questions about working capital and how to manage it effectively.

What's a good working capital ratio?

A working capital ratio between 1.2 and 2.0 is generally healthy for most businesses. This means you have £1.20 to £2.00 in current assets for every £1.00 in current liabilities. A ratio below 1.0 may indicate liquidity problems, while a ratio significantly above 2.0 might suggest you're not using your assets efficiently.

How can I improve my working capital?

You can improve working capital by accelerating cash inflows and delaying cash outflows where appropriate. Speed up customer payments by offering early payment discounts, send invoices promptly, and follow up on overdue accounts. Manage inventory levels carefully to avoid tying up excess cash in stock. Negotiate better payment terms with suppliers to extend your payment periods without damaging relationships.

What's the difference between working capital and cash?

Cash is the actual money you have in bank accounts and on hand. Working capital is a broader measure that includes all current assets (cash, receivables, inventory) minus all current liabilities (payables, short-term loans). You can have positive working capital but still run short of cash if your assets are tied up in inventory or unpaid invoices.

Can a business have negative working capital and still be successful?

Yes, some businesses operate successfully with negative working capital. Large retailers often collect cash from customers before paying suppliers, creating negative working capital. However, this model requires consistent sales and strong cash flow management. For most small businesses, negative working capital signals potential financial stress and difficulty meeting short-term obligations.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Get one month free

Purchase any Xero plan, and we will give you the first month free.