What is a basis of accounting?

Learn how your basis of accounting affects when you record income and expenses.

Published Thursday 23 July 2026

Table of contents

Key takeaways

Basis of accounting determines the point at which you recognise transactions.

- A basis of accounting determines when you record income and expenses, and it directly affects your tax return, cash flow picture, and financial reporting.

- Cash basis accounting records transactions when money changes hands, while accrual basis records them when they're earned or owed, regardless of payment timing.

- Since April 2024, cash basis is the default method for sole traders and partnerships in the UK, with no turnover threshold to qualify.

- Choosing the right method depends on your business size, growth plans, and whether you need detailed financial reports for lenders or investors.

What is a basis of accounting?

A basis of accounting is the set of rules that decides when you record income and expenses in your books. It's the foundation of how your financial records are put together.

There are 2 main methods used in the UK: cash basis and accrual basis. Each one treats the timing of transactions differently, which affects your taxable profits, financial statements, and how clearly you can see your business's financial health.

The method you use shapes everything from your Self Assessment tax return to the reports you share with your accountant. Understanding the difference helps you pick the approach that suits your business.

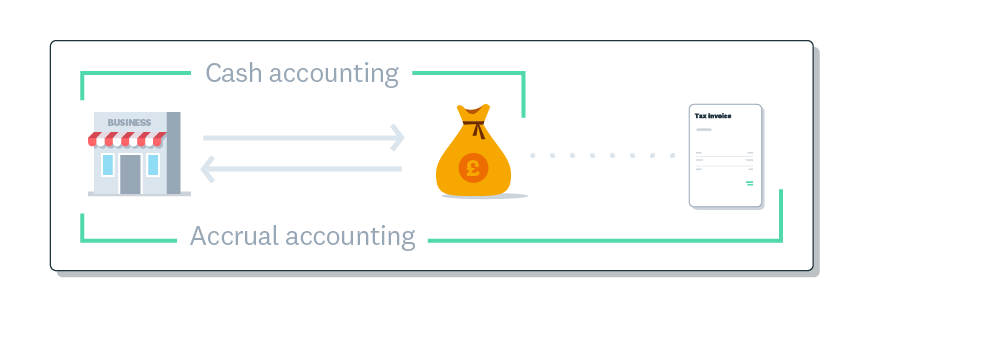

What is cash basis accounting?

Cash basis accounting records income when you actually receive payment, and expenses when you actually pay them. It's the simpler of the 2 methods and focuses on real money in and out of your bank account.

Since April 2024, cash basis is the default accounting method for sole traders and partnerships reporting to HMRC. If you're self-employed and don't opt out, you'll use this method automatically.

Here's a practical example. Say you invoice a client £2,000 in March but they don't pay until May. Under cash basis, you'd record that £2,000 as income in May, when the money actually hits your account. If you buy £300 of supplies in March and pay for them straight away, that expense is recorded in March.

This makes bookkeeping straightforward because your records closely match your bank statements. You only pay tax on money you've genuinely received, which can help with cash flow if your clients are slow to pay.

What is accrual basis accounting?

Accrual basis accounting records income when it's earned and expenses when they're incurred, regardless of when the money moves. It gives a more complete picture of your financial commitments at any point in time.

Using the same example: if you invoice a client £2,000 in March, you'd record that income in March, even if the client doesn't pay until May. The £300 supplies purchase would also be recorded when the goods are delivered or the service is provided, not necessarily when you pay for them.

This method is required for limited companies and limited liability partnerships (LLPs) in the UK. It's also the standard used in formal financial reporting, so lenders, investors, and partners generally expect to see accrual-based accounts.

While it takes more effort to maintain, accrual accounting shows you a truer view of profitability. You can see what you're owed and what you owe, not just what's cleared through the bank.

Cash basis vs accrual basis: key differences

The core distinction between these 2 methods comes down to timing. For a deeper look, read the full cash vs accrual accounting guide. Here's how they compare across the areas that matter most to your business.

- When income is recorded: Cash basis records it when payment is received. Accrual basis records it when it's earned (for example, when you send an invoice).

- When expenses are recorded: Cash basis records them when you pay. Accrual basis records them when you receive the goods or services.

- Tax timing: With cash basis, you're taxed on money you've actually received. With accrual, you may owe tax on income you haven't collected yet.

- Financial accuracy: Accrual gives a fuller picture of your financial position, including money owed to you and debts you haven't yet paid. Cash basis reflects only completed transactions.

- Complexity: Cash basis is simpler to manage day to day. Accrual requires tracking receivables and payables, which adds bookkeeping work.

- Who it suits: Cash basis works well for smaller, straightforward businesses. Accrual is better for growing businesses or those needing detailed financial reports.

Who can use cash basis accounting in the UK?

Cash basis is available to sole traders and ordinary partnerships. Since the 2024/25 tax year, HMRC has removed the turnover thresholds that previously restricted eligibility, so there's no longer a cap on how much you can earn and still use cash basis.

Before this change, you needed a turnover of £150,000 or less to join cash basis, and had to leave if your turnover exceeded £300,000. Those limits no longer apply. Additionally, the £500 cap on interest deductions under cash basis has been removed from 2024/25 onwards, and loss relief rules now align with accrual accounting.

Some businesses can't use cash basis, including:

- Limited companies

- Limited liability partnerships (LLPs)

- Lloyd's underwriters

- Businesses with farming or creative works averaging elections

If you're a sole trader or partner and none of these exclusions apply, you'll use cash basis by default unless you actively opt out on your tax return.

How to choose the right accounting method

Your ideal accounting method depends on your business circumstances now and where you're heading. There's no universally correct answer, but a few factors can guide your decision.

Business size and complexity: If you run a small, straightforward business with few outstanding invoices, cash basis keeps things simple. For a broader overview, see the small business accounting guide. If you carry significant stock, manage multiple revenue streams, or regularly have large amounts of unpaid invoices, accrual gives you better visibility.

Growth and funding plans: Planning to apply for a business loan or bring in investors? They'll typically want accrual-based accounts because these show a more complete financial picture. Switching to accrual before you need it avoids a disruptive changeover later.

Making Tax Digital (MTD): MTD for VAT already requires quarterly digital submissions, and MTD for Income Tax Self Assessment is being introduced from April 2026. Both methods are supported under MTD, so your accounting basis won't prevent compliance. However, if you're already using software for MTD, the switch between methods is simpler than doing it manually.

Record-keeping preference: Cash basis means fewer adjustments at year end because you're matching records to bank transactions. Accrual requires you to track what's owed and owing, which can be more work but also more informative.

How accounting software simplifies your bookkeeping

Whichever method you choose, accounting software takes the manual effort out of recording and reconciling transactions. Instead of tracking everything in spreadsheets, you can automate most of the routine work.

Xero supports both cash basis and accrual basis reporting, so you can switch between views without re-entering data. This is especially useful if you use cash basis for your tax return but want an accrual view to understand your true financial position.

Bank feeds pull transactions directly into Xero, and automated reconciliation matches them to your invoices and bills. Hubdoc captures receipts and bills automatically, which can help reduce the chance of missing a deductible expense.

For MTD compliance, Xero handles digital record-keeping and quarterly submissions. It keeps your records in the format HMRC expects, whichever accounting method you're using. And if your business grows and you need to switch from cash basis to accrual, your historical data is already in the system.

Manage your accounts with confidence using Xero

Choosing your basis of accounting is one of the first financial decisions you'll make for your business. Getting it right means clearer tax returns, better cash flow visibility, and fewer surprises at year end.

Xero gives you the tools to manage your finances on either method, with automated bank reconciliation, invoicing, expense tracking, and MTD-ready reporting built in. Whether you're a sole trader on cash basis or a growing business using accrual, you can help stay on top of your books with less manual hassle. Get one month free.

FAQs on basis of accounting

Here are answers to some common questions about accounting methods in the UK.

Can you switch from cash basis to accrual basis?

Yes. You can switch by selecting accrual accounting on your next Self Assessment tax return. You'll need to make transitional adjustments to account for any income or expenses that would otherwise be counted twice or missed.

Do I need to use accrual accounting for Making Tax Digital?

No. MTD for VAT and the upcoming MTD for Income Tax both support cash basis and accrual basis. Your choice of accounting method doesn't affect your ability to comply with MTD requirements.

Is cash basis the same as cash accounting for VAT?

They're related but separate. Cash basis for income tax records your profits based on when you receive and make payments. VAT cash accounting is a separate HMRC scheme that lets you account for VAT on the date of payment rather than the invoice date.

What happens if I use the wrong accounting method?

If you're a limited company using cash basis, HMRC could challenge your accounts. Sole traders and partnerships are on cash basis by default from 2024/25, so you'd only be "wrong" if you're using a method you're not eligible for, such as a limited company trying to use cash basis.

Does my accountant decide which basis of accounting I use?

Your accountant can advise you, but the decision is yours. They'll help you weigh up factors like business complexity, growth plans, and reporting needs to recommend the method that fits best. You can find an accountant or bookkeeper through the Xero advisor directory.

Handy resources

Advisor directory

You can search for experts in our advisor directory

How to do bookkeeping

Learn about data entry, bank rec, reporting and tax prep in our guide to doing bookkeeping.

Online accounting with Xero

Automate your accounting in the cloud

Disclaimer

This glossary is for small business owners. The definitions are written with their requirements in mind. More detailed definitions can be found in accounting textbooks or from an accounting professional. Xero does not provide accounting, tax, business or legal advice.