Straight-line depreciation explained

Learn straight-line depreciation: the formula, worked examples, and how to record it in your books.

Written by Jotika Teli—Certified Public Accountant with 24 years of experience. Read Jotika's full bio

Published Friday 15 May 2026

Table of contents

Key takeaways

- Straight-line depreciation spreads the cost of an asset evenly over its useful life, making it the simplest method to calculate and apply

- The formula is (Cost - Salvage Value) / Useful Life, giving you the same expense amount each year

- This method works best for assets that lose value steadily over time, like office furniture, buildings, and rental property

- Understanding depreciation helps you make smarter tax decisions, including whether to use Section 179 expensing or bonus depreciation for faster write-offs

Every physical asset your business owns loses value over time. Depreciation is the accounting method you use to reflect that loss of value on your financial records. Among the different approaches available, straight-line depreciation is the most commonly used, and it's the easiest to understand.

What is straight-line depreciation?

Straight-line depreciation is a method that spreads the cost of a tangible asset evenly across each year of its useful life. You subtract the asset's salvage value (what it's worth at the end of its life) from its original cost to get the depreciable base. Then you divide that depreciable base by the number of years you expect to use the asset.

Businesses use depreciation because accounting standards don't allow you to expense the full cost of a long-term asset in the year you buy it. Instead, you recognize a portion of the cost each year, matching the expense to the revenue the asset helps generate. This gives you a more accurate picture of your profitability over time.

Straight-line depreciation is popular because the calculation is simple and produces a consistent expense each period. If you're a small business owner looking for a predictable way to account for wear and tear on your equipment, vehicles, or property, this is often the right starting point.

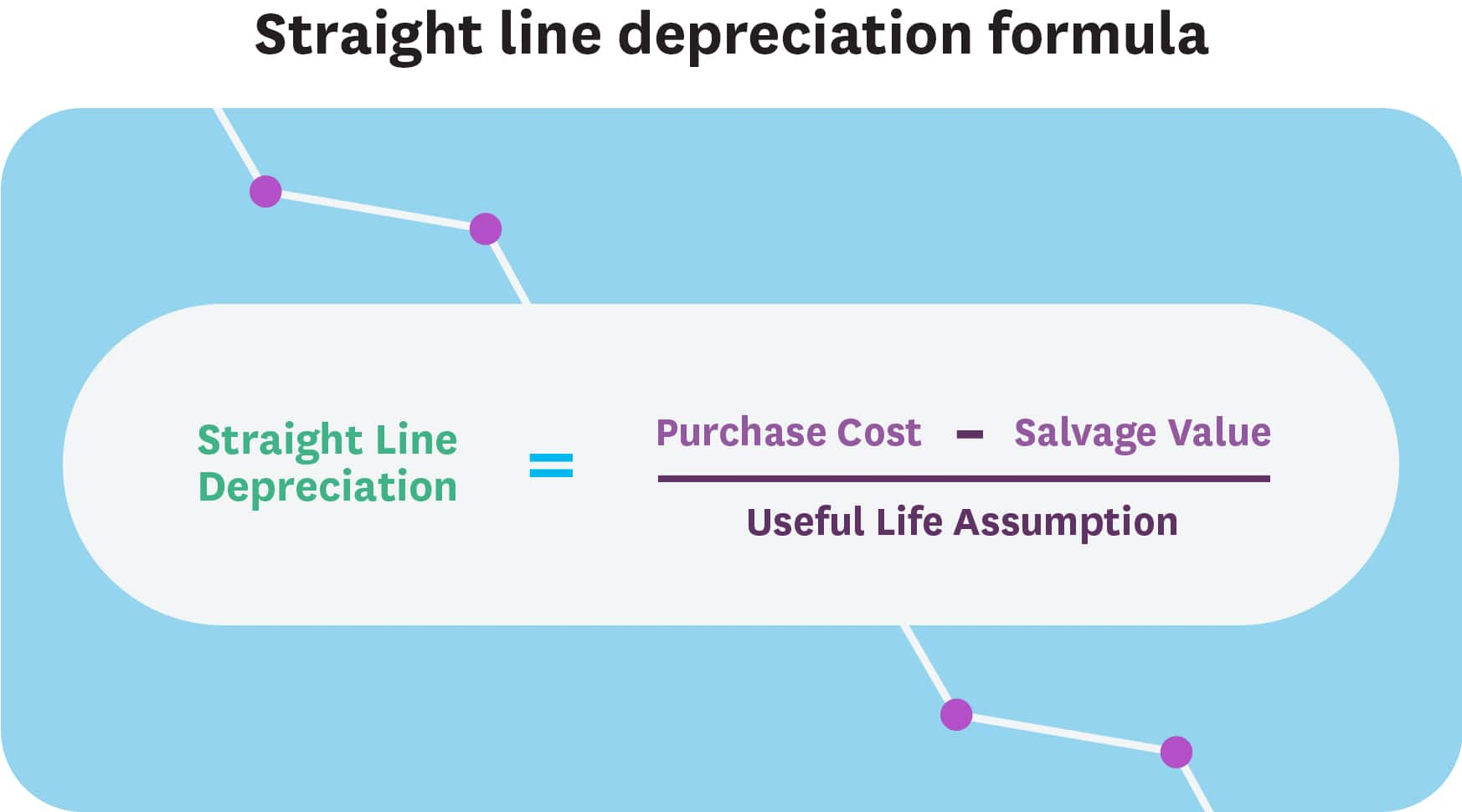

Straight-line depreciation formula

The formula for calculating straight-line depreciation is simple. Here's how it works:

Annual Depreciation Expense = (Cost - Salvage Value) / Useful Life

Each component plays a specific role in the calculation:

- Cost: the total amount you paid to acquire and put the asset into service, including purchase price, shipping, and installation

- Salvage value: the estimated amount the asset will be worth when you're done using it, sometimes called residual value

- Useful life: the number of years you expect to use the asset in your business before retiring or replacing it

The difference between cost and salvage value is known as the depreciable base. That's the total amount you'll expense over the asset's useful life.

How to calculate straight-line depreciation

Now that you know the formula, here's how to apply it step by step. Follow these three steps for any asset:

- Determine the asset's original cost, including purchase price and any setup costs

- Estimate the salvage value at the end of the asset's useful life

- Divide the depreciable base (cost minus salvage value) by the useful life in years

Let's work through several examples to see how this looks in practice.

Example 1: Plant machinery

Suppose you buy a piece of manufacturing equipment for $22,000. You estimate it will last 10 years and have a salvage value of $2,000.

- Depreciable base: $22,000 - $2,000 = $20,000

- Annual depreciation: $20,000 / 10 = $2,000 per year

You'd record $2,000 in depreciation expense each year for 10 years.

Example 2: Office computer

You purchase a computer for your office at a cost of $1,200. You expect to use it for five years, and it will have a salvage value of $200.

- Depreciable base: $1,200 - $200 = $1,000

- Annual depreciation: $1,000 / 5 = $200 per year

Example 3: Delivery vehicle

Your business buys a delivery van for $35,000. You plan to use it for seven years and estimate a salvage value of $7,000.

- Depreciable base: $35,000 - $7,000 = $28,000

- Annual depreciation: $28,000 / 7 = $4,000 per year

Here's what the year-by-year depreciation schedule looks like for the delivery vehicle:

- Year 1: $4,000 depreciation expense, accumulated depreciation $4,000, book value $31,000

- Year 2: $4,000 depreciation expense, accumulated depreciation $8,000, book value $27,000

- Year 3: $4,000 depreciation expense, accumulated depreciation $12,000, book value $23,000

- Year 4: $4,000 depreciation expense, accumulated depreciation $16,000, book value $19,000

- Year 5: $4,000 depreciation expense, accumulated depreciation $20,000, book value $15,000

- Year 6: $4,000 depreciation expense, accumulated depreciation $24,000, book value $11,000

- Year 7: $4,000 depreciation expense, accumulated depreciation $28,000, book value $7,000 (salvage value)

Mid-year convention

In some cases, you may not place an asset in service on the first day of your fiscal year. The mid-year convention assumes that all assets are placed in service at the midpoint of the year, regardless of the actual purchase date. This means you claim half a year's depreciation in the first year and half in the final year.

For the delivery vehicle example above, a mid-year convention would give you $2,000 of depreciation in year one and $2,000 in year eight, with $4,000 in each year between. The IRS requires the mid-year convention for most assets under MACRS unless a different convention applies.

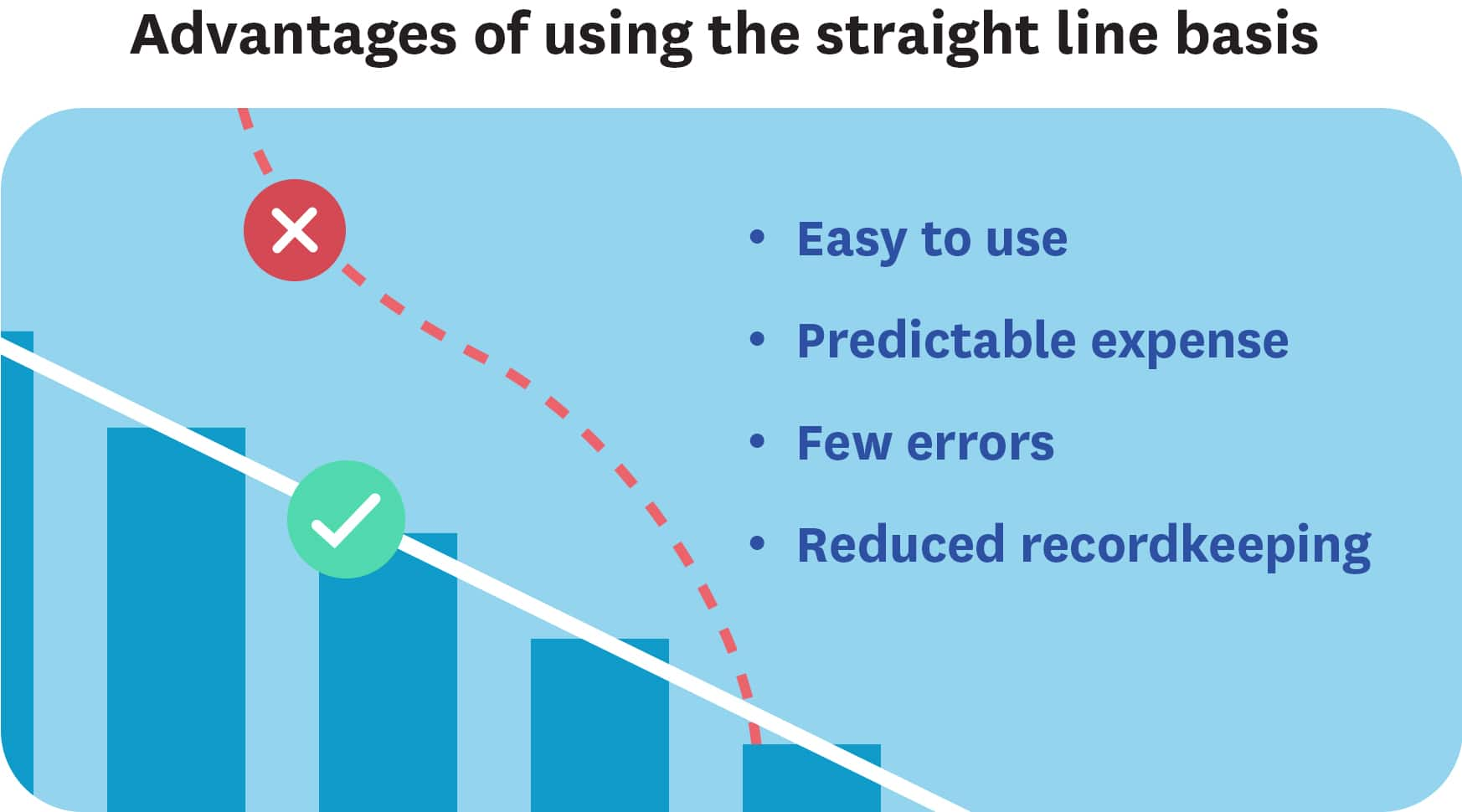

Pros and cons of the straight-line method

Like any accounting method, straight-line depreciation has clear advantages and some limitations. Here's what to consider when deciding if it's right for your business.

Pros

- Simple to calculate and easy to understand, even without an accounting background

- Produces a consistent, predictable expense each period, which helps with budgeting and forecasting

- Widely accepted for financial reporting under GAAP (Generally Accepted Accounting Principles)

- Works well for assets that wear out evenly over time

Cons

- Doesn't reflect the actual usage pattern of assets that lose value faster in early years, like technology or vehicles

- May not match revenue generation if an asset produces more revenue early in its life

- Not accepted for tax purposes in most cases; the IRS typically requires MACRS for tax depreciation

- Doesn't account for unexpected changes in an asset's useful life or value

Other depreciation methods

Straight-line isn't the only way to depreciate your assets. Depending on how an asset is used and your tax situation, a different method may be more appropriate. Here are the main alternatives.

Units of production

This method ties depreciation to actual usage rather than time. You calculate a per-unit rate by dividing the depreciable base by the total estimated units the asset will produce. This works well for manufacturing equipment or vehicles where wear and tear depends on how much you use them, not just how long you own them.

Declining balance

The declining balance method applies a fixed depreciation rate to the asset's remaining book value each year. Because the book value shrinks over time, your depreciation expense is highest in the first year and decreases after that. This better reflects assets that lose the most value early in their life.

Double-declining balance

This is an accelerated version of the declining balance method. You take twice the straight-line rate and apply it to the remaining book value each year. It's useful when you want to front-load your depreciation expense, which is common for technology assets and equipment that becomes obsolete quickly.

Sum-of-the-years'-digits

Another accelerated method, sum-of-the-years'-digits assigns a fraction to each year based on the remaining life of the asset. For an asset with a five-year life, the fractions would be 5/15, 4/15, 3/15, 2/15, and 1/15. Like declining balance, this front-loads the expense to reflect faster early depreciation.

MACRS (Modified Accelerated Cost Recovery System)

MACRS is the depreciation system the IRS requires for most business assets for tax purposes. It uses predetermined recovery periods and accelerated methods to calculate your deduction. MACRS assigns specific recovery periods to different asset types:

- Computers and peripherals: 5 years

- Light trucks and vehicles: 5 years

- Office furniture: 7 years

- Residential rental property: 27.5 years

- Nonresidential real property: 39 years

You'll find a complete list of recovery periods in IRS Publication 946.

MACRS also has an alternative system called ADS (Alternative Depreciation System). ADS generally uses longer recovery periods and the straight-line method. It's required for certain types of property, including assets used predominantly outside the US and tax-exempt property.

Keep in mind that MACRS is for tax depreciation only. For your internal books and financial statements, you can still use straight-line or any other method that best reflects how the asset loses value.

Depreciation impact on financial statements and taxes

Depreciation affects more than just one line on your books. It touches three major financial statements and plays a significant role in your tax planning. Here's how.

Income statement

Depreciation appears as an operating expense on your income statement. It reduces your reported net income for the period, even though you didn't make a cash payment. This non-cash expense lowers your taxable income, which is one reason depreciation matters for tax purposes.

Balance sheet

On your balance sheet, accumulated depreciation is subtracted from the asset's original cost to show its net book value. As depreciation builds up over time, the net book value of your assets decreases. This gives you and anyone reviewing your financials a more realistic picture of what your assets are currently worth.

Cash flow statement

Because depreciation is a non-cash expense, it gets added back to net income in the operating activities section of your cash flow statement. This means depreciation reduces your taxable income without reducing your actual cash on hand, which can improve your cash flow position.

Section 179 expensing

Instead of depreciating an asset over several years, Section 179 lets you deduct the full purchase price in the year you buy it. For 2026, the maximum Section 179 deduction is $2,560,000. This benefit begins to phase out when your total equipment purchases exceed $4,090,000 in a single year. It's a popular choice for small businesses that want an immediate tax benefit on qualifying purchases like equipment, vehicles, and software.

Bonus depreciation

Bonus depreciation is a federal tax incentive that lets you deduct a percentage of an asset's cost in the first year you place it in service. The One Big Beautiful Bill Act restored 100% bonus depreciation for qualifying property placed in service after January 19, 2025. This means for 2026, you can deduct the full cost of eligible assets in year one. You can use bonus depreciation alongside regular MACRS depreciation if you choose a reduced rate.

Book vs. tax depreciation

Your financial statements (book depreciation) and your tax return (tax depreciation) often use different methods and timelines. For books, you might use straight-line over 10 years. For taxes, the IRS may require MACRS over five years. This creates temporary differences between your reported income and your taxable income. Tracking both is important for accurate financial reporting and tax compliance.

When to use straight-line depreciation

Choosing the right depreciation method depends on the type of asset and how your business uses it. Straight-line depreciation works best when an asset loses value at a steady, predictable rate over its lifetime.

Assets suited for straight-line depreciation

Some assets naturally fit the straight-line approach because their value decreases consistently from year to year:

- Office furniture and fixtures

- Buildings and structural improvements

- Residential and commercial rental property

- Leasehold improvements

- General office equipment like printers and phone systems

Assets better served by accelerated methods

Other assets lose most of their value in the first few years. For these, an accelerated method like double-declining balance or MACRS may give you a more accurate picture and a larger tax deduction early on:

- Computers and technology hardware

- Vehicles, especially those with high mileage

- Specialized manufacturing equipment

- Software with a short expected lifespan

If you're unsure which method fits your situation, talk with your accountant. They can help you choose the approach that balances accurate financial reporting with the best tax outcome for your business.

Recording straight-line depreciation in your accounting system

Once you've calculated your annual depreciation, you need to record it in your books. If you use double-entry bookkeeping, each depreciation entry involves two accounts.

At the end of each period, you record a journal entry with two parts:

- Debit the depreciation expense account for the amount of depreciation calculated

- Credit the accumulated depreciation account for the same amount

The debit increases your expense, which lowers your net income for the period. The credit increases accumulated depreciation, which is a contra-asset account on your balance sheet that reduces the asset's book value over time.

Using the office computer example from earlier ($200 per year), your journal entry each year would look like this:

- Debit: Depreciation Expense $200

- Credit: Accumulated Depreciation $200

Cloud accounting software like Xero can help you set up fixed asset registers and automate these recurring journal entries. This saves you time and helps you avoid manual errors, so your books stay accurate throughout the year.

Track depreciation and manage your assets with Xero

Getting depreciation right keeps your financial statements accurate and your tax filings on track. With Xero's cloud accounting software, you can manage your fixed assets, automate depreciation calculations, and keep your books organized in one place.

FAQs on straight-line depreciation

Here are some frequently asked questions about straight-line depreciation.

What does depreciation mean in accounting?

Depreciation is the process of spreading the cost of a tangible asset over its useful life. Instead of recording the full cost as an expense when you buy it, you recognize a portion each year. This approach matches the expense to the periods in which the asset helps your business generate revenue.

What are the main methods for calculating depreciation?

The most common methods are straight-line, declining balance, double-declining balance, sum-of-the-years'-digits, and units of production. For tax purposes, most US businesses use MACRS, which the IRS requires for depreciating business property. Each method distributes the cost of an asset differently over time.

How does depreciation affect my business's financial statements and taxes?

Depreciation reduces your net income on the income statement and lowers the book value of assets on the balance sheet. Because it's a non-cash expense, it's added back on your cash flow statement. For taxes, depreciation deductions reduce your taxable income, which can lower your tax bill.

What is the difference between straight-line and accelerated depreciation?

Straight-line depreciation spreads the cost evenly across each year of the asset's useful life. Accelerated methods, like double-declining balance, front-load the expense so you record more depreciation in the early years and less later. Accelerated methods are often better for assets that lose value quickly, like technology equipment.

Can you change depreciation methods after you start?

You can change your depreciation method, but it requires careful consideration. For financial reporting, a change is treated as a change in accounting estimate and applied going forward. For tax purposes, switching methods generally requires filing Form 3115 with the IRS. Consult your accountant before making any changes.

What is the depreciable base of an asset?

The depreciable base is the total amount you can depreciate over the life of an asset. You calculate it by subtracting the asset's estimated salvage value from its original cost. For example, an asset that costs $10,000 with a $1,000 salvage value has a depreciable base of $9,000.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Get one month free

Sign up to any Xero plan, and we will give you the first month free.