What is cash flow?

Cash flow is the movement of money in and out of your business, and managing it well is key to staying solvent.

Published Tuesday 14 July 2026

Table of contents

Key takeaways

- Cash flow is the total movement of money into and out of your business over a set period, and it determines whether you can pay bills, staff, and suppliers on time.

- Positive cash flow means more money is coming in than going out; negative cash flow means the opposite, and even profitable businesses can run into trouble if cash flow timing is off.

- Regularly forecasting and monitoring your cash flow helps you spot shortfalls early, plan for quieter months, and make confident decisions about spending and growth.

- Tools like Xero give you real-time visibility over your cash position so you can stay on top of invoices, payments, and your overall financial health.

What is cash flow?

Cash flow is the movement of money into and out of your business over a given period. It shows whether you have enough money coming in to cover what's going out, including payments to suppliers, employees, lenders, and yourself.

You can express cash flow with a simple formula:

Net cash flow = total cash inflows - total cash outflows

When more money flows in than out, you have positive cash flow. When more goes out than comes in, you have negative cash flow. Even a profitable business can experience negative cash flow if the timing of payments doesn't line up; for example, if a large supplier invoice is due before your customers have paid you.

Cash doesn't just mean notes and coins. It also includes "cash equivalents": anything that can be converted to a known amount of money at short notice, usually within about 3 months. Think of short-term investments or deposits that you could access quickly if needed.

Why is cash flow important?

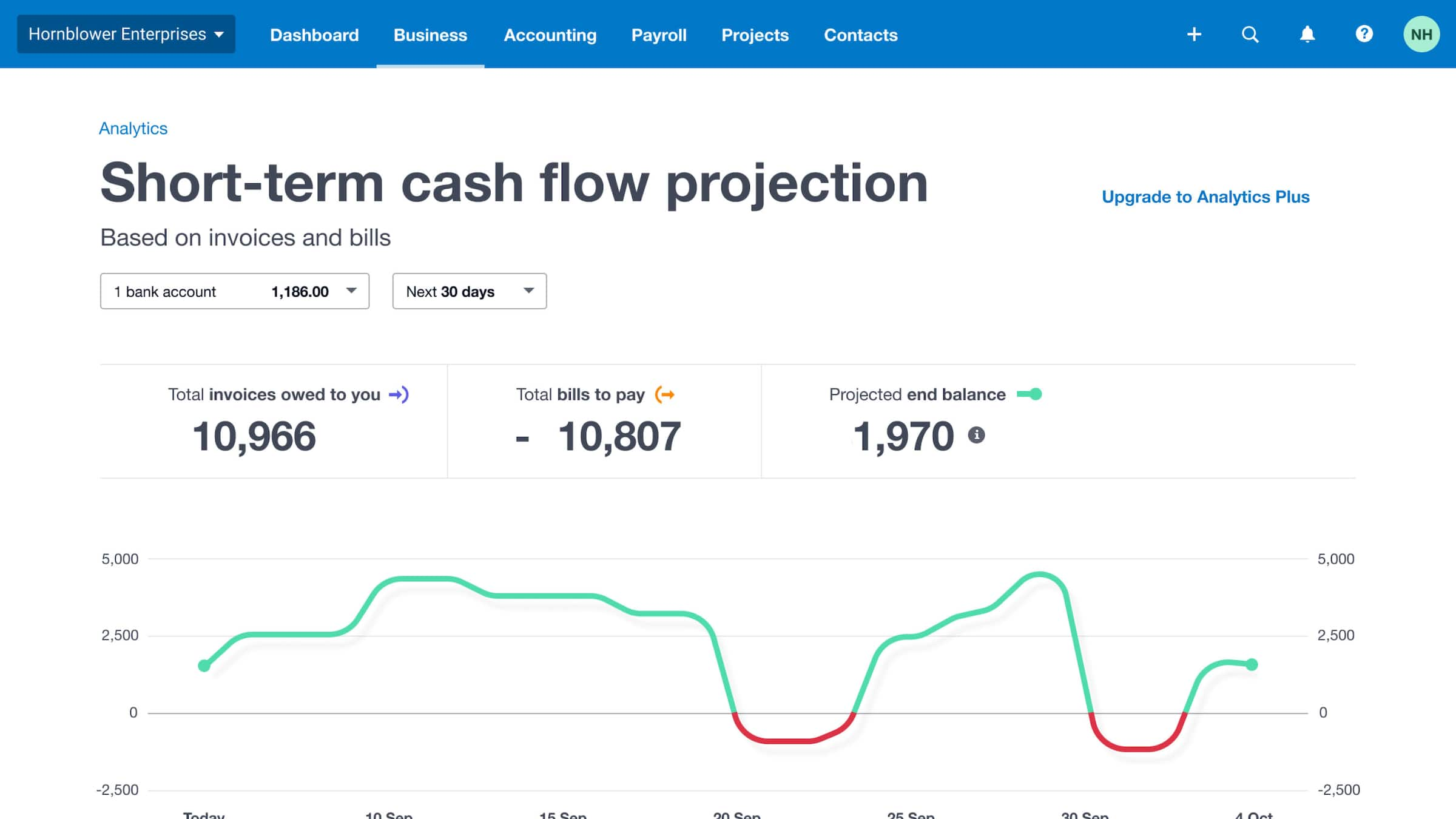

Small businesses can get a picture of future cash flow by accounting for upcoming bills and payments (example from Xero dashboard).

Cash flow is one of the most important measures of your business's financial health. Without enough cash at the right time, you can't pay bills, cover wages, or keep trading, regardless of how profitable your business looks on paper.

According to Xero Small Business Insights, UK small businesses waited an average of 29 days to be paid in the March quarter of 2026, with invoices settled an average of 8.2 days late. These payment delays put real pressure on day-to-day cash flow and make planning harder.

Poor cash flow management can lead to serious problems, from missed payments to stalled growth. You can read more about common cash flow problems and solutions. Here are some of the most common issues:

- Overtrading: taking on more work than your cash reserves can support, leaving you unable to fund delivery costs

- Overspending: committing to expenses before the money to cover them has arrived

- Missed payments: falling behind on supplier invoices, loan repayments, or tax obligations

- Stalled growth: turning down opportunities because you don't have the cash to pursue them

Having spare cash also gives you the flexibility to invest in new opportunities when they arise. Good cash flow visibility reduces financial stress and helps you make confident decisions about your business's future.

Types of cash flow

Cash flow is typically broken down into 3 categories. Understanding each one helps you see where your money is coming from and where it's going.

Cash flow from operations (CFO)

This is the money generated by your core business activities: selling products or services and paying the costs of delivering them. It includes revenue from sales, payments to suppliers, wages, rent, and other day-to-day expenses.

Operational cash flow is the most important type for most small businesses because it shows whether your everyday trading is generating enough money to sustain itself.

Cash flow from investing (CFI)

This covers money spent on or received from longer-term assets. Buying equipment, property, or vehicles counts as a cash outflow here. Selling those assets counts as an inflow.

A negative investing cash flow isn't necessarily bad; it often means you're investing in your business's future capacity.

Cash flow from financing (CFF)

Financing cash flow tracks money moving between your business and its funders. Inflows include bank loans, investor funding, or shareholder contributions. Outflows include loan repayments and dividend payments.

Ideally, your business shouldn't rely too heavily on financing cash flow to stay afloat. Sustainable growth comes from strong operational cash flow.

What affects cash flow

Several factors influence how much cash you have available at any given time. Keeping an eye on these helps you anticipate shortfalls before they become a problem.

Payment timing: the gap between when you pay your costs and when your customers pay you is one of the biggest drivers of cash flow. Long payment terms or late-paying customers can leave you short, even when sales are strong. A solid accounts receivable process helps you stay on top of what's owed.

Seasonal patterns: many businesses experience quieter months where income drops but fixed costs like rent and wages remain the same. Planning ahead for these dips is essential.

Large or unexpected expenses: equipment breakdowns, tax bills, or one-off costs can drain your cash quickly if you haven't set aside reserves.

Growth: expanding your business often requires spending money before the additional revenue arrives. Hiring staff, buying stock, or investing in marketing all increase your outgoings in the short term.

How to calculate cash flow

Calculating your net cash flow is straightforward. You add up all the money that came into your business during a period and subtract everything that went out.

Net cash flow = total cash inflows - total cash outflows

Here's a simple example for a small UK business over 1 month:

- Cash inflows: customer payments of £18,000 + a VAT refund of £1,200 = £19,200

- Cash outflows: supplier payments of £7,500 + wages of £5,000 + rent of £1,500 + other costs of £800 = £14,800

- Net cash flow: £19,200 - £14,800 = £4,400 (positive)

A positive result means you brought in more cash than you spent. A negative result means you spent more than you received, which could signal a problem if it continues over several months.

For a more detailed breakdown, you can calculate cash flow from operations, investing, and financing separately, then add them together. Xero's cash flow calculator can help you run these numbers quickly. You can also explore how to calculate cash flow in more detail.

Cash flow statements and forecasts

Two key tools help you understand your cash flow: statements look backward at what's already happened, and forecasts look forward to predict what's coming.

What is a cash flow statement?

A cash flow statement reviews a past period, such as a month, quarter, or year, to show how cash was generated and spent. It breaks the figures down by operations, investing, and financing so you can see whether your cash is coming from sustainable sources.

This helps you check that your business isn't overly reliant on borrowing or asset sales to keep going. It's a key part of your financial reporting.

What is a cash flow forecast?

A cash flow forecast plots your expected income and expenses on a timeline to predict how much cash you'll have in the weeks or months ahead. It's one of the most practical tools for spotting potential shortfalls before they hit.

Regular forecasting helps you plan for quieter periods, time big purchases carefully, and make sure you can always cover your commitments. Xero's reporting tools, including Analytics Plus, let you build and monitor forecasts alongside your live financial data.

How to manage your cash flow

Managing cash flow well means staying on top of what's coming in, what's going out, and when. Here are practical steps you can take to keep your cash position healthy.

1. Invoice promptly and follow up

Send invoices as soon as work is complete or goods are delivered. Set clear payment terms and use automated invoice reminders to chase late payers. The sooner you invoice, the sooner you're likely to be paid.

2. Monitor your cash flow regularly

Don't wait until the end of the month to check your cash position. Use real-time dashboards and bank reconciliation to see exactly where you stand at any time. Catching issues early gives you more options to respond.

3. Build a cash buffer

Set aside a reserve to cover unexpected costs or quiet periods. Knowing your numbers starts with a clear plan; learning to create a small business budget can help. Even a small buffer gives you breathing room and reduces the risk of missing payments when income dips.

4. Review your payment terms

Look at both the terms you offer customers and the terms your suppliers offer you. If you're paying suppliers in 14 days but giving customers 30 days, you're funding that gap from your own cash. Negotiate where you can to close the timing mismatch.

5. Forecast ahead

Use a cash flow forecast to map out expected income and expenses over the coming weeks and months. This helps you plan for large outgoings like tax payments, stock purchases, or seasonal slowdowns. Update your forecast regularly as things change.

Cash flow vs profit

Cash flow and profit are related but they measure different things. Confusing the 2 is one of the most common financial mistakes small business owners make.

Profit is the amount left over after you subtract all your expenses from your revenue. It's calculated on an accrual basis, meaning it includes money you've earned but haven't yet received, and costs you've committed to but haven't yet paid.

Cash flow tracks the actual movement of money in and out of your bank account. It only counts cash when it's received or spent, not when it's invoiced or owed.

This means a business can be profitable on paper but still run out of cash. For example, if you've invoiced £50,000 in a month but only £20,000 has been paid so far, your profit figures look healthy but your cash position might be tight. That's why monitoring both is essential; profit tells you whether your business model works, and cash flow tells you whether you can keep the lights on.

Cash flow vs free cash flow, working capital, and liquidity

Cash flow is one of several measures of your business's spending power. Each term captures a slightly different angle, so it helps to understand how they compare.

- Cash flow refers to the general movement of money in and out of your business over a period

- Free cash flow is the cash left after you've covered operating costs and capital investments; it shows what's available to repay debt, pay dividends, or reinvest

- Working capital is the difference between your current assets and current liabilities, showing how much money you'd have left after covering short-term obligations

- Liquidity measures how easily your business can cover upcoming costs, usually expressed as a ratio

All 4 are useful for understanding your financial position, but cash flow is typically the starting point because it reflects what's actually happening in your bank account right now.

Manage your cash flow with Xero

Staying on top of your cash flow doesn't have to mean hours in spreadsheets. Xero gives you real-time visibility over your cash position, with automated bank reconciliation, invoicing with built-in payment reminders, and cash flow reporting that updates as your transactions come in. You can see where your business stands at any moment and spot potential issues before they become problems, so you can focus on running your business with confidence. Get one month free.

FAQs on cash flow

Here are answers to some common questions about cash flow for small businesses.

What is positive cash flow?

Positive cash flow means more money is coming into your business than going out over a given period. It's a sign that your business is generating enough income to cover its costs and potentially invest in growth.

What is the difference between cash flow and revenue?

Revenue is the total amount you've earned from sales, whether or not you've been paid yet. Cash flow only counts money that has actually been received or spent, so you can have high revenue but low cash flow if customers are slow to pay.

How often should you review your cash flow?

At a minimum, review your cash flow monthly. If your business has tight margins or variable income, checking weekly gives you a clearer picture and more time to act on any shortfalls.

Can a profitable business have negative cash flow?

Yes. A business can show a profit on its accounts but still have negative cash flow if there's a gap between when income is recognised and when it's actually received. Late customer payments and large upfront costs are common causes.

What is the easiest way to track cash flow?

Cloud accounting software like Xero connects to your bank account and updates your cash position automatically. This gives you an up-to-date view without manually updating spreadsheets, so you can check your cash flow whenever you need to.

Handy resources

Advisor directory

You can search for experts in our advisor directory

Cash flow forecast template

Download our free template to help predict cash flow for your business

Business analytics with Xero

See future cash flow, check financial health and track metrics

Disclaimer

This glossary is for small business owners. The definitions are written with their requirements in mind. More detailed definitions can be found in accounting textbooks or from an accounting professional. Xero does not provide accounting, tax, business or legal advice.