Solvency vs liquidity: differences and ratios explained

Learn how solvency vs liquidity helps you protect cash today and build a stronger business tomorrow.

Written by Lena Hanna—Trusted CPA Guidance on Accounting and Tax. Read Lena's full bio

Published Tuesday 24 February 2026

Table of contents

Key takeaways

- Monitor both solvency and liquidity regularly since they measure different timeframes - solvency shows your ability to meet long-term debts while liquidity measures your capacity to pay short-term bills within the coming months.

- Calculate your solvency ratio by dividing net income plus depreciation by total liabilities, aiming for 20% or higher to indicate strong financial health and ability to meet long-term obligations.

- Measure liquidity using the current ratio by dividing current assets by current liabilities, targeting a ratio between 1.5-3.0 to ensure you can cover immediate expenses and maintain smooth operations.

- Improve liquidity by speeding up invoice collections, monitoring cash flow regularly, and building cash reserves, while strengthening solvency through debt renegotiation and attracting new investment capital.

What does solvency mean in business?

Solvency is your business's ability to meet long-term financial commitments. A solvent business maintains positive net equity, meaning total assets exceed total liabilities.

What factors affect your solvency?

To keep your business solvent, you must:

- Stay profitable: Maintain consistent profits so total assets continue to exceed total liabilities.

- Manage your debts: Negotiate lower repayments and understand the terms of any collateral loans.

- Use your assets wisely: Ensure assets like inventory generate enough returns to cover your debts.

What is solvency vs profitability?

Solvency relates to your ability to pay debts over time, while profitability measures how much you earn relative to your costs. If you earn more than it costs to produce your goods or services, your business is profitable.

Strong profits boost your chances of staying solvent. However, a business that fails to manage debts or assets could become insolvent.

For example, taking out new loans without paying off existing ones can push total liabilities above total assets, resulting in insolvency.

Learn more about profitability.

How does solvency affect your business growth?

Stay solvent and you'll more easily:

- Access funding: Borrow from banks and lenders who feel confident you can repay them.

- Attract investors: Bring in resources and expertise to grow your business.

- Negotiate better deals: Use cash reserves to buy in bulk and lower your cost per unit.

- Plan for the future: Keep operations running smoothly and focus on long-term goals.

What does liquidity mean in business?

Liquidity measures your business's ability to pay bills and loan repayments in the coming months. It compares current assets against current liabilities (amounts owed within the coming year).

Current assets include cash, inventory, payments due, and anything that can be sold quickly. Liquidity is commonly expressed as a ratio, such as the current ratio, quick ratio, or cash ratio.

Other liquidity ratios

The current ratio is the most common liquidity measure, but two other ratios provide additional insight:

- Quick ratio (acid test ratio): Cash, cash equivalents, short-term investments, and receivables divided by current liabilities. This ratio only uses assets convertible to cash within three months, and a result of 1.0 or higher generally indicates solid short-term financial strength.

- Cash ratio: Cash and cash equivalents divided by current liabilities. This is the most conservative liquidity measure.

Learn more in our guide on liquidity ratios.

How liquid are your assets?

Assets vary in how quickly they convert to cash:

- Cash: Physical currency and savings account funds are your most liquid assets, available immediately.

- Accounts receivable:Invoices owed to you convert to cash relatively quickly, as they are typically collected in 60–90 days, though longer payment terms can still reduce liquidity.

- Physical assets:Buildings, equipment, and other resources can take months to sell, making them less liquid.

Liquidity vs other financial concepts

Liquidity relates to several other financial concepts. Here's how they differ:

- Liquidity: Measures how easily you can cover upcoming costs.

- Cash flow: Tracks the movement of cash in and out of your business.

- Working capital: Shows the money remaining after covering short-term obligations.

- Free cash flow: Represents cash left after capital investments.

How does liquidity affect business growth?

When expanding your business, liquidity helps you:

- Seize opportunities: Keep cash ready to launch new products or hire additional staff.

- Handle unexpected challenges: Cover surprise expenses like emergency repairs without disrupting operations.

- Maintain stability: Avoid scrambling for cheaper suppliers or alternative lenders during tight periods.

The main differences between solvency and liquidity

Understanding how solvency and liquidity differ helps you monitor your business's financial health more effectively.

Solvency takes a long-term view of your financial health, while liquidity focuses on the short term. The table below compares timeframes, what each measures, key ratios, and warning signs.

Table of the difference between solvency and liquidity

Monitor both metrics regularly to maintain a complete picture of your business's financial health.

How to measure solvency and liquidity in your business

Tracking your solvency and liquidity ratios helps you spot problems early and make informed decisions. Calculate each using the formulas below.

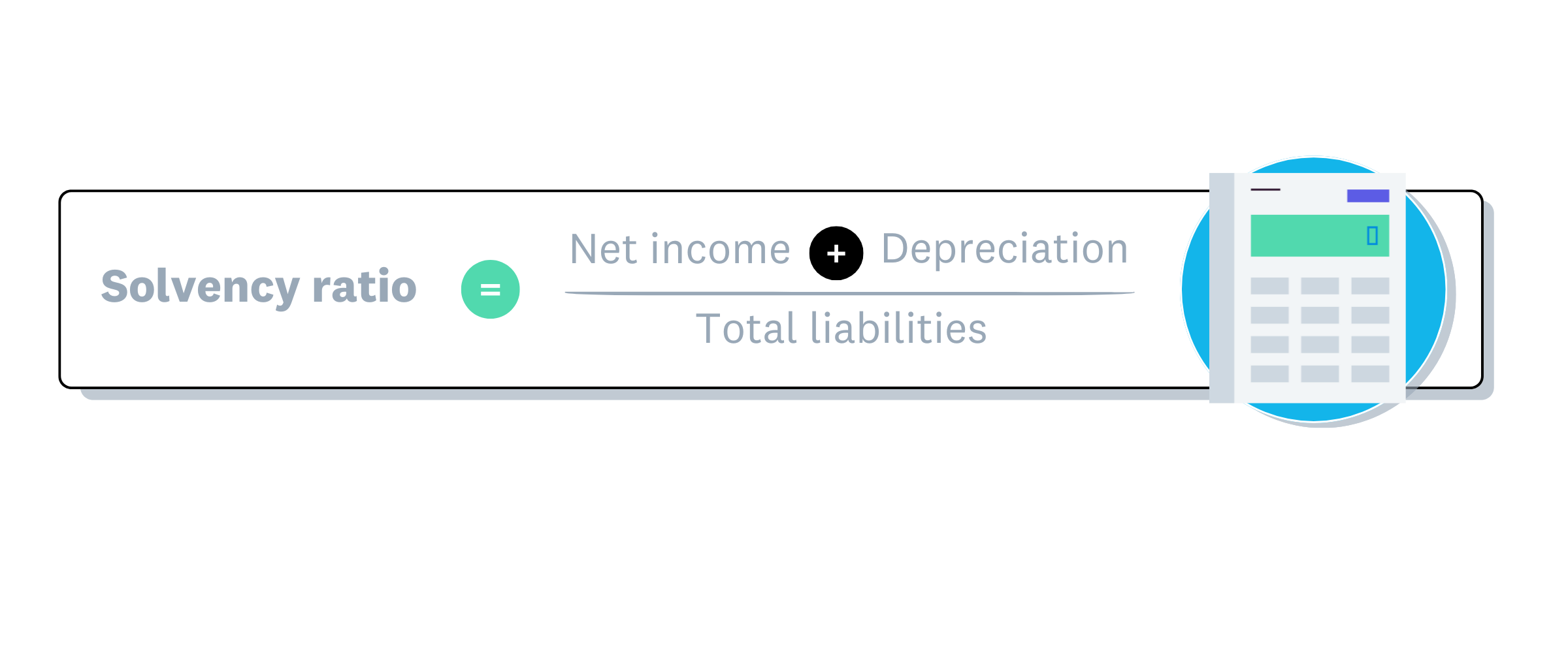

Solvency ratio formula

Use this formula to calculate your solvency ratio.

Solvency ratio formula

Example: Martha's cafe

Martha's cafe has:

- Net income: $50,000

- Asset depreciation: $10,000

- Total liabilities: $300,000

To calculate solvency, divide net income plus depreciation by total liabilities: ($50,000 + $10,000) ÷ $300,000 = 20%.

A ratio of 20% or above is considered healthy, as research shows a company is financially strong if it achieves a solvency ratio exceeding 20%.

*Depreciation is the decrease in asset value over time from normal wear and tear.

Liquidity ratio formula

Use one of these formulas to measure your business's liquidity.

There are several liquidity ratios, like the cash ratio, quick ratio, and the working capital ratio, which is a useful long-term measure of liquidity.

The working capital ratio formula is:

Example: Sadiq's sports shop

Sadiq's sports shop has:

- Current assets: $120,000

- Current liabilities: $80,000

To calculate liquidity using the current ratio, divide current assets by current liabilities: $120,000 ÷ $80,000 = 1.5.

While a ratio above 1.0 indicates good liquidity, a current ratio of 1.5–3.0 is generally considered healthy.

Sadiq can likely meet his short-term financial commitments.

Why solvency and liquidity matter for your small business

Both metrics play essential roles in keeping your business financially healthy.

Why solvency matters

A solvent business is financially stable. It can manage risks like clients not paying, use resources to grow, and keep shareholders confident. Poor solvency means trouble paying debts, which can lead to an excessive debt burden, and an insolvent business faces potential bankruptcy.

Why liquidity matters

A liquid business has enough cash to pay suppliers and staff on time. Good liquidity also protects against unexpected challenges like market changes, low productivity periods, or surprise expenses. Poor liquidity often stems from customers paying late, which slows cash flow.

Monitoring both metrics helps you make better decisions for daily operations and long-term planning.

Tips to improve your financial solvency and liquidity

These practical strategies can help strengthen your solvency and liquidity.

To improve solvency:

- Attract investors: Bring in new capital to strengthen your balance sheet.

- Renegotiate debt: Refinance or consolidate loans to reduce repayment pressure.

- Restructure operations: Adjust costs, including staffing, to match your financial position.

To improve liquidity:

- Monitor cash flow: Track cash regularly and plan payments accordingly.

- Benchmark performance: Compare your liquidity ratios against industry standards.

- Speed up collections: Make it easier for customers to pay invoices promptly.

- Build reserves: Maintain a cash buffer for unexpected expenses.

Track your solvency and liquidity with accounting software

Xero accounting software gives you a clear view of your financial health. Track daily spending in real time or review long-term solvency through detailed financial reports. Learn more about Xero's financial reports for your business.

Stay on top of both metrics and make confident decisions for your business. Get one month free and try Xero for your business.

FAQs on solvency and liquidity

Find answers to common questions about solvency and liquidity for small businesses.

What does it mean to provide liquidity?

When you provide liquidity, you ensure your business has enough cash to cover short-term bills and obligations. You can improve liquidity by speeding up cash flow, such as offering early payment discounts to customers.

Can my business have good solvency but poor liquidity?

Yes. Your business can be solvent with valuable fixed assets like land and buildings, yet struggle with liquidity due to weak cash flow. In this case, you can meet long-term debts but may have difficulty paying short-term bills.

Is solvency good or bad?

Solvency is good. It means your business can meet long-term financial obligations. Higher solvency makes it easier to borrow at favourable rates and withstand economic setbacks.

What is a good solvency ratio for my small business?

A solvency ratio of 20% or higher generally indicates your business can meet long-term obligations. However, healthy ratios vary by industry, so compare your results against sector benchmarks.

How often should I check my solvency and liquidity?

Review liquidity monthly or quarterly to catch cash flow issues early. Check solvency at least annually, or whenever you're considering major financial decisions like taking on new debt or seeking investment.

Which is more important for a small business: solvency or liquidity?

Both are critical, but they address different timeframes. Liquidity is your immediate priority because it keeps the business running day-to-day. Without it, you can't pay staff or suppliers. Solvency is your long-term goal, ensuring the business is financially viable over time. A healthy business needs to manage both.

Start using Xero for free

Access Xero features for 30 days, then decide which plan best suits your business.