What is working capital? Formula and how to calculate

Learn what working capital is, why it matters, and how to calculate it to keep cash flowing.

Written by Jotika Teli—Certified Public Accountant with 24 years of experience. Read Jotika's full bio

Published Saturday 7 March 2026

Table of contents

Key takeaways

- Calculate your working capital by subtracting current liabilities from current assets to determine if you have enough money to cover day-to-day expenses and short-term debts over the next 12 months.

- Maintain a working capital ratio between 1.2 and 2.0 for optimal financial health, as ratios below 1.0 indicate you can't cover your debts while extremely high ratios suggest you're holding too much cash that could be invested for growth.

- Improve your working capital by sending invoices immediately, negotiating longer payment terms with suppliers, and keeping optimal inventory levels to avoid tying up cash in unsold goods.

- Monitor your working capital regularly using accounting software to track real-time financial data, automate invoicing, and forecast cash flow to prevent shortfalls before they happen.

What is working capital?

Working capital is the difference between your business's current assets and current liabilities, measured in dollars. It shows how much money you have available to cover day-to-day expenses and short-term debts over the next 12 months.

Current assets and liabilities

Current assets are anything you can turn into cash within a year:

- Cash: Money in bank accounts and on hand

- Accounts receivable: Payments owed to you by customers

- Inventory: Stock you can sell

- Prepaid expenses: Costs paid in advance, like insurance

- Short-term investments: Investments you can liquidate quickly

- Tax refunds: Money owed to you by the government

Current liabilities are amounts you must pay within a year:

- Accounts payable: Bills you owe to suppliers

- Loan payments: Principal and interest due within 12 months

- Accrued expenses: Wages, bank fees, and other costs you've incurred but not yet paid

- Deferred revenue: Payments received for goods or services you haven't delivered yet

More about current liabilities

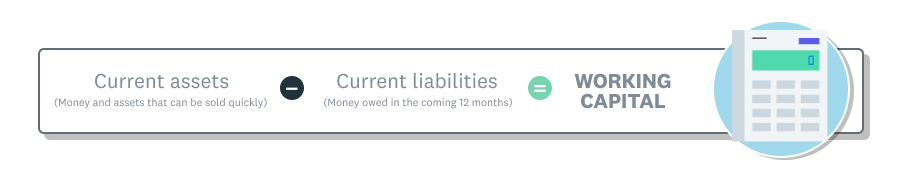

How to calculate working capital

To calculate working capital, subtract your current liabilities from your current assets. You'll need to project both figures for the next 12 months.

If you use accounting software, you can pull this information directly from your balance sheets and financial reports. Learn about Xero financial reports.

The working capital formula

A working capital formula example

Here's how a retail florist calculates their working capital:

- Add up current assets: Cash, inventory, and accounts receivable total $100,000.

- Add up current liabilities: Accounts payable, wages owed, and short-term loans total $75,000.

- Apply the formula: $100,000 − $75,000 = $25,000 in positive working capital.

This florist has enough assets to cover their short-term debts with $25,000 left over.

Working capital examples in different businesses

A "good" working capital figure depends on your industry. Businesses with long project timelines need more working capital than those with quick cash cycles. Here's how it works in different sectors.

Working capital in construction and manufacturing

Construction and manufacturing businesses often have irregular cash flow due to long project timelines. You may need to pay for materials, subcontractors, and labour upfront, but won't recover those costs until the project is complete.

Example: A building materials manufacturer calculates their working capital:

- Current assets: Cash ($100,000) + accounts receivable ($200,000) + inventory ($300,000) = $600,000

- Current liabilities: Accounts payable ($150,000) + short-term loans ($100,000) + accrued expenses ($50,000) = $300,000

- Working capital: $600,000 − $300,000 = $300,000

With $300,000 in positive working capital, this business has enough assets to cover its liabilities and weather uncertain markets.

Working capital in service businesses

Service businesses like consultancies and agencies don't hold inventory, so they typically need less working capital than product-based industries.

However, they often have higher accounts receivable because they invoice clients after completing work. You'll still need enough working capital to cover:

- Payroll and contractor payments

- Office and operating expenses

- Project costs before client payment arrives

Working capital in retail

Retail, wholesale, and hospitality businesses often hold significant inventory and depend heavily on steady revenue. You'll need enough working capital to buy stock in advance, especially before peak seasons.

The key is to balance inventory levels with sales. Too much stock ties up cash; too little means missed sales. Balancing this correctly keeps your working capital healthy.

The importance of working capital in business

Working capital matters because it reveals whether your business can pay its bills and invest in growth. Here's what it tells you:

- Operational health: Can you cover day-to-day expenses without borrowing?

- Resilience: Can you handle slow seasons or unexpected costs?

- Growth potential: Do you have surplus funds to reinvest in the business?

Lenders and investors also use working capital to assess how financially stable you are before approving loans or funding.

Positive vs negative working capital

- Positive working capital: Your current assets exceed your current liabilities. You can pay your bills, cover debts, and reinvest surplus funds into the business.

- Negative working capital: Your current liabilities exceed your current assets. You may struggle to meet debts without borrowing or raising funds. If this continues, your business could face financial trouble.

- Neutral working capital: Your assets and liabilities are roughly equal. This works if you're converting inventory into cash quickly, but leaves little buffer for unexpected expenses or reinvestment.

Very high working capital isn't always ideal either, as research from the Bank of Canada suggests that holding too many liquid assets eventually diminishes a bank's profitability.

Working capital vs working capital ratio

Working capital is a dollar amount: current assets minus current liabilities.

Working capital ratio (also called the current ratio) is a proportion: current assets divided by current liabilities. Innovation, Science and Economic Development Canada defines this ratio as a firm's ability to pay liabilities with current assets. It shows how many times over you can cover your short-term debts.

For example, if you have $100,000 in assets and $50,000 in liabilities:

- Working capital: $100,000 − $50,000 = $50,000

- Working capital ratio: $100,000 ÷ $50,000 = 2.0

Learn more about the working capital ratio.

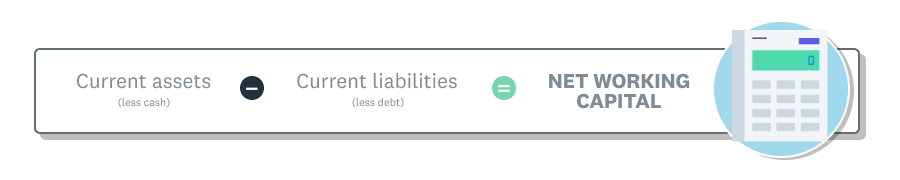

What is net working capital?

Net working capital (also called operating working capital) measures operational efficiency by excluding cash and debt from the standard working capital formula.

Here's how it differs from regular working capital:

- What it excludes: Cash (from assets) and debt (from liabilities)

- What it measures: How efficiently you operate daily to convert resources into revenue

- When to use it: When assessing longer-term finances, planning expansion, or working in industries with tight margins like retail, manufacturing, and distribution

The net working capital formula

Look again at the florist example. Suppose their current assets include $20,000 in cash, and their current liabilities include $10,000 in loan debts. The new formula for their net working capital is $80,000 ($100,000 – $20,000) – $65,000 ($75,000 – $10,000) = $15,000.

Working capital vs cash flow: what's the difference?

These two metrics measure different things:

- Working capital: Shows how much money remains after covering your short-term debts. It includes all current assets and liabilities, giving you a snapshot of financial health.

- Cash flow: Shows how money moves in and out of your business over time. It tracks actual cash on hand but doesn't include non-cash assets like inventory or accounts receivable.

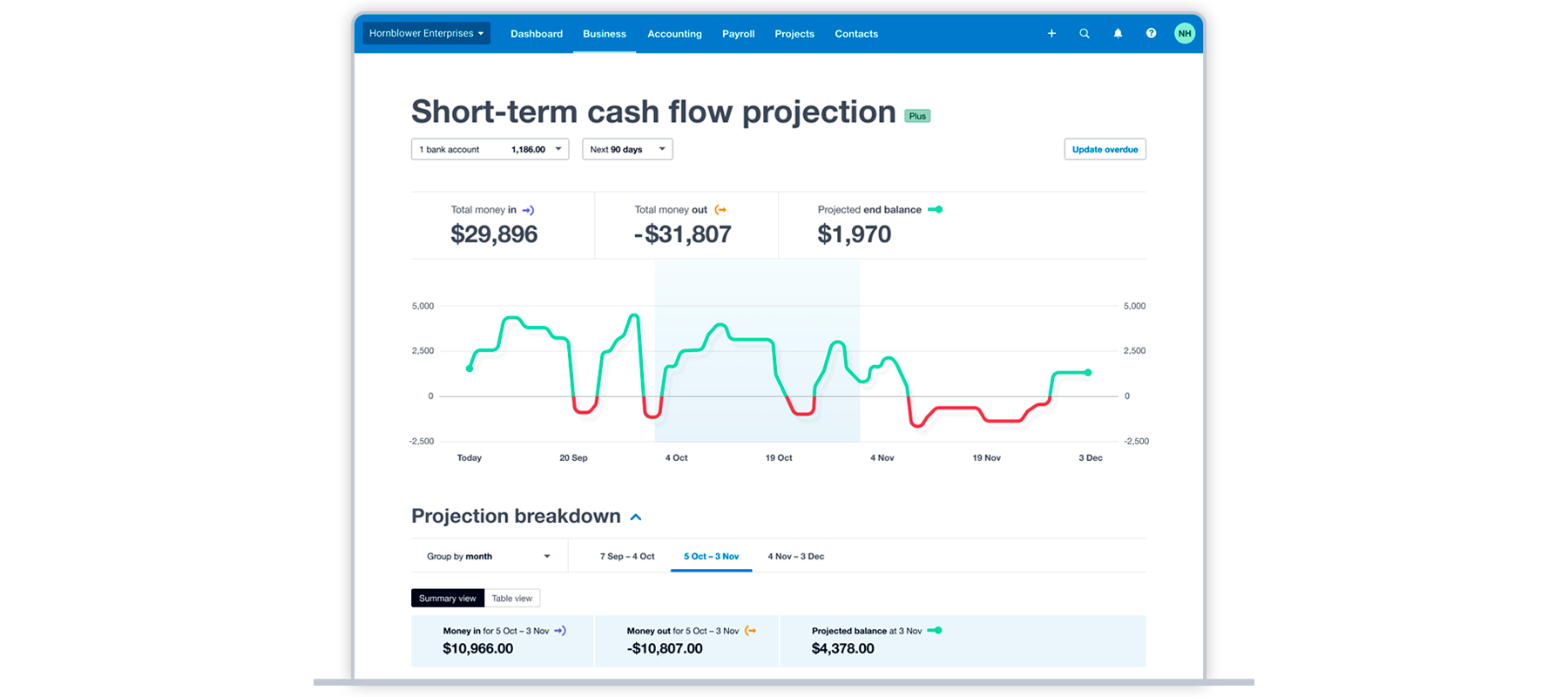

Here's an example from Xero's short-term cash flow projection, showing total money in and out for the next 90 days. Unlike working capital, it doesn't include liquid assets or show how well your business can adapt financially.

How to manage your working capital

Managing your working capital well keeps cash flowing, prevents shortfalls, and frees up funds for growth. Here's how to stay on top of it.

Manage your inventory

- Keep optimal stock levels: Avoid tying up cash in unsold goods or being understocked when demand spikes.

- Turn over inventory faster: Offer promotions or discounts on slow-moving stock to free up cash.

- Use inventory software: Track stock in real time, forecast demand, and automate reordering with tools like Xero's inventory management features.

Check out Xero's inventory management guide for more advice.

Control your expenses

- Review your spending: Identify where you can reduce costs without affecting quality or operations.

- Cut non-essentials: Focus spending on activities that directly help your business grow.

- Streamline processes: Use lean practices to reduce waste and improve efficiency.

Learn more about tracking business expenses.

Monitor your cash flow

- Check regularly: Review cash inflows and outflows to anticipate shortages or surpluses before they happen.

- Build a buffer: Set aside some profits as a reserve fund for lean periods.

Invest in software tools to streamline how you operate

Accounting software like Xero helps you run your business smoothly, which directly benefits your working capital. Here's how:

- Automate invoicing: Generate and send invoices automatically, track payment status, and follow up on overdue accounts without manual effort.

- Speed up payments: Send automatic reminders and offer multiple payment options to get paid faster.

- Track expenses in real time: Monitor spending as it happens so you can control costs and spot issues early.

- Access finances anywhere: Cloud-based software lets you check your financial data and respond to cash flow issues from any device.

These features let you better control your business finances, improving working capital so you can grow from a stable base.

Improve your working capital with Xero

Xero accounting software helps you manage your working capital by tracking assets and liabilities, streamlining invoicing, and giving you real-time financial insights.

With Xero you can:

- Automate invoicing and payments: Get paid faster with less manual work.

- Track inventory easily: Know what you have and what you need.

- See real-time financial insights: Make decisions based on current data.

- Monitor expenses: Spot cost issues before they affect your working capital.

- Forecast cash flow: Plan ahead and avoid shortfalls.

Ready to see how Xero can help? Get one month free on Xero pricing plans and start managing your working capital with confidence.

Learn more about Xero accounting software.

FAQs on working capital

Here are answers to common questions about working capital.

What is a good working capital ratio for small businesses?

A good working capital ratio for small businesses is typically between 1.2 and 2.0. A ratio below 1.0 means you don't have enough assets to cover your debts. Service businesses can operate with lower ratios than retailers, who need more working capital to manage inventory.

How can I improve working capital ratio?

To improve your working capital ratio:

- Send invoices immediately: Reduce payment turnaround time and get cash in faster. This shortens the collection period for accounts receivable, which is the average time between a credit sale and when you receive the cash.

- Negotiate longer payment terms: Ask suppliers for extended deadlines to slow cash outflows.

- Offer early payment discounts: Encourage customers to pay sooner with small incentives.

- Cut non-essential spending: Reduce overheads to keep more cash in your business.

What happens if my working capital ratio is too low?

A low working capital ratio means your business may struggle to cover short-term debts. If this continues, your business could become insolvent. Address the issue quickly by speeding up receivables, reducing expenses, or securing short-term financing.

What is a working capital loan?

A working capital loan is short-term financing that covers day-to-day operating costs when your business is struggling with cash flow. It's typically a last resort after other efforts to improve haven't worked.

Before taking on new debt, consult a financial advisor. Explore working capital financing at the Business Development Bank of Canada.

Is working capital the same as liquidity?

Not quite. Here's the difference:

- Liquidity: Measures how easily you can convert assets to cash to cover upcoming costs.

- Working capital: Measures how much money remains after you've covered those costs.

Both indicate financial health, but working capital gives you a clearer picture of your buffer for growth and unexpected expenses.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Start using Xero for free

Access Xero features for 30 days, then decide which plan best suits your business.