Assets vs liabilities: key differences and examples

Learn how assets vs liabilities guide smarter choices and strengthen cash flow and profit.

Written by Lena Hanna—Trusted CPA Guidance on Accounting and Tax. Read Lena's full bio

Published Tuesday 14 April 2026

Table of contents

Key takeaways

- Classify your assets and liabilities by timeframe to improve cash flow planning—current assets and liabilities involve transactions within 12 months, while fixed assets and long-term liabilities extend beyond 12 months.

- Calculate your owner's equity regularly using the formula Assets minus Liabilities equals Owner's Equity to understand your business's true net worth and financial health.

- Distinguish between liabilities and expenses since liabilities are amounts you owe that appear on your balance sheet, while expenses are immediate costs that reduce profits on your income statement.

- Review your balance sheet monthly with a professional accountant to spot potential issues early and ensure your assets exceed your liabilities for positive equity.

What's the difference between assets and liabilities?

Assets are resources your business owns that have future economic value. Liabilities are amounts your business owes to others, such as debts or obligations to deliver goods and services.

The key difference: assets increase your business's value, while liabilities reduce it. Understanding this distinction helps you see your true financial position.

What are small business assets?

Small business assets are everything your company owns that has monetary value. These resources can generate revenue, secure financing, or support daily operations.

Assets fall into three main categories:

- Physical assets: buildings, vehicles, equipment, and inventory

- Financial assets: cash, bank accounts, and investments

- Intangible assets: patents, trademarks, and brand value

The more assets your business holds, the stronger your financial position becomes.

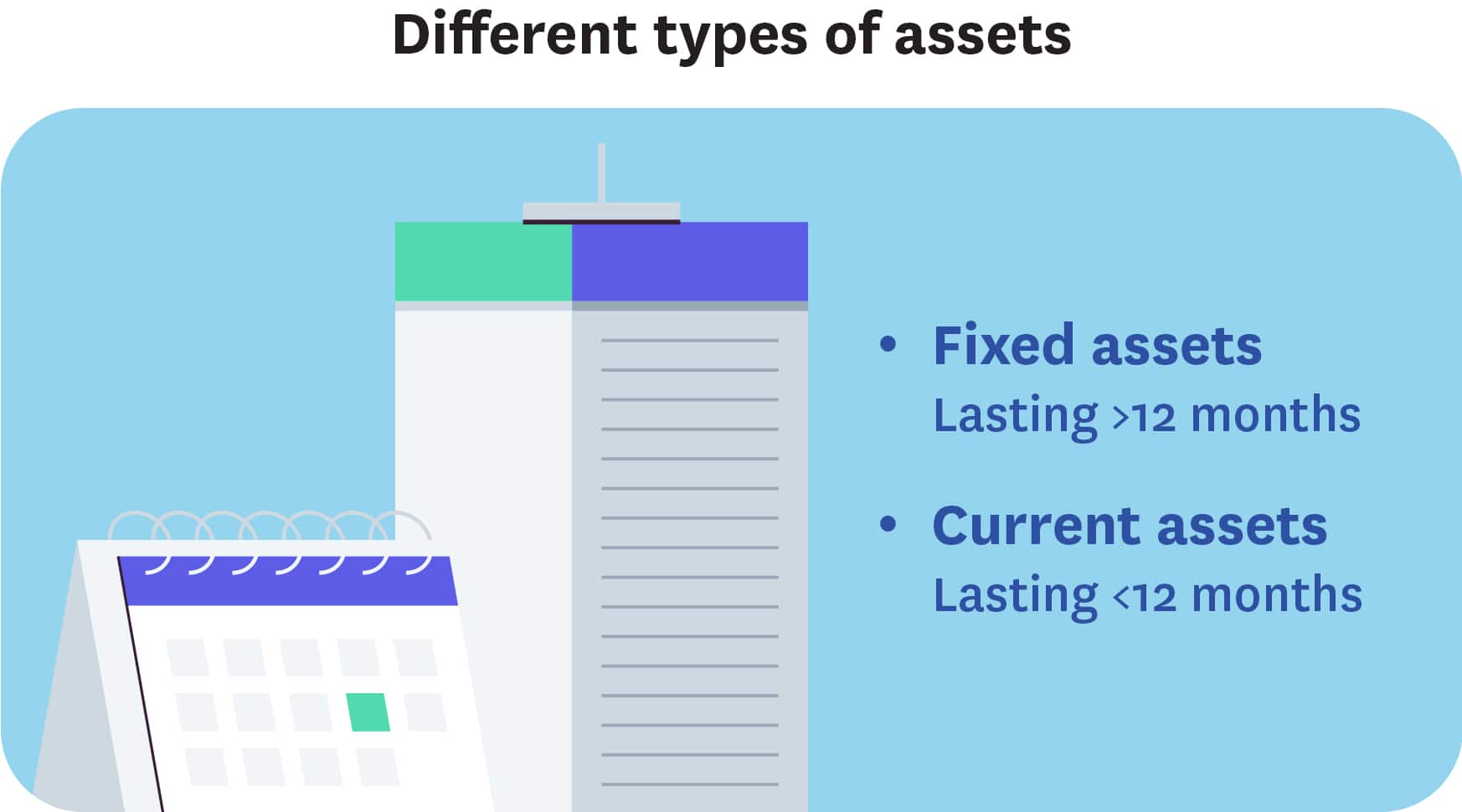

Different types of assets

Asset classification groups your assets by how long you expect to hold them. This distinction helps you understand your cash availability and long-term investments.

The two main types are:

- Current assets: items owned for 12 months or less, such as cash, inventory, and accounts receivable

- Fixed assets: items owned for longer than 12 months, such as buildings, equipment, and vehicles

Knowing which category each asset falls into helps you plan cash flow and make informed financial decisions.

Fixed assets

Fixed assets are long-term investments your business owns for more than 12 months. They come in two types:

Tangible fixed assets are physical items you can touch:

- real estate and buildings

- vehicles and equipment

- machinery

These assets depreciate over time, which affects your profits.

Intangible fixed assets are non-physical items that hold value:

- patents and copyrights

- trademarks and brand value

You must test goodwill for impairment at least once a year to confirm it hasn't lost value.

Current assets

Current assets are short-term resources you can convert to cash within 12 months, including financial instruments like short-term government securities. They fund daily operations and cover immediate expenses.

Common current assets include:

- cash in bank accounts and petty cash

- accounts receivable from customers, which can include both private and public sector clients

- inventory ready for sale

- prepaid expenses such as insurance or rent

Here are common examples you might find in a small business:

- cash in your bank account or cash register

- accounts receivable from customers, which can include both private and public sector clients

- inventory or stock for sale

- business equipment such as computers and machinery

- company vehicles

- property and buildings

- patents, trademarks, and copyrights

What are small business liabilities?

Business liabilities are financial obligations your company owes to others. These include debts, unpaid bills, and commitments to pay in the future.

Managing your liabilities helps you meet financial obligations on time and maintain strong relationships with suppliers and lenders.

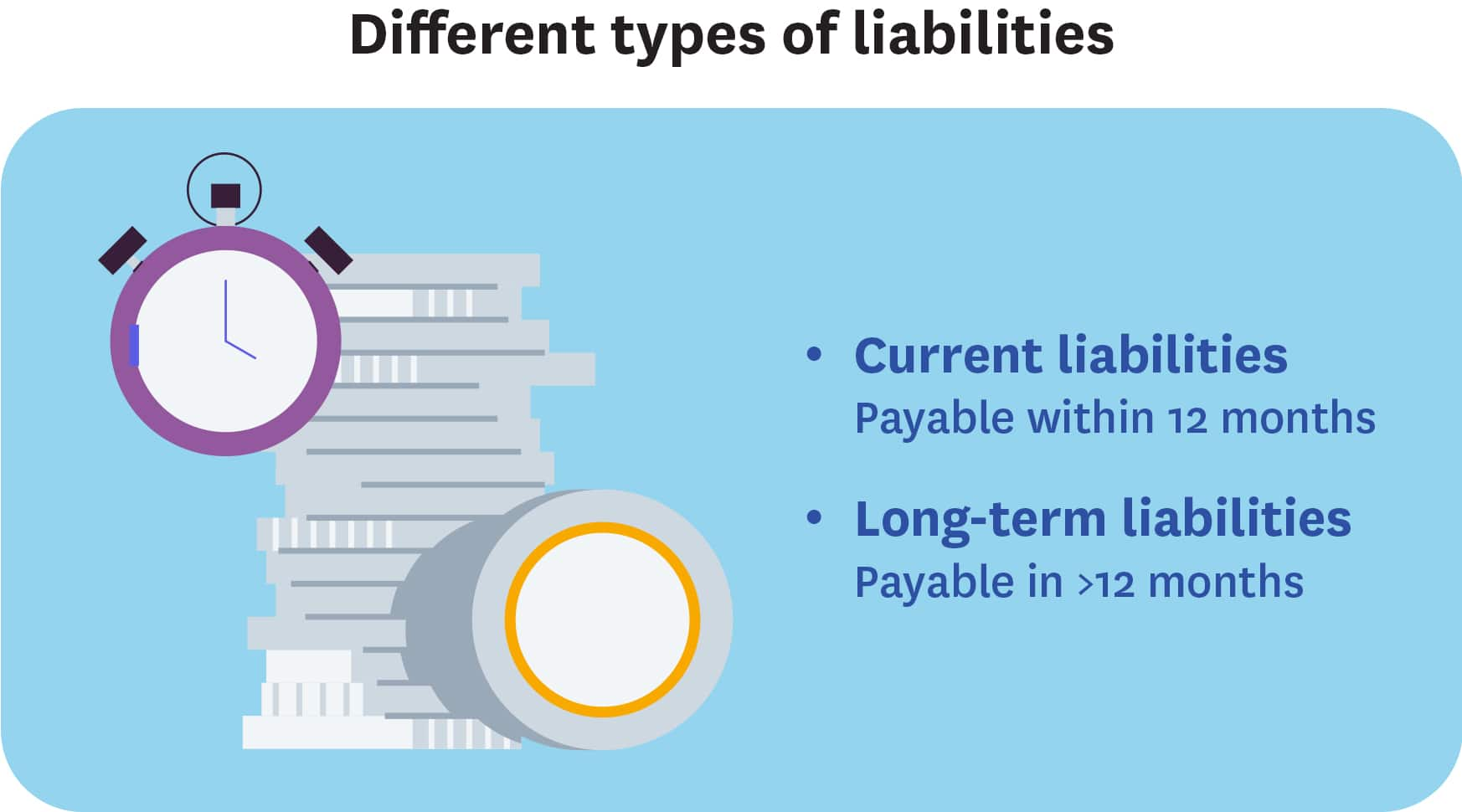

Different types of liabilities

Liability classification groups your debts by when payment is due. This helps you plan cash flow and prioritize payments.

The two main types are:

- Current liabilities: amounts due within 12 months, such as bills, salaries, and short-term loans

- Long-term liabilities: amounts due beyond 12 months, such as mortgages and long-term loans

Keep your total liabilities lower than your total assets to maintain positive equity and financial health.

Current liabilities

Current liabilities are debts you must pay within 12 months, often within just a few months. These cover your daily business operations.

Common current liabilities include:

- accounts payable to suppliers

- staff salaries and benefits due

- business credit card balances

- bank overdraft fees

Long-term liabilities

Long-term liabilities are debts payable beyond 12 months. These typically involve larger amounts and structured payment plans.

Common long-term liabilities include:

- business loans with multi-year terms

- mortgages for property financing

- deferred taxes due in future periods

You can only recognize a deferred tax asset if you expect to have future taxable profit.

Liabilities represent your financial obligations. Keeping track of them is crucial for managing your cash flow.

Common liabilities include:

- accounts payable to suppliers

- salaries and wages owed to employees

- business loans or lines of credit

- credit card balances

- taxes owed to the government

- customer deposits or deferred revenue for services not yet delivered

If you don't meet loan covenants, a long-term loan can become a current liability and may require immediate repayment.

Is a liability the same as an expense?

Liabilities and expenses are not the same, though many business owners confuse them.

Expenses are costs of running your business that reduce profits immediately:

- rent, utilities, and supplies

- items recorded on your income statement

- costs recognized when incurred

Liabilities are amounts you owe to others that appear on your balance sheet:

- loans, unpaid bills, and taxes payable

- obligations you must settle in the future

- amounts that don't immediately affect profits

Understanding this difference helps you manage cash flow and plan your finances accurately.

Valuing your business: seeing what it's worth

Owner's equity represents your business's net worth after subtracting what you owe from what you own. The Canada Revenue Agency requires this figure for reporting total shareholder equity.

Assets - Liabilities = Owner's Equity

The result tells you where your business stands:

- Positive equity: your assets exceed your liabilities

- Negative equity: your liabilities exceed your assets

- Zero equity: your assets and liabilities are equal

Knowing your net worth matters when applying for a loan or seeking investors. Lenders and investors want to see that your business is financially viable before committing funds.

Accounting for your assets and liabilities

Both your assets and liabilities appear on your business's balance sheet. This financial statement provides a snapshot of what you own, what you owe, and your net worth at a specific point in time.

The balance sheet has two columns: assets on the left, and liabilities plus owner's equity on the right. Double-entry bookkeeping keeps both sides equal. Every transaction has a debit and a credit entry, so if the two sides don't match, there's an error.

Common errors that prevent a balance sheet from balancing include:

- duplicate entries

- incorrect dates

- missing transactions

- wrong inventory numbers or values

Check and correct these errors in your accounting ledger to balance your books. Filing a balance sheet is a statutory requirement for many financial institutions under Canadian law. The Bank Act and the Trust and Loan Companies Act outline these requirements.

Reviewing your balance sheets

Review your balance sheet and other financial statements regularly with a professional. An accountant can help you understand your financial position, spot potential issues, and plan your next steps.

Xero accounting software helps you create your balance sheet, income statement, and profit and loss statement quickly. Automation reduces manual errors, which is especially helpful if you're audited.

Manage your assets and liabilities with confidence

Understanding the difference between assets and liabilities helps you see your true financial position. When you know what you own and what you owe, you can make smarter decisions about loans, investments, and growth.

Xero accounting software tracks your assets and liabilities automatically. It generates accurate balance sheets and shows your financial position in real time so that you can review your numbers anytime, from anywhere. Get one month free.

FAQs on assets and liabilities

Here are answers to common questions about assets and liabilities in small business accounting.

What's assets minus liabilities?

Assets minus liabilities equals owner's equity, also called your business's net worth. This figure shows the value that belongs to you after paying all debts.

Is cash an asset or liability?

Cash is always an asset. It's the most liquid asset because you can use it immediately to pay expenses or invest in your business.

How do I know if something is an asset or liability?

Ask two questions: Does this item provide future value to your business? Or is it something you need to pay?

If it provides value, it's an asset. If it's an obligation you must settle, it's a liability.

How can I improve my asset-to-liability ratio?

Increase your assets by building cash reserves, collecting receivables faster, or investing in equipment that generates revenue. Reduce your liabilities by paying down debt, avoiding unnecessary borrowing, and negotiating better payment terms with suppliers.

What are the most common current liabilities for small businesses?

The most common current liabilities include:

- accounts payable to suppliers

- credit card balances

- wages owed to employees

- sales tax collected but not yet remitted

- short-term loan payments due within 12 months

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Start using Xero for free

Access Xero features for 30 days, then decide which plan best suits your business.