Solvency vs liquidity: differences, ratios and tips

Learn solvency vs liquidity to gauge cash strength and long term health, make smarter funding and growth decisions.

Written by Lena Hanna—Trusted CPA Guidance on Accounting and Tax. Read Lena's full bio

Published Wednesday 18 February 2026

Table of contents

Key takeaways

- Monitor both solvency and liquidity regularly since they measure different aspects of financial health - solvency shows your ability to meet long-term debts while liquidity indicates whether you can pay immediate bills and expenses.

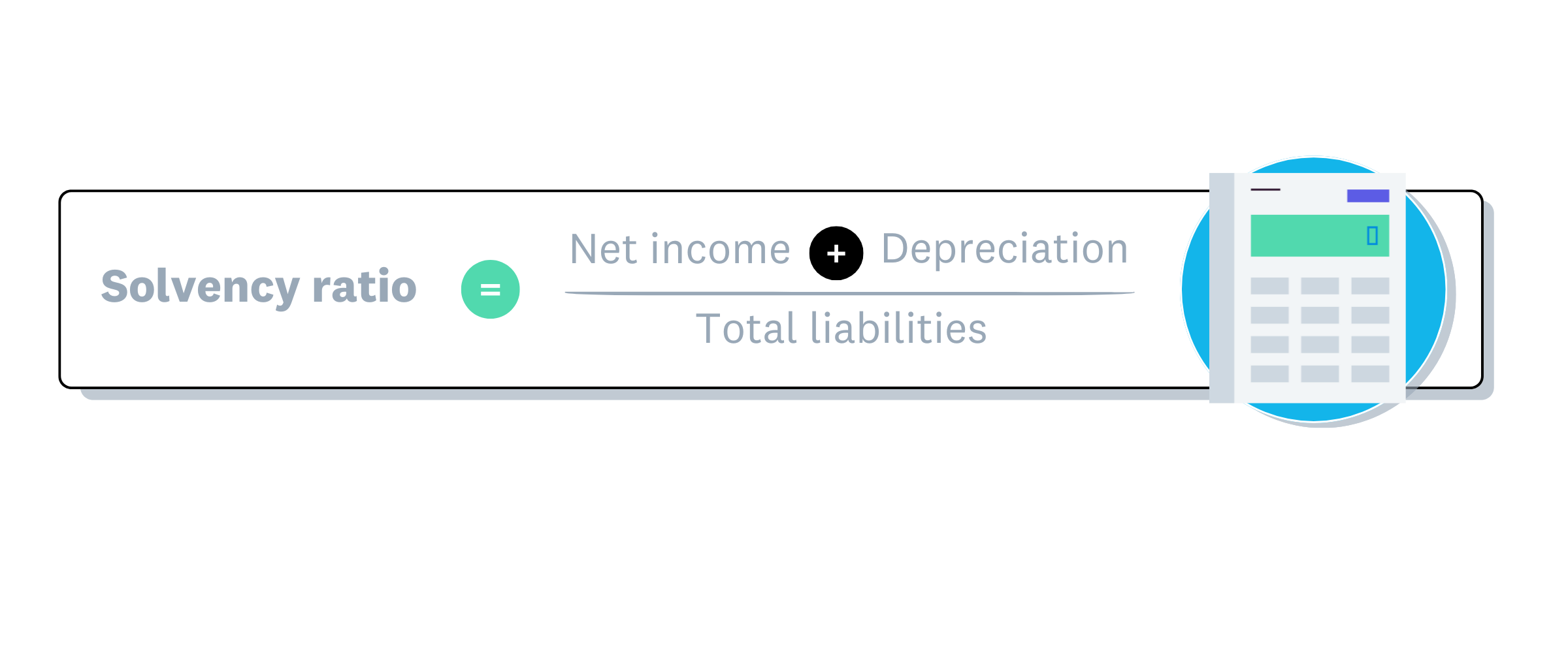

- Calculate your solvency ratio by dividing net income plus depreciation by total liabilities, aiming for 20% or higher to demonstrate strong long-term financial stability to lenders and investors.

- Improve liquidity by making it easier for customers to pay invoices quickly, maintaining cash reserves for unexpected expenses, and regularly tracking cash flow to plan payments effectively.

- Recognise that a business can have good solvency but poor liquidity if most assets are tied up in property or equipment rather than readily available cash, so track both metrics independently.

What does solvency mean in business?

Solvency refers to how well a business can meet its long-term financial commitments. A 'solvent' business must maintain a positive net equity, meaning its total assets are worth more than its total liabilities.

What factors affect your solvency?

To keep your business solvent, you must:

- stay profitable: Your profits must be consistent enough to keep your balance sheet in good shape. This means your total assets need to continue to exceed your total liabilities

- manage your debts: You might negotiate lower repayments on any loans. When it comes to collateral loans (which use your assets as security), ask your lender exactly what happens if you can't pay on time

- use your assets wisely: Your assets (things you own, like inventory) must generate enough financial returns to cover your debts. Optimise how you use each asset; for instance, track your inventory to avoid waste

Understanding how solvency impacts growth helps you plan for the future.

How does solvency affect your business growth?

Stay solvent and you'll more easily:

- borrow money from banks and lenders who'll feel more confident that you can pay them back

- attract potential investors to bring more resources and expertise to your business

- get better deals with suppliers by using your cash reserves to buy in bulk, and therefore lower your cost per unit

- keep your business running smoothly and make plans for the future

What does liquidity mean in business?

Liquidity measures a business's ability to pay its bills and make loan repayments in the coming months. It's commonly expressed as a ratio, like the cash ratio or quick ratio.

Liquidity compares current liabilities (amounts owed within the coming year) against current assets. Current assets include cash, inventory, payments due, and any assets that can be sold quickly.

Beyond the current ratio, there are other ways to measure liquidity.

Other liquidity ratios

Although the current ratio is the most common way for small businesses to measure liquidity, there are two other ratios:

- Quick ratio (or acid test ratio): It only uses assets that can be changed into cash within three months. Cash, cash equivalents, short-term investments and receivables divided by current liabilities (debts due to be paid within three months). Or alternatively, current assets minus inventory and prepaid expenses divided by current liabilities (debts due to be paid within three months)

- Cash ratio: Cash and cash equivalents divided by current liabilities

Learn more in our guide on liquidity ratios.

Not all assets convert to cash at the same speed.

How liquid are your assets?

Some assets are highly liquid – that is, they can be quickly converted to cash.

Cash (physical currency and funds in savings accounts that can be withdrawn immediately) is your most liquid asset.

Accounts receivable is the balance of invoices owed to you as part of your regular operations. These are treated as liquid assets because they can be converted to cash relatively quickly. The longer you give your customer to pay you, the less liquid this asset is.

Other assets are less liquid. Physical assets (resources your business owns, like buildings or equipment) aren't that liquid as it can take months to sell them before you get any cash.

It helps to understand how liquidity compares to similar financial concepts.

Liquidity vs other financial concepts

You might hear about liquidity in relation to other terms, like cash flow. Here's how they compare. Liquidity shows how easily your business can cover its upcoming costs:

- Cash flow refers to the general availability of cash

- Working capital shows how much money you have left after covering these upcoming costs

- Free cash flow is the amount of cash left after making capital investments

Liquidity plays an important role in your ability to expand.

How does liquidity affect business growth?

When it comes to expanding your business, liquidity can help you:

- seize opportunities: with cash ready to launch a new product, or take on more staff

- prepare for unexpected challenges: if your liquidity is high, you'll have cash ready to, say, pay for a rain-damaged roof

- maintain stability: since you won't need to adapt your operations to find cheaper suppliers, different lenders, and so on

The main differences between solvency and liquidity

Solvency takes a long-term view of your financial health, while liquidity focuses on the short term. The table below outlines the differences between solvency and liquidity.

Table of the difference between solvency and liquidity

Keep a steady eye on both your business's liquidity and solvency to stay on top of its financial picture.

Why solvency and liquidity matter for your small business

A solvent business is financially stable. It can manage risk (such as clients not paying), use its resources to grow, and keep the shareholders happy. A business with poor liquidity will struggle to pay its staff and suppliers, and insufficient liquidity creates serious risks, as diminished capital flow is a characteristic of some bankrupt companies. This might be because their customers pay them late, which slows their cash flow.

A business with poor solvency will have trouble paying its debts. And an 'insolvent' business is in financial distress and may face bankruptcy.

A business with liquidity has enough cash to pay its suppliers and team. This liquidity also protects it against financial difficulties, like periods of low productivity due to illness, changes in market conditions, and unexpected costs.

By watching your solvency and liquidity, you'll make better decisions for both your daily operations and your long-term financial planning.

How to measure solvency and liquidity in your business

To understand your financial position, look at the ratios that measure solvency and liquidity.

The solvency ratio shows your ability to meet long-term obligations.

Solvency ratio formula

Solvency ratio formula

Solvency ratio calculation example

Martha owns a cafe that has:

- A net income of $50,000

- Asset depreciation* of $10,000

- Total liabilities of $300,000

To work out her solvency, she divides 60,000 (50,000 + 10,000) by 300,000, which equals 20%. A ratio of 20% or above indicates good health, as financial experts consider a company financially strong when it achieves a solvency ratio exceeding 20%, so Martha's business has a good chance of paying its debts over the years.

*Depreciation is the decrease of the value of your assets over time from normal wear and tear. You enter it on your balance sheet as a deduction from the asset's value.

Now let's look at how to calculate liquidity.

Liquidity ratio formula

There are several liquidity ratios, like the cash ratio, quick ratio, and the working capital ratio, which is a useful long-term measure of liquidity.

Here's the formula for the working capital ratio:

Liquidity ratio calculation example

Sadiq runs a sports shop that has:

- Current assets of $120,000

- Current liabilities of $80,000

To work out his liquidity (using the current ratio), he must divide 120,000 by 80,000 to equal 1.5. Since this is above 1.0, his liquidity is good and it's likely he can meet his short-term financial commitments, although creditors and investors often prefer to see higher liquidity ratios, such as 2 or 3.

Tips to improve your financial solvency and liquidity

These tips can help your business stay (or become) solvent and liquid.

To improve your solvency, consider these strategies:

- Attract new investors to your business

- Look for ways to renegotiate, refinance, or consolidate bank loans

- Consider restructuring your business, possibly by making some staff redundant

To improve your liquidity, try these approaches:

- Regularly measure your cash flow and plan your payments in line with it

- Benchmark your liquidity against industry standards to see how you stack up

- Make it easier for customers to pay their invoices

- Consider maintaining a cash reserve for unexpected expenses

Use Xero to track your solvency and liquidity

Xero accounting software helps you track both solvency and liquidity in real time. Use financial reports to monitor your long-term position, and check daily cash flow to stay on top of short-term obligations.

With Xero, you can generate balance sheets to calculate solvency ratios, track cash flow for liquidity monitoring, and access real-time data from anywhere.

Ready to get the full picture of your business finances? Get one month free or learn more about Xero's financial reports for your business.

FAQs on solvency and liquidity

Common questions about solvency and liquidity answered below.

Can my business have good solvency but poor liquidity?

Yes. A business can be solvent (total assets exceed total liabilities) while struggling with liquidity (not enough cash to pay immediate bills). For example, a company owning valuable property may have strong solvency but weak liquidity if most of its value is tied up in buildings rather than cash.

Is solvency good or bad?

Solvency is good. The financial solvency definition is being able to meet your long-term financial obligations.

What is a good solvency ratio for my small business?

It depends on your industry. In general, a ratio of 20% or more indicates you can meet your long-term financial obligations, with some financial experts considering a ratio above 20–25% healthy.

What is an example of solvency?

A business with $500,000 in total assets and $300,000 in total liabilities has positive solvency. Its assets exceed its debts by $200,000, meaning it can meet long-term financial obligations. This business would have a solvency ratio of approximately 17% if net income plus depreciation equals $50,000.

Which is more important: solvency or liquidity?

Both matter, but for different reasons. Liquidity keeps your business running day-to-day by ensuring you can pay bills and staff. Solvency determines your long-term survival and ability to secure financing. Most small businesses should monitor liquidity more frequently (weekly or monthly) while reviewing solvency quarterly.

Start using Xero for free

Access Xero features for 30 days, then decide which plan best suits your business.