Accumulated depreciation: definition, formula, examples

Learn how accumulated depreciation impacts your assets and cash flow, and how to calculate it.

Written by Lena Hanna—Trusted CPA Guidance on Accounting and Tax. Read Lena's full bio

Published Tuesday 17 March 2026

Table of contents

Key takeaways

- Calculate accumulated depreciation using the straight-line method by subtracting salvage value from asset cost, dividing by useful life, then multiplying by the number of years owned to track total depreciation over time.

- Record accumulated depreciation as a contra asset on your balance sheet that reduces the original asset value, helping you show realistic asset worth to stakeholders and make informed replacement decisions.

- Use depreciation expense to reduce your taxable income each year while preserving cash flow, since depreciation is a non-cash expense that gets added back on your cash flow statement.

- Track accumulated depreciation with cloud accounting software to automate calculations and journal entries, ensuring accurate financial statements without manual spreadsheet errors as your business grows.

What is accumulated depreciation?

Accumulated depreciation is the total amount an asset has depreciated since you bought it. This running total shows how much value your asset has lost over time due to wear, tear, and aging. You'll find it on your balance sheet, where it reduces the original cost of your assets to reflect their current book value.

Tracking accumulated depreciation helps you:

- Record accurate values: Show true asset worth on your financial statements

- Calculate book value: Subtract accumulated depreciation from original cost

- Make informed decisions: Use realistic asset values for planning and reporting

For example:

- Office furniture that cost $5,000 and depreciates at $1,000 each year has a book value of $2,000 after three years.

- Machinery cost $25,000, with $2,500 depreciation each year. After six years it has depreciated by $15,000, leaving a book value today of $10,000.

Depreciation vs accumulated depreciation

Depreciation is the annual expense that reduces an asset's value each year. Accumulated depreciation is the running total of all depreciation expenses since you bought the asset.

Key differences:

- Depreciation: Annual expense that appears on your income statement

- Accumulated depreciation: Cumulative total that appears on your balance sheet

- Frequency: Recorded yearly for depreciation; grows continuously for accumulated depreciation

How accumulated depreciation works

Accumulated depreciation works by pairing with a specific asset on your balance sheet. It's a contra asset account, which means it has a credit balance that offsets the debit balance of an asset.

Each time you record depreciation expense on your income statement, you also increase the balance in the accumulated depreciation account. This gradually reduces the asset's book value (original cost minus accumulated depreciation) over its useful life. This gives you a more realistic picture of your asset's current worth without removing its original cost from your books.

Is accumulated depreciation an asset or a liability?

Accumulated depreciation is a contra asset, not an asset or liability. It appears on your balance sheet as a negative value that reduces your total assets.

Why it's not a liability:

- No debt owed: You don't have to repay accumulated depreciation

- No obligation: It represents value loss, not money owed to anyone

A contra asset works by offsetting the value of a related asset account. Here's how it functions:

- Negative value: Appears as a reduction on your balance sheet

- Asset offset: Reduces the original cost of your assets

- Realistic valuation: Reflects what your assets are actually worth today

Why understanding accumulated depreciation matters for your business

Understanding accumulated depreciation helps you plan ahead and make better business decisions.

Business planning benefits:

- Asset replacement timing: Know when to replace equipment before it breaks

- Maintenance budgeting: Predict upcoming repair costs

- Accurate valuations: Show realistic asset worth to stakeholders

Tracking depreciation also strengthens your financial position.

Financial benefits:

- Tax savings: Reduce taxable income and keep more cash

- Better financing: Improve loan approval chances with accurate asset values

- Investment readiness: Present a realistic financial position to investors

How does accumulated depreciation affect financial statements?

Accumulated depreciation on the balance sheet

Accumulated depreciation reduces your asset values from original cost to current worth. It appears directly below the related asset, showing the net book value after accounting for wear and tear over time.

Accumulated depreciation on the income statement

Depreciation expense appears on your income statement and reduces your taxable income each year. For instance, under certain Canadian tax rules, eligible businesses can deduct the full cost of specific properties, up to $1.5 million in a tax year.

Tax benefits of recording depreciation:

- Lower taxable income: Reduce profits on paper through depreciation expense

- Tax savings: Pay less tax without spending actual cash

- Cash preservation: Keep more money available in your business

Accumulated depreciation on the cash flow statement

Depreciation gets added back to your cash flow because it's a non-cash expense.

While depreciation reduces your net income on the income statement, no money actually leaves your business. On the cash flow statement, this amount is added back to show your true cash position. For example, CPA Canada's 2023 cash flow statement shows an adjustment of $1,435 (in thousands) for amortization to reconcile net income to cash flow.

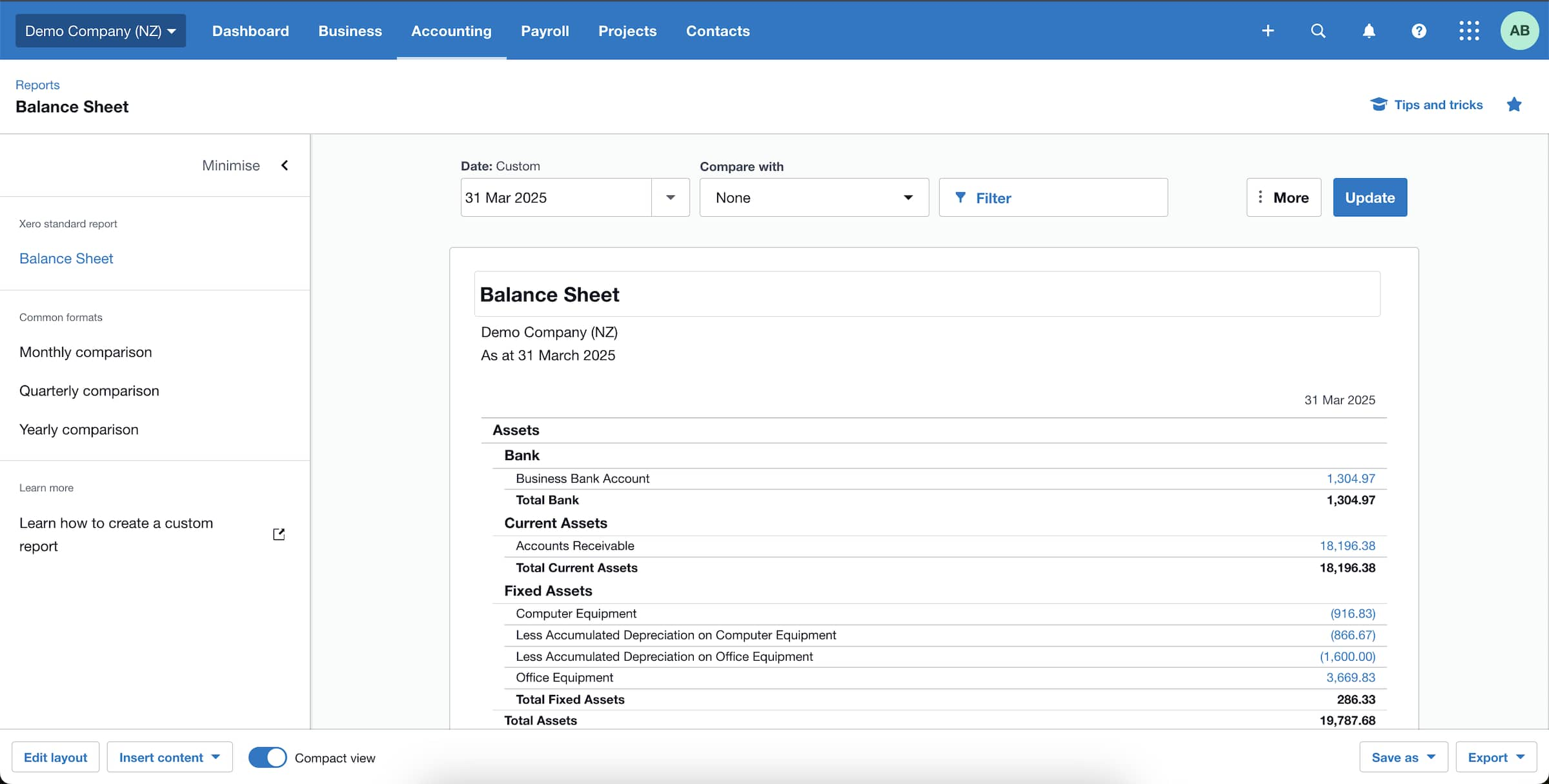

Example: Balance sheet for accumulated depreciation

This example shows how accumulated depreciation changes the net book value of assets and affects your overall financial health.

How to calculate accumulated depreciation

Calculating accumulated depreciation requires choosing a depreciation method. Most small businesses use the straight-line method for its simplicity.

For tax purposes, the Canada Revenue Agency applies specific Capital Cost Allowance (CCA) rates. For example, certain non-residential buildings used for manufacturing can include an additional allowance of 6% for a total rate of 10% in certain cases.

The straight-line depreciation calculation

The straight-line depreciation formula is:

Annual depreciation = (asset cost − salvage value) ÷ useful life

Authoritative bodies like CPA Canada use this method, defining estimated useful lives for assets like furniture (three to 10 years) and computer software (three to five years).

Formula components:

- Asset cost: The original purchase price of the asset

- Salvage value: The estimated resale or scrap value at end of use

- Useful life: The expected number of years you'll use the asset

How each factor affects your calculation:

- Shorter useful life: Increases annual depreciation expense

- Higher salvage value: Decreases annual depreciation expense

- Higher asset cost: Increases annual depreciation expense

Calculate straight-line depreciation

Now, let's calculate accumulated depreciation using the straight-line depreciation method. In this example, the asset costs $1,000, has a useful life of five years, and a salvage value of $100.

Step 1: Calculate the annual depreciation expense

Apply the straight-line formula to find your yearly depreciation amount.

Using the example above:

($1,000 – $100) ÷ 5 = $180 per year

Step 2: Track accumulated depreciation each year

Create a depreciation schedule to track how accumulated depreciation grows over time. Each year, add the annual depreciation expense to the running total.

In our example:

- Year 1: 1 × $180 = $180

- Year 2: 2 × $180 = $360

- Year 3: 3 × $180 = $540

- Year 4: 4 × $180 = $720

- Year 5: 5 × $180 = $900

Step 3: Calculate the asset's book value at a point in time

Use the formula:

Book value = initial cost – accumulated depreciation

In our example, after three years, the asset's book value is:

$1,000 – $540 = $460

Other depreciation methods

While straight-line depreciation is the simplest method, other approaches may better suit certain assets or tax situations.

Common alternative methods include:

- Declining balance method: Applies a fixed percentage to the remaining book value each year, resulting in higher depreciation in early years

- Double-declining balance method: Uses twice the straight-line rate for accelerated depreciation in the early years of an asset's life

- Units of production method: Bases depreciation on actual usage or output rather than time, ideal for machinery or equipment with variable use

Your accountant can help you choose the best method for your business and ensure you comply with tax regulations.

How to record accumulated depreciation

The journal entry for accumulated depreciation debits Depreciation Expense and credits Accumulated Depreciation. This entry ensures your financial statements reflect the asset's reduced value.

Record the entry as:

- Debit: Depreciation Expense

- Credit: Accumulated Depreciation

Here's what each part of the entry does:

- Debit to Depreciation Expense: Increases your total expenses on the income statement and lowers your taxable income for the period

- Credit to Accumulated Depreciation: Increases the contra asset balance, which reduces the net book value of your asset on the balance sheet

In Canada, claim this deduction by entering the amount from Form T777 on line 22900 of your tax return.

This simple entry keeps your records straight without affecting your cash flow, as no actual money is spent.

Manage depreciation efficiently with cloud accounting

Tracking depreciation manually can be time-consuming, especially as your business grows and acquires more assets. Spreadsheets can lead to errors that affect your financial reports and tax filings.

Cloud accounting software simplifies tracking your fixed assets and calculating depreciation. With a platform like Xero, you can set up a fixed asset register and automate depreciation calculations. Once you enter an asset's details, the software handles the monthly or yearly journal entries for you.

This saves you time and ensures your asset values stay up-to-date. You get a clear, accurate picture of your financial health and can run your business with confidence. Get one month free to see how Xero can streamline your asset management.

FAQs on accumulated depreciation

Here are some of the most commonly asked questions about accumulated depreciation.

How does accumulated depreciation affect cash flow?

Accumulated depreciation doesn't directly affect cash flow because no money actually leaves your business. However, it provides indirect cash benefits:

- Tax savings: Lower taxable income means smaller tax bills

- Cash preservation: Keep money that would otherwise go to taxes

- Improved cash position: Have more cash available for business operations

What happens to an asset's accumulated depreciation when you sell it?

When you sell an asset, its original cost and accumulated depreciation are removed from your books. For example, a financial statement might note that an asset with a cost of $891 and accumulated amortization of $889 was disposed of. This clears both values from the balance sheet.

Special tax rules may apply. For example, if you sell a certain class of vehicle, Canadian tax law allows you to claim 50% of the CCA that would have been allowed for that fiscal period.

Follow these steps when recording an asset sale:

- Remove accumulated depreciation: Clear the contra asset account

- Calculate book value: Subtract accumulated depreciation from asset cost

- Determine gain or loss: Compare book value to sale price

Do I record accumulated depreciation as a debit or a credit?

Record accumulated depreciation as a credit. As a contra asset, it offsets the debit balance of your assets.

Why it's recorded as a credit:

- Contra asset nature: Offsets the debit balance of asset accounts

- Value reduction: Shows decreasing asset worth over time

- Balance sheet presentation: Appears as a negative against total assets

Is accumulated depreciation a current liability?

No, accumulated depreciation is not a . It's a contra asset that reduces the value of your assets on the balance sheet.

Key differences:

- Current liabilities: Debts due within 12 months

- Accumulated depreciation: Reduces asset value over time

- Repayment: Not required because it's not money owed to anyone

Here's more about current and non-current liabilities.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Start using Xero for free

Access Xero features for 30 days, then decide which plan best suits your business.