Financial statements explained: types and how to read

Learn how financial statements reveal cash flow, profit, and risk so you can spot issues and grow with confidence.

Written by Lena Hanna—Trusted CPA Guidance on Accounting and Tax. Read Lena's full bio

Published Tuesday 14 April 2026

Table of contents

Key takeaways

- Review all four financial statements together monthly or quarterly to get a complete picture of your business health, rather than focusing only on profit, since you can be profitable on paper but still run out of cash if customers haven't paid yet.

- Use your cash flow statement to track actual money moving in and out of your business, as this shows whether you can cover short-term expenses like payroll and bills even when your income statement shows strong profits.

- Compare your financial statements across multiple periods to spot trends like rising costs, declining margins, or seasonal patterns that help you make informed decisions about pricing, expenses, and growth investments.

- Calculate key financial ratios like the current ratio and debt-to-equity ratio from your balance sheet to quickly assess your liquidity and financial stability, which helps you benchmark performance and identify potential problems early.

What is a financial statement?

A financial statement is a formal record that tracks your business's financial activities and performance over a specific period. These documents show what your business owns, owes, earns, and spends.

Financial statements help you:

- assess your business's financial health

- secure funding from lenders and investors

- make informed decisions about growth and operations

Reporting periods typically cover monthly, quarterly, or annual timeframes. Regular reporting helps you spot trends early and adjust your strategy before problems become serious.

Financial statements vs. other business reports

Financial statements differ from other business reports in purpose and format. Knowing the difference helps you choose the right document for each situation:

- Financial statements vs. budgets: Budgets project future spending, while financial statements record what actually happened.

- Financial statements vs. forecasts: Forecasts estimate future performance, while financial statements report historical results.

- Financial statements vs. tax returns: Tax returns report income to the government, while financial statements provide a complete picture of financial health for internal decision-making.

Understanding these differences helps you use the right report for each business decision.

Types of financial statements

Four main types of financial statements give you a complete picture of your business's financial health. Each statement shows a different aspect of your finances:

- Balance sheet: Shows what you own versus what you owe at a specific point in time.

- Income statement: Tracks revenue, expenses, and profit over a period.

- Cash flow statement: Records money moving in and out of your business.

- Statement of changes in equity: Shows how much profit you retain in the business.

Balance sheet

The balance sheet is one of the most important financial statements for understanding your business's worth.

A balance sheet shows what your business owns versus what it owes at a specific point in time. This snapshot helps you understand your net worth and financial stability.

Assets (what you own):

- Liquid assets: Cash and bank accounts

- Physical assets: Inventory, equipment, property, and machinery

- Intangible assets: Intellectual property and patents

Liabilities (what you owe):

- Long-term obligations: Loans and long-term debt

- Short-term obligations: Accounts payable and unpaid expenses

Equity equals your total assets minus total liabilities. This figure helps determine your business's net worth and value.

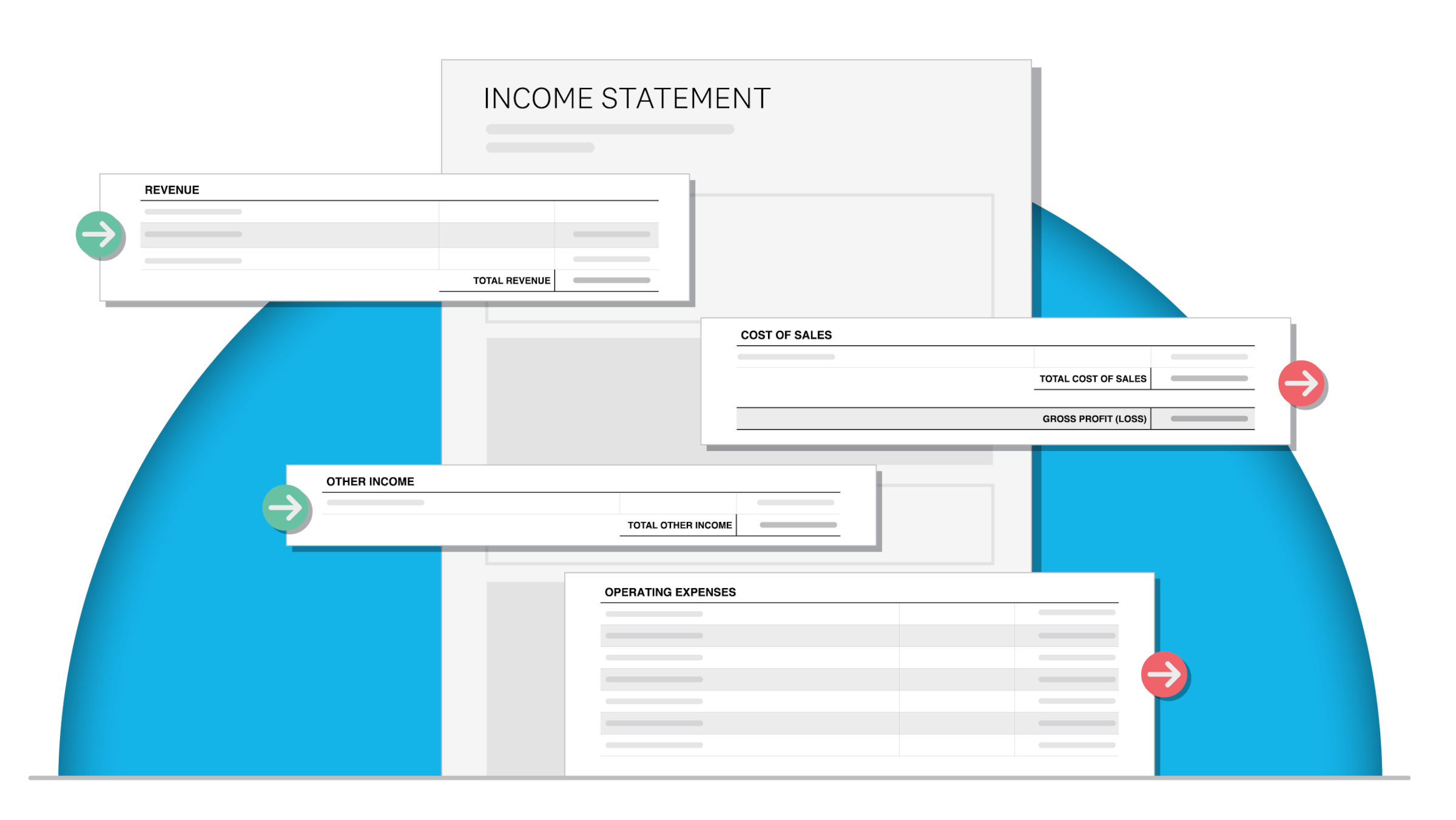

Income statement / profit and loss statement

While the balance sheet shows your position at a moment in time, the income statement reveals your performance over a period.

An income statement (also called a profit and loss statement or P&L) shows whether your business is profitable over a specific period. It compares total revenue against all expenses to calculate your net profit or loss.

Key components of an income statement:

- Revenue: Total money earned from sales

- Cost of sales: Direct costs to produce your product or service

- Operating expenses: Costs like rent, utilities, and salaries

- Net income: Your profit after all expenses

Example: A manufacturing business with $150,000 revenue, $50,000 operating expenses, and $70,000 cost of sales would have $30,000 net income.

Cash flow statement

Profitability doesn't guarantee you have cash available. That's where the cash flow statement comes in.

The cash flow statement tracks how cash moves in and out of your business over time. This statement shows whether you have enough cash to cover short-term expenses like bills and payroll.

It records three types of cash activities:

- Operating activities: Cash from customer sales and daily business operations

- Investing activities: Cash from purchases and sales of assets like machinery

- Financing activities: Cash from loans, investments, or stock sales

Statement of changes in equity

The final core statement tracks what happens to your profits over time.

The statement of changes in equity (also called a retained earnings statement) shows how much profit your business keeps after paying all costs and dividends. This statement tracks changes in your ownership stake over time.

You might retain earnings to:

- Repay debt: Reduce interest costs and improve your balance sheet

- Reinvest in growth: Fund new equipment, hiring, or expansion

- Build reserves: Create a financial cushion for unexpected expenses

Why financial statements are important for small businesses

Financial statements are essential because they turn raw numbers into clear insights about your business's financial health. With them, you can make informed decisions based on real data. These documents help you:

- Make informed decisions based on real data

- Manage cash flow and profitability effectively

- Meet tax and compliance requirements to avoid issues like the penalty of 10% on income you failed to report after an initial omission

- Secure funding from lenders and investors

Supports business growth

Financial statements support your business in several key ways, starting with growth.

Strategic growth requires data. Financial statements give you the numbers you need to make confident decisions. They help you:

- Identify which products or services generate the most revenue

- Spot areas that need improvement

- Guide smart investments with financial data

Improves financial management

Beyond growth, financial statements help you manage day-to-day operations more effectively.

Better financial management starts with accurate statements. When your numbers are right, you can:

- Track cash flow to cover payroll and operating expenses

- Measure profitability and overall financial health

- Prepare for seasonal fluctuations and future needs

Builds stronger external relationships

Your financial statements also matter to people outside your business.

External relationships with lenders, investors, and regulators depend on solid financial reporting. With clear statements, you can:

- Present reliable financial data to attract investors

- Demonstrate repayment ability to secure business loans

- Meet tax and regulatory requirements to avoid major penalties, which can be the greater of $100 or 50% of the amount of understated tax for false statements or omissions

Understanding your financial statements

Focus on the key areas to understand your financial statements. Each statement tells a different part of your business's financial story.

Reading your balance sheet

Start with the balance sheet to understand your business's financial position.

Reading your balance sheet starts with comparing assets to liabilities on a specific date. Here's what to look for:

- Compare totals: Assets should exceed liabilities in a healthy business.

- Calculate equity: Subtract liabilities from assets to find your net worth.

- Check ratios: Use current ratio and debt-to-equity ratio for deeper insights.

Interpreting your income statement

Once you understand your balance sheet, move on to your income statement.

Your income statement shows performance over time, like a month or quarter. Start at the top with total revenue, then work through your expenses.

Net income appears at the bottom of the statement. A positive number means you're profitable. A negative number means expenses exceeded income for that period.

Understanding your cash flow statement

Finally, review your cash flow statement to see your actual liquidity.

Your cash flow statement tracks actual cash moving in and out of your business. The key section to check is cash flow from operating activities.

A positive number here means your core operations bring in more cash than they use. This is a good sign of financial health.

You might be profitable on paper but still struggle to pay bills if cash hasn't arrived yet.

Common mistakes when reading financial statements

Even experienced business owners make these errors when reviewing their numbers. Avoiding them helps you make better decisions.

Confusing profit with cash flow

The most common mistake is confusing two different measures of financial health.

Profit and cash flow measure different things. Your income statement might show a healthy profit, but your bank account tells a different story. This happens when customers owe you money or you've prepaid expenses.

Always check your cash flow statement alongside your income statement to see the full picture.

Ignoring the cash flow statement

Related to the first mistake, many owners overlook a critical document entirely.

Many business owners skip the cash flow statement and focus only on profit. Reviewing all statements gives you a complete picture. Profitable businesses fail every day because they run out of cash to pay bills, staff, or suppliers.

Make reviewing your cash flow statement a regular habit.

Not comparing statements across periods

Another common error is viewing statements in isolation.

A single statement only shows one moment in time. Comparison helps you spot trends like rising costs, declining margins, or seasonal patterns.

Compare your statements month over month and year over year to identify what's improving and what needs attention.

Focusing only on the bottom line

Finally, avoid the temptation to skip straight to the final number.

Net income matters, and so do the details behind it. You might miss warning signs hiding in the details, like growing debt, shrinking margins, or slow-paying customers.

Review each section of your statements, including the details that lead to the final number.

How to create financial statements

Creating financial statements can be straightforward. You can do it manually with spreadsheets or use accounting software for faster, more accurate results. Here's an overview of the steps involved.

1. Gather your financial documents

The first step is collecting everything you need.

Gather all your financial records for the period before you start. Having everything in one place makes the process faster and reduces errors. You'll need:

- Bank and credit card statements

- Records of sales and invoices sent to customers

- Receipts and bills from suppliers

- Payroll records and expense claims

- Loan agreements and asset details

2. Choose your method: manual or automated

Next, decide how you'll create your statements.

Manual method: Entering data into spreadsheets is time-consuming and error-prone. You'll need to build formulas and constantly update information yourself.

Automated method: Accounting software handles most of this work for you. Connect your bank accounts and the software imports transactions automatically. You just categorize them. From there, software like Xero generates your balance sheet, income statement, and cash flow statement in real time.

How to use financial statements to analyze your business

Financial statement analysis helps you make data-driven decisions and spot problems early. Each statement provides specific insights that guide your strategy and keep you tax compliant.

Analyze financial performance with the income statement

Start your analysis with the income statement to understand profitability.

Your income statement reveals how well your business generates profit. Use it to:

- Measure profitability: Compare revenue against expenses to confirm you're making money.

- Control costs: Identify overspending in cost of goods sold and operating expenses.

- Track growth: Compare periods to spot revenue trends and margin improvements.

You can use your income statement to calculate gross profit, operating income and net income. These numbers help you decide if you need to adjust prices or reduce costs to improve profits.

Manage assets and plan for growth with the balance sheet

Next, use your balance sheet to assess your overall financial position.

Your balance sheet reveals your business's financial position at a specific moment. Use it to:

- Assess liquidity: Compare current assets to current liabilities using the current ratio and quick ratio.

- Evaluate solvency: Examine long-term liabilities and equity using the debt-to-equity ratio.

- Track asset management: Review how efficiently inventory, property, and equipment contribute to revenue.

A high debt-to-equity ratio may signal financial risk, while a lower ratio indicates stability.

The cash ratio formula helps you see if you've got enough cash to cover payroll, expenses and loan payments over the next year.

The current ratio formula, unlike the quick ratio, includes your business's inventory value from your balance sheet. Use the current ratio to help you decide about your expenses and cash on hand.

Manage your cash flow with the cash flow statement

Your cash flow statement helps you manage liquidity and avoid cash shortages.

Strong cash flow means your business can pay its bills. Your cash flow statement shows exactly where you stand, so you can improve if needed. Use it to:

- Analyze operating cash flow: Confirm your core activities generate enough cash to sustain the business.

- Judge investment quality: Track capital expenditures on equipment and expansion.

- Monitor financing activities: Review how loans, equity, and dividends affect your cash position.

For more advice on managing your finances and cash flow, visit the Xero guides section. Check your local accounting standards and government resources for programs that support your business.

Analyze growth with the retained earnings statement

Finally, review your retained earnings to understand long-term growth potential.

Your retained earnings statement shows how profits accumulate over time. It demonstrates your business's:

- Growth potential: Growing retained earnings suggest you can reinvest profits without borrowing.

- Financial health: Declining retained earnings may signal you're using profits to cover losses or debts.

Ways to use your financial statements

Get more value from your financial statements with these practical strategies.

Consider the big picture, not just profit

First, avoid the trap of looking at just one number.

Focusing only on net income can leave your business financially vulnerable. You might miss warning signs in other areas.

For a complete picture, review all four statements together: income statement, balance sheet, cash flow statement, and retained earnings statement.

Pay attention to your cash flow

Cash flow deserves special attention in your regular reviews.

Overlooking your cash flow statement can leave you short of cash, even when profitable. Check it regularly to track liquidity and confirm you can cover short-term costs.

Know the difference between revenue and cash

Understanding the timing difference between revenue and cash is essential.

Recorded revenue and cash on hand are different measures. A sale on your books may not have reached your bank account yet.

Track accounts receivable separately so you always know the difference between what you've earned and what you can actually spend.

Analyze trends by comparing your financial statements

Trend analysis reveals patterns you can't see in a single statement.

Compare your statements across several periods to spot patterns in revenue, expenses, and liabilities. Look for trends like rising costs or seasonal dips.

This helps you invest in what's working and address problem areas before they grow.

Get across your financial ratios

Ratios help you benchmark your performance and spot issues quickly.

Financial ratios turn your statement numbers into meaningful benchmarks. They help you measure liquidity, profitability, and overall financial health.

Key ratios to track include the current ratio and quick ratio, which show whether you can cover short-term obligations.

Simplify your financial statements with Xero

Easily create, track, and share financial statements in real time with Xero. Get clear insights into your cash flow and performance so you can make smarter business decisions.

FAQs on financial statements

Here are answers to the most common questions small business owners ask about financial statements.

What's the difference between the income statement and cash flow statement?

These two statements measure different things.

Your income statement shows profitability by comparing revenue to expenses. Your cash flow statement tracks actual cash moving in and out.

The key difference: You can be profitable on paper but still run out of cash if customers haven't paid yet.

Does my small business need all four types of financial statements?

You may not need every statement right away.

Most small businesses need three core statements: balance sheet, income statement, and cash flow statement. These provide the essential insights for managing your finances.

The fourth statement, retained earnings, becomes important when reinvesting profits for growth or debt repayment.

How often should I prepare financial statements?

Regular reporting helps you stay on top of your finances.

Prepare financial statements monthly or quarterly for optimal business management.

- Monthly reporting: Helps you catch problems within 30 days.

- Quarterly reporting: Aligns with tax deadlines and investor expectations.

Regular reporting lets you adjust strategies before small issues become expensive problems.

What are the 5 basic financial statements?

There are five statements in a complete set of financials.

The five basic financial statements are the balance sheet, income statement, cash flow statement, statement of changes in equity, and notes to financial statements. Most small businesses focus on the first three for day-to-day management.

What's the difference between a balance sheet and an income statement?

These two statements serve different purposes.

A balance sheet shows your financial position at a specific moment, listing what you own and owe. An income statement shows performance over a period, tracking revenue and expenses to calculate profit. Together, they tell different parts of your financial story.

Can I create financial statements without accounting software?

You have options for creating your statements.

Yes, you can create financial statements using spreadsheets. However, manual entry is time-consuming and error-prone. Accounting software automates calculations, imports bank transactions, and generates statements in real time, saving you hours of work.

When should I hire an accountant to help with my financial statements?

Professional help can be valuable at certain stages.

Consider hiring an accountant when your business grows beyond basic bookkeeping, you're preparing for a loan or investment, or you need help with tax compliance. An accountant can also set up your systems so you can manage day-to-day finances yourself.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Start using Xero for free

Access Xero features for 30 days, then decide which plan best suits your business.