Is accumulated depreciation an asset or a liability?

Learn if accumulated depreciation is an asset, and how to calculate it for clearer accounts.

Written by Jotika Teli—Certified Public Accountant with 24 years of experience. Read Jotika's full bio

Published Thursday 19 February 2026

Table of contents

Key takeaways

- Recognize that accumulated depreciation is a contra asset account, not an asset or liability, which reduces the book value of your fixed assets on the balance sheet to show their current worth.

- Calculate accumulated depreciation using the straight-line method by dividing the asset's cost minus salvage value by its useful life, then tracking the cumulative total each year.

- Use accumulated depreciation to reduce your taxable income through depreciation expenses, which can lower your tax bill while providing a non-cash way to reflect asset wear and tear.

- Review your asset's useful life and salvage value estimates at least annually to ensure your accumulated depreciation calculations remain accurate for financial reporting.

What is accumulated depreciation?

Accumulated depreciation is the total depreciation recorded for an asset since you purchased it. It represents the portion of an asset's value that has been "used up" over time.

Tracking accumulated depreciation lets you record the true value of your assets on financial statements. This value, known as book value (asset cost minus accumulated depreciation), shows what the asset is realistically worth today. International Financial Reporting Standards (IFRS) refer to this as the "carrying amount," which is calculated by deducting any accumulated depreciation and impairment losses from the asset's recognised cost.

For example:

- Office furniture cost $5,000, with $1,000 depreciation each year. After three years it has depreciated by $3,000, leaving a book value today of $2,000.

- Machinery cost $25,000, with $2,500 depreciation each year. After six years it has depreciated by $15,000, leaving a book value today of $10,000.

Depreciation vs accumulated depreciation

Understanding the difference between these two terms is essential for accurate financial reporting.

Depreciation and accumulated depreciation are related but different concepts.

Depreciation is a recurring expense that shows the decrease in an asset's value over a specific period, like a month or a year.

Accumulated depreciation is the cumulative total of all depreciation expenses recorded for an asset since purchase. It increases each time you record a new depreciation expense.

Is accumulated depreciation an asset or a liability?

This is a common question when learning about balance sheet classifications.

Accumulated depreciation is neither an asset nor a liability. It's classified as a contra asset account.

A contra asset offsets the value of a related asset on the balance sheet. Unlike traditional assets, it carries a negative value.

Liabilities represent amounts your business owes. Accumulated depreciation isn't a debt to be repaid. Instead, it reflects the reduction of an asset's book value over time due to wear and tear.

You record accumulated depreciation alongside your other assets, but its negative value shows how much the asset has depreciated from its original cost. This gives you a more realistic estimate of what the asset is worth today.

How does accumulated depreciation affect financial statements?

Accumulated depreciation appears on multiple financial statements, each serving a different purpose.

Accumulated depreciation on the balance sheet

Accumulated depreciation appears under fixed assets on the balance sheet as a credit balance deducted from the asset's original cost.

While the balance sheet lists the asset's original cost, accumulated depreciation adjusts this value downwards to reflect the asset's current worth. This gives you a clearer picture of your net asset value.

Accumulated depreciation on the income statement

Accumulated depreciation doesn't appear directly on the income statement. Instead, the periodic depreciation expense is recorded there.

Depreciation expense reduces your taxable income each period. As a non-cash expense, it lowers your profits without affecting your actual cash flow.

Accumulated depreciation on the cash flow statement

Depreciation is a non-cash expense, so it doesn't represent money leaving your business.

On the cash flow statement, depreciation is added back to net income. This adjustment reflects that while depreciation reduces profit on paper, no cash actually changed hands.

How to calculate accumulated depreciation

Calculating accumulated depreciation helps you track how much value your assets have lost over time. Here's how to do it using the straight-line depreciation method, the most common approach for small businesses.

The straight line depreciation calculation

This formula distributes the asset's cost evenly across its useful life.

The straight-line depreciation formula is:

Annual depreciation expense = (cost of asset − salvage value) / useful life

Each term means:

- Cost of asset: the original purchase price

- Salvage value: the estimated amount you'll receive when the asset is no longer usable (resale or scrap value)

- Useful life: the estimated number of years the asset will be functional. According to accounting standards, both the useful life and salvage value should be reviewed at least at each financial year-end to ensure estimates remain accurate.

Calculate straight line depreciation

Here's how to calculate accumulated depreciation step by step. In this example, an asset costs $1,000, has a useful life of five years, and a salvage value of $100.

1. Calculate the annual depreciation expense

Using the formula:

($1,000 – $100) ÷ 5 = $180 per year

2. Track accumulated depreciation each year

Create a depreciation schedule showing how accumulated depreciation grows:

- Year 1: $180

- Year 2: $360

- Year 3: $540

- Year 4: $720

- Year 5: $900

3. Calculate book value at any point

Use the formula: Book value = initial cost – accumulated depreciation

After three years, the book value is: $1,000 – $540 = $460

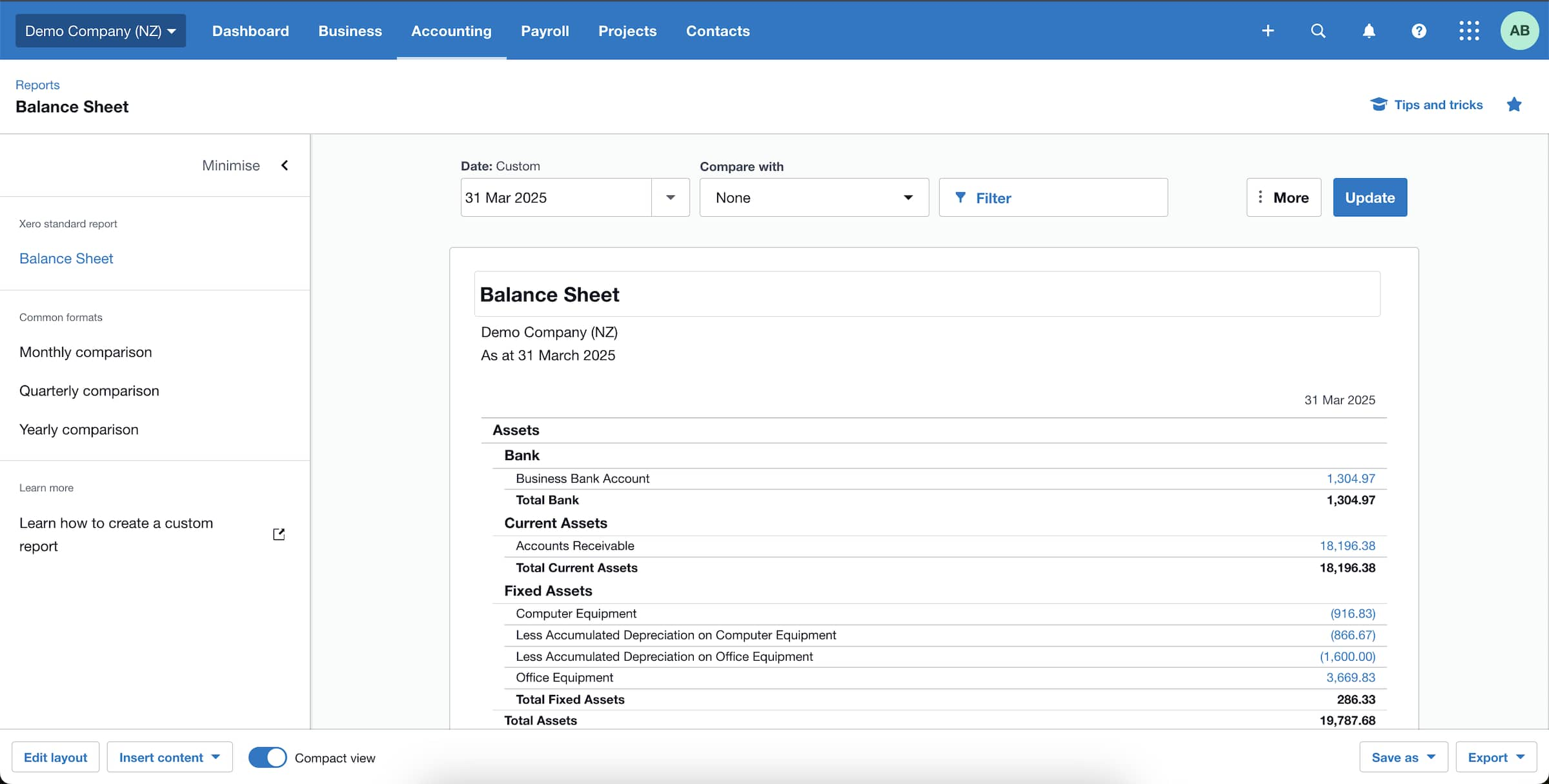

Example: Balance sheet for accumulated depreciation

This example shows how accumulated depreciation changes the net book value of assets and affects overall financial health.

Why understanding accumulated depreciation matters for a business

Tracking accumulated depreciation provides several key benefits for your business:

- Better business planning: track changes in asset values over time to plan replacements, upgrades, and maintenance costs

- Potential tax savings: reduce your taxable income with depreciation charges, lowering your tax bill and keeping more cash in the business

- Easier financing: present accurate book values to improve your chances of attracting investment and getting loan applications approved

Track accumulated depreciation with Xero

Managing depreciation and calculating accumulated depreciation gets complicated as your business grows. Xero simplifies these tasks so you can focus on running your business.

With Xero, you can:

- create depreciation schedules for a clear view of fixed asset values over time

- track assets automatically and manage them in one place

- improve reporting accuracy and generate financial statements with confidence

FAQs on accumulated depreciation

Here are answers to common questions about accumulated depreciation.

How does accumulated depreciation affect cash flow?

Accumulated depreciation doesn't directly affect cash flow because it's a non-cash expense. No money leaves your business when you record it.

However, depreciation reduces your taxable income, which lowers your tax bill. This indirectly improves your cash position by keeping more money in the business.

What happens to an asset's accumulated depreciation when you sell it?

The accumulated depreciation is removed from the balance sheet when you sell or dispose of the asset.

You compare the asset's book value (cost minus accumulated depreciation) with the sale price to determine whether you made a gain or loss on the sale. For example, IFRS guidance shows how selling an asset with a carrying amount of CU2 million for CU3.5 million (minus fees) results in recognising a gain on the disposal in profit or loss.

Do I record accumulated depreciation as a debit or a credit?

Record accumulated depreciation as a credit. It's a contra asset account, which means it offsets the value of the related asset.

Since assets typically have debit balances, accumulated depreciation is credited to reflect the asset's falling value over time.

Is accumulated depreciation a current liability?

No, accumulated depreciation is not a current liability. It's a contra asset account that reduces the value of an asset on the balance sheet.

Current liabilities are short-term debts due within 12 months. Accumulated depreciation isn't an amount you owe or need to repay.

Here's more about current and non-current liabilities

What is the journal entry for accumulated depreciation?

Debit depreciation expense and credit accumulated depreciation. This entry records the periodic depreciation charge.

For example, if monthly depreciation is $150:

- Debit: Depreciation expense $150

- Credit: Accumulated depreciation $150

This increases your expenses (reducing profit) while building up the contra asset that offsets your fixed asset value.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Start using Xero for free

Access Xero features for 30 days, then decide which plan best suits your business.