Solvency vs liquidity: what’s the difference for you?

Learn how solvency vs liquidity impacts your cash flow and long term stability, and what to track to stay in control.

Written by Lena Hanna—Trusted CPA Guidance on Accounting and Tax. Read Lena's full bio

Published Friday 20 February 2026

Table of contents

Key takeaways

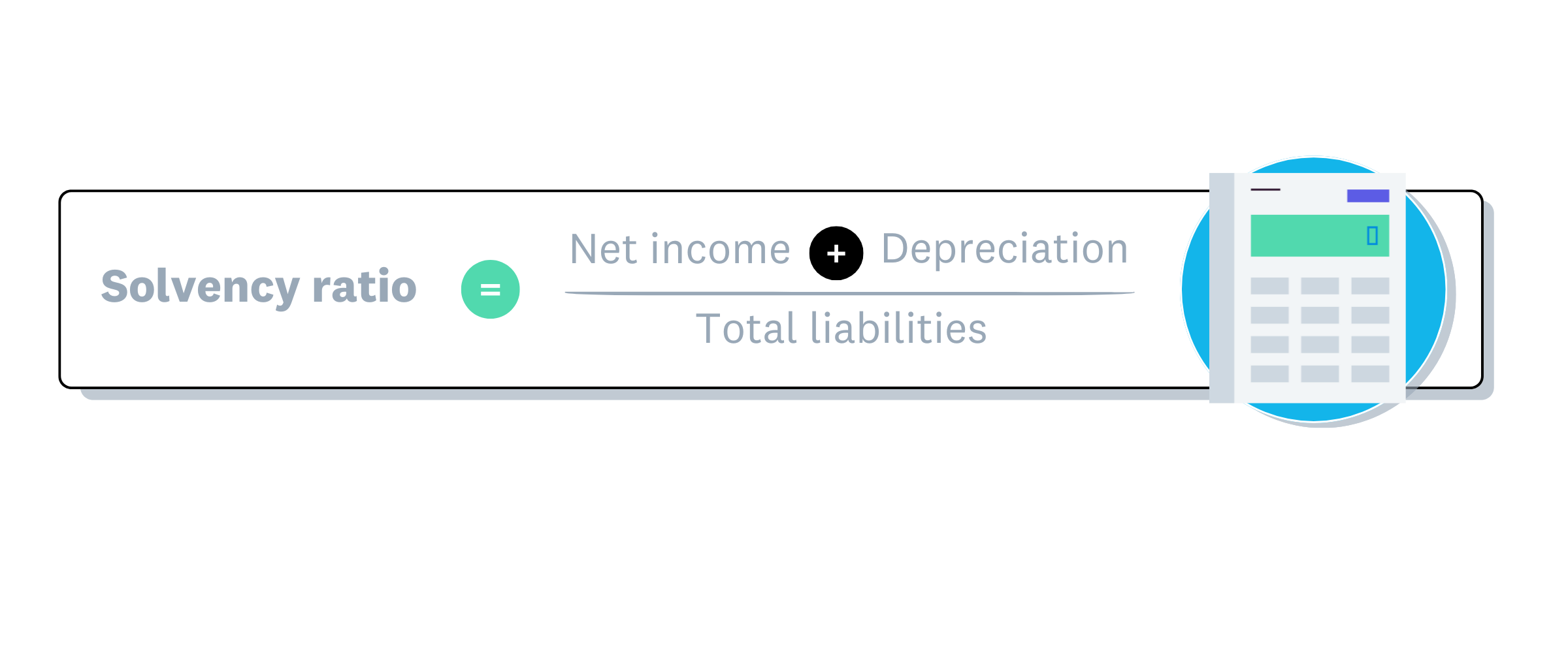

- Calculate your solvency ratio by dividing net income plus depreciation by total liabilities, aiming for 20% or higher to demonstrate your ability to meet long-term debt obligations.

- Monitor your current ratio by dividing current assets by current liabilities, ensuring it stays above 1:1 to maintain sufficient cash flow for short-term bills and expenses.

- Recognise that your business can be solvent but still face cash flow problems if valuable assets like property can't be quickly converted to cash when immediate payments are due.

- Improve liquidity by speeding up customer payments through early payment discounts and maintaining cash reserves, while boosting solvency by attracting investors or renegotiating loan terms.

What does liquidity mean in business?

Liquidity is your business's ability to pay bills and loan repayments in the coming months. It compares current assets (cash, inventory, and receivables) against current liabilities (amounts owed within the year).

Liquidity is commonly expressed as a ratio, such as the current ratio, quick ratio, or cash ratio. A higher ratio means you have more resources available to cover short-term obligations.

Other liquidity ratios

Beyond the current ratio, two other liquidity ratios help assess short-term financial health:

- Quick ratio (acid test): (Cash + receivables + short-term investments) ÷ current liabilities. This measures your ability to pay debts without selling inventory.

- Cash ratio: Cash and cash equivalents ÷ current liabilities. This is the most conservative measure, showing whether you can pay debts with cash on hand.

Learn more in our guide on liquidity ratios.

How liquid are your assets?

Assets vary in how quickly you can convert them to cash. Here's a breakdown from most to least liquid:

- Cash: Physical currency and savings account funds you can withdraw immediately

- Accounts receivable: Invoices owed to you that convert to cash relatively quickly (the shorter your payment terms, the more liquid this asset)

- Inventory: Stock you can sell, though conversion time varies by product type

- Physical assets: Buildings, equipment, and property that may take months to sell

How does liquidity affect business growth?

Strong liquidity supports business growth by helping you:

- Seize opportunities: Launch new products or hire staff when the timing is right

- Handle unexpected costs: Cover emergencies like equipment repairs or property damage

- Maintain operational stability: Avoid scrambling for cheaper suppliers or new lenders during cash crunches

What does solvency mean in business?

Solvency is your business's ability to meet long-term financial commitments. A solvent business has positive net equity, meaning total assets exceed total liabilities.

If your assets are worth more than what you owe, you're solvent. If liabilities exceed assets, you're insolvent and may face bankruptcy risk.

What factors affect your solvency?

To keep your business solvent, focus on these three areas:

- Stay profitable: Generate consistent profits to maintain a healthy balance sheet where assets exceed liabilities

- Manage your debts: Negotiate lower repayments on loans and understand the terms of any collateral-backed financing

- Use assets wisely: Ensure your inventory, equipment, and other assets generate returns that cover your debt obligations

How does solvency affect your business growth?

Maintaining solvency helps you:

- Access funding: Borrow from banks and lenders who trust your ability to repay

- Attract investors: Draw in partners who bring capital and expertise

- Negotiate better terms: Use cash reserves to buy in bulk and lower per-unit costs

- Plan for growth: Keep operations stable while building toward future goals

The main differences between solvency and liquidity

Solvency and liquidity work together to give you a complete picture of financial health. They are just two of many metrics available. Research identifies as many as 50 financial ratios across various categories. A business can be solvent (assets exceed liabilities) but still face liquidity problems if those assets can't be converted to cash quickly enough to pay immediate bills.

Solvency takes a long-term view, while liquidity focuses on the short term. This table outlines the key differences.

Table of the difference between solvency and liquidity

How to measure solvency and liquidity in your business

Calculating your solvency and liquidity ratios helps you understand where your business stands financially. Here's how to measure each one.

Solvency ratio formula

Use this formula to calculate your solvency ratio.

Solvency ratio formula

Solvency ratio calculation example

Martha owns a cafe with these figures:

- Net income: $50,000

- Depreciation: $10,000 (the decrease in asset value from normal wear and tear)

- Total liabilities: $300,000

Formula: (Net income + depreciation) ÷ total liabilities

Calculation: ($50,000 + $10,000) ÷ $300,000 = 20%

A solvency ratio of 20% or above is generally considered healthy. Experts note that a company is financially strong if its ratio exceeds this threshold. Martha's cafe has a good chance of meeting its long-term debt obligations.

Liquidity ratio formula

There are several liquidity ratios, including the cash ratio, quick ratio, and working capital ratio. The working capital ratio is a useful long-term measure of liquidity.

Here's the formula for the working capital ratio:

Liquidity ratio calculation example

Sadiq runs a sports shop with these figures:

- Current assets: $120,000

- Current liabilities: $80,000

Formula: Current assets ÷ current liabilities

Calculation: $120,000 ÷ $80,000 = 1.5

A current ratio above 1:1 indicates good liquidity. Accounting guidance considers any ratio greater than 1:1 reasonable. Sadiq's shop can likely meet its short-term financial commitments.

Why solvency and liquidity matter for your small business

Understanding both metrics helps you make better decisions for daily operations and long-term planning.

Why solvency matters:

- Strong solvency: You have a financially stable business, can manage risks like unpaid invoices, and have resources to grow

- Low solvency: Improving solvency helps you pay debts more easily and reduces bankruptcy risk

Why liquidity matters:

- Strong liquidity: You have cash to pay staff, suppliers, and handle unexpected costs

- Low liquidity: Improving liquidity helps you cover immediate expenses, complementing your overall solvency

Tips to improve your financial solvency and liquidity

Here are practical ways to improve your financial health.

To improve solvency:

- Attract new investors to increase equity

- Renegotiate, refinance, or consolidate existing loans

- Restructure operations to reduce ongoing costs

To improve liquidity:

- Measure cash flow regularly and align payment schedules accordingly

- Benchmark your ratios against industry standards

- Make invoices easier for customers to pay

- Maintain a cash reserve for unexpected expenses

Use Xero to track your solvency and liquidity

Xero accounting software gives you real-time visibility into your numbers. Track daily spending, monitor cash flow, and generate financial reports that show your solvency and liquidity at a glance.

Get one month free and see how Xero helps you stay on top of your financial health.

FAQs on solvency and liquidity

Here are answers to common questions small business owners ask about solvency and liquidity.

What does it mean to provide liquidity?

Providing liquidity means ensuring your business has enough cash to cover short-term bills and obligations. You can improve liquidity by speeding up cash flow, such as offering early payment discounts to customers.

Can my business have good solvency but poor liquidity?

Yes. Your business can have strong solvency from valuable fixed assets like land and buildings, while still needing to improve liquidity by increasing cash in the bank. It can therefore pay its long-term debts.

Is solvency good or bad?

Solvency is positive. It means your business can meet long-term financial obligations because your assets exceed your liabilities. Higher solvency typically means lower risk for lenders and investors.

What is a good solvency ratio for my small business?

The ideal ratio varies by industry. A ratio of 20% or more indicates you can meet your long-term financial obligations.

What is an example of solvency?

A business with $500,000 in total assets and $300,000 in total liabilities is solvent because assets exceed liabilities by $200,000. This positive net equity means the business can meet its long-term financial obligations.

Start using Xero for free

Access Xero features for 30 days, then decide which plan best suits your business.