What is working capital? Formula and how to calculate

Learn how working capital keeps cash flowing, funds daily costs, and supports growth.

Written by Jotika Teli—Certified Public Accountant with 24 years of experience. Read Jotika's full bio

Published Thursday 2 April 2026

Table of contents

Key takeaways

- Calculate your working capital by subtracting current liabilities from current assets to determine if you have enough short-term resources to cover upcoming expenses and invest in growth.

- Monitor your working capital regularly and compare it to previous periods to spot trends, as a declining number over several months may indicate growing financial pressure even if the current figure is positive.

- Improve your working capital by speeding up invoice collection, negotiating longer payment terms with suppliers, and managing inventory levels to avoid tying up excess cash in unsold goods.

- Recognise that ideal working capital varies by industry, with service businesses typically needing lower ratios than retail or manufacturing companies that hold significant inventory.

What is working capital?

Working capital is the difference between your business's current assets and current liabilities. It shows whether you have enough short-term resources to cover your upcoming expenses.

A positive number means you can pay your bills and invest in growth. A negative number signals potential cash flow problems ahead.

Current assets and liabilities

- Current assets: assets you can convert to cash within a year, like cash, funds in bank accounts, accounts receivable, inventory, prepaid expenses, short-term investments, and tax refunds

- Current liabilities: amounts your business must pay within a year, such as accounts payable, loan or credit interest and payments, deferred revenue, and accrued expenses like wages and bank fees

The importance of working capital in business

Working capital reveals your business's short-term financial health. It helps you answer critical questions about your operations and growth potential.

Here's why working capital matters:

- Operational stability: shows whether you can cover day-to-day expenses

- Market resilience: indicates your ability to handle seasonal dips or unexpected costs

- Growth potential: reveals if you have funds to reinvest in your business

- Funding readiness: lenders and investors use it to assess your financial stability

Positive vs negative working capital

Your working capital result tells you where your business stands financially. Here's what each scenario means:

- Positive working capital: your current assets exceed your liabilities, so you can pay bills and reinvest surplus funds into growth

- Negative working capital: your liabilities exceed your assets, which may signal trouble meeting debts without borrowing or raising funds

- Neutral working capital: your assets and liabilities are roughly equal, which works if sales are strong but leaves little buffer for unexpected costs

Extremely high working capital isn't always ideal, as it may suggest your business isn't reinvesting enough in innovation or growth. For example, some service industries show very high ratios, which can indicate potential capital inefficiency alongside conservative risk management. Learn more about working capital ratios by industry.

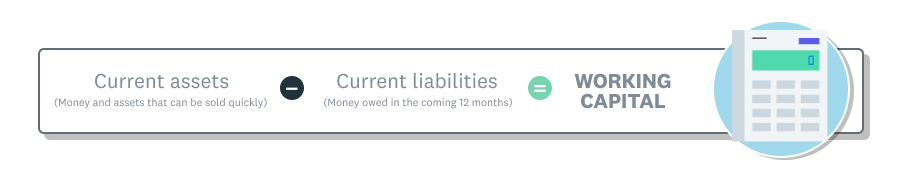

How to calculate working capital

Calculate working capital by subtracting your current liabilities from your current assets. You'll need figures from your balance sheet.

Working capital = Current assets - Current liabilities

Accounting software like Xero makes this easy by pulling figures directly from your balance sheet and financial reports.

The working capital formula

Here's how the formula works in practice.

A working capital formula example

Here's how a retail florist might calculate their working capital:

- Add up current assets for the next 12 months: $100,000

- Add up current liabilities for the next 12 months: $75,000

- Subtract liabilities from assets: $100,000 - $75,000 = $25,000 in positive working capital

This florist has enough short-term resources to cover upcoming expenses and reinvest in the business.

Working capital vs working capital ratio

Understanding the difference between these two metrics helps you analyse your finances more effectively.

Working capital and the working capital ratio measure the same components differently.

- Working capital is a dollar amount (assets minus liabilities)

- Working capital ratio is a proportion (assets divided by liabilities)

Each serves a different purpose. Working capital shows your actual surplus or shortfall. The ratio shows how many times your assets can cover your liabilities.

Understanding your working capital

Once you've calculated your working capital, you need to know what the number means for your business. Your result indicates whether you have enough short-term resources to operate smoothly and invest in growth.

Here's how to interpret your working capital:

- Positive result (above zero): you have more assets than liabilities, giving you a buffer to cover expenses and reinvest in your business

- Negative result (below zero): your liabilities exceed your assets, which may signal difficulty paying bills without borrowing

- Result near zero: your assets and liabilities are roughly balanced, leaving little room for unexpected costs or growth investments

The ideal working capital amount varies by industry and business model. For example, asset-light service businesses like transportation have lower ratios (1.0–3.1), while retail and food processing require greater working capital (1.3–31.5) to manage inventory.

Compare your working capital to previous periods to spot trends. A declining number over several months may indicate growing financial pressure, even if the current figure is still positive.

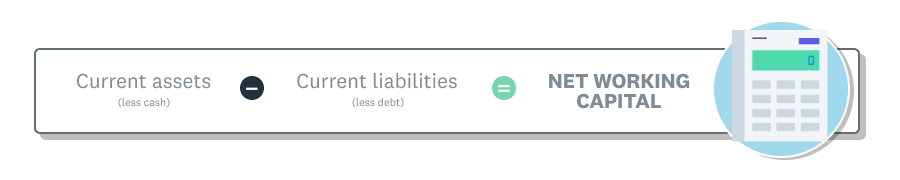

What is net working capital?

Net working capital (also called operating working capital) measures your business's operational efficiency by excluding cash and debt from the standard working capital calculation.

While often used interchangeably with working capital, net working capital focuses specifically on how well your daily operations convert resources into revenue.

Net working capital differs from standard working capital in two key ways:

- Excludes cash: removes cash from the asset side of the equation

- Excludes debt: removes short-term debt from the liability side

This calculation is especially useful for:

- Long-term planning: assessing operational efficiency over time

- Growing businesses: evaluating how well you convert resources into revenue

- Low-margin industries: retail, manufacturing, and distribution where efficiency drives profitability

Use this formula to calculate net working capital:

The net working capital formula

Consider the florist example again. Suppose their current assets include a cash amount of $20,000, and their current liabilities include loan debts of $10,000. The new formula for their net working capital is $80,000 ($100,000 - $20,000) - $65,000 ($75,000 - $10,000) = $15,000.

Working capital vs cash flow: what's the difference?

Working capital and cash flow both measure financial health, but they answer different questions.

- Working capital shows how much money remains after covering upcoming costs (a snapshot of your short-term financial position)

- Cash flow shows how money moves in and out of your business over time (a view of your actual cash on hand)

You can have positive working capital but still face cash flow problems if payments are delayed. Tracking both gives you a complete picture of your financial health.

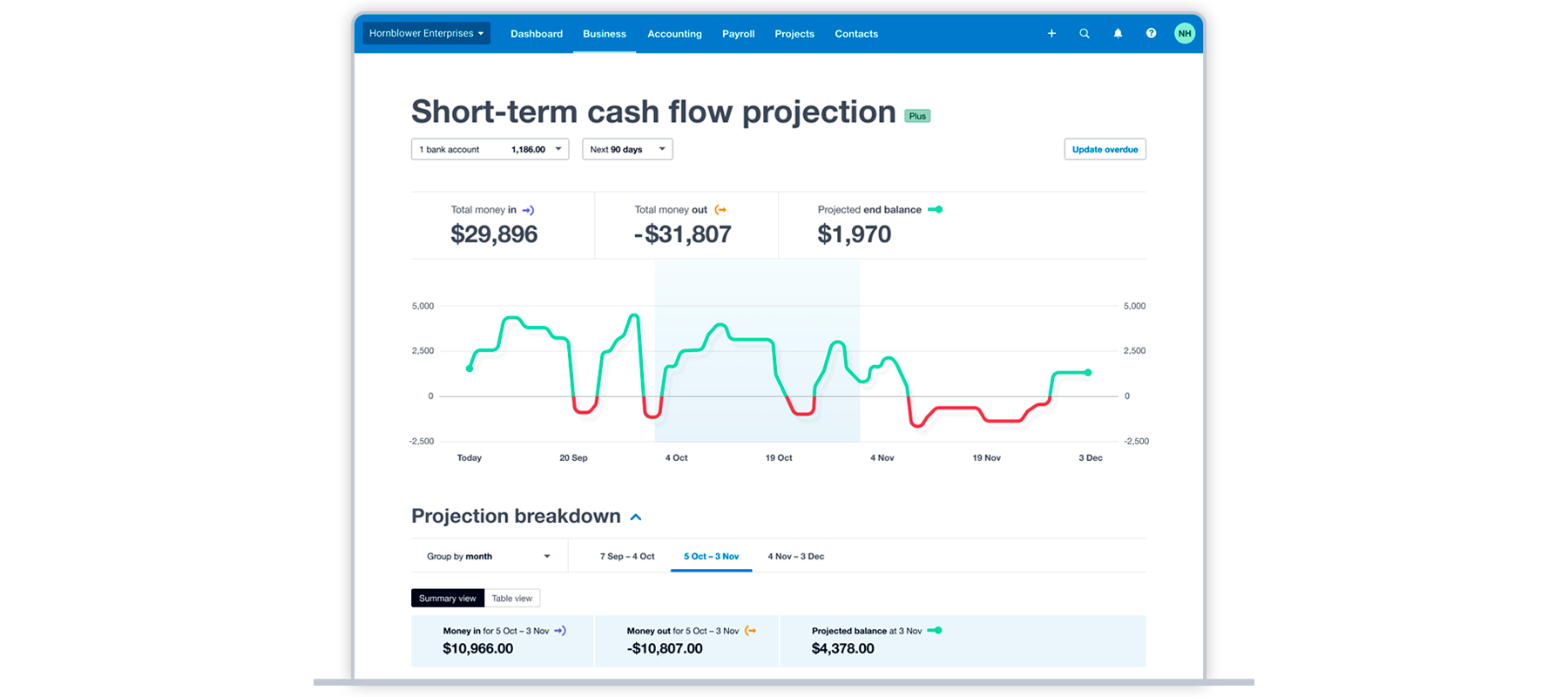

Here's an example of a short-term cash flow projection in Xero. This shows figures for the total money in and out for the next 90 days. It doesn't include liquid assets or show the whole picture of the business's health and adaptability.

Working capital examples in different businesses

Working capital needs vary by industry because of different operating cycles, cash flow patterns, and asset structures. Here's how working capital works across different business types.

Working capital in construction and manufacturing

Construction projects and manufacturing businesses often have irregular cash flow due to long project timelines and payment schedules. Working capital funds upfront material, subcontractor, and labour costs that the business often can't recover until a project is finished.

For example, a small business manufacturer of building materials wants to know how the business will hold up in an uncertain market.

- Add up current assets: cash ($100,000) + accounts receivable ($200,000) + inventory ($300,000) = $600,000

- Add up current liabilities: accounts payable ($150,000) + short-term loans ($100,000) + accrued expenses ($50,000) = $300,000

- Apply the working capital formula by subtracting current liabilities from current assets: $600,000 - $300,000 = $300,000. The business has $300,000 in positive working capital, which means it has enough assets to cover its liabilities for now.

Working capital in service businesses

Businesses providing services, like consultancies or agencies, don't hold inventory so they typically need less working capital than product-based industries. They may have higher accounts receivable (because they invoice clients) and will still need enough working capital to cover payroll, office expenses, and project costs.

Working capital in retail

Retail and wholesale businesses often hold significant inventory, requiring plenty of working capital to meet customer demand. For instance, a Yale School of Management analysis of Tiffany & Co. found its working capital was 65.6% of 2020 revenues, largely due to its vast inventory.

How to manage your working capital

Managing your working capital directly affects your ability to pay bills, invest in growth, and weather unexpected costs. Here are practical strategies to keep your working capital healthy.

Manage your inventory

Inventory ties up cash that could be used elsewhere. In fact, among S&P 1500 companies that saw their cash conversion cycle deteriorate, 87% experienced an increase in Days Inventory Outstanding (DIO).

- Balance stock levels: keep enough inventory to meet demand without tying up excess cash in unsold goods

- Speed up turnover: offer promotions or discounts on slow-moving stock to free up funds

- Automate tracking: use inventory management software to monitor stock in real time, forecast demand, and automate reordering

Control your expenses

Reducing expenses improves your working capital without increasing revenue. Here's where to focus:

- Review spending regularly: identify costs you can cut without affecting quality or operations

- Prioritise growth investments: focus spending on activities that directly support business growth

- Streamline processes: use lean practices to reduce waste and improve efficiency

Monitor your cash flow

Regular cash flow monitoring helps you spot problems before they affect your working capital:

- Track inflows and outflows: review your cash position weekly or monthly to anticipate shortages or surpluses

- Build a reserve fund: set aside a portion of profits to cover lean periods or unexpected expenses

Invest in software tools to streamline your operations

Accounting software helps you manage working capital by automating routine tasks and providing real-time visibility. Here's how Xero supports better working capital management:

- Automated invoicing: generate and send invoices automatically, track payment status, and follow up on overdue accounts to reduce payment delays

- Payment management: monitor customer payments, send automatic reminders, and offer multiple payment options to speed up collections

- Expense tracking: track expenses in real time to control costs and maintain visibility into your cash position

- Anywhere access: manage your finances from any device with an internet connection so you can respond to cash flow issues quickly

These features give you more control over your financial position, helping you maintain healthy working capital and grow from a stable base.

Improve your working capital with Xero

Xero accounting software helps you manage your working capital by tracking your assets and liabilities and streamlining invoicing and payments.

With Xero, you can:

- automate invoicing and payment collection

- track inventory levels in real time

- access real-time financial insights and reports

- monitor and categorise expenses easily

- forecast your cash flow with confidence

Ready to take control of your working capital? Get one month free and see how Xero helps you manage your finances with confidence.

FAQs on working capital

Here are answers to common questions about working capital.

What is a good working capital ratio for small businesses?

A good working capital ratio for small businesses is typically between 1.2–2.0, a range seen across many established industries with predictable cash flows, including manufacturing (1.52) and retail (1.57). A ratio below 1.0 means your liabilities exceed your assets, which could signal trouble.

The ideal ratio varies by industry. Service businesses generally need lower ratios than retailers who hold significant inventory.

How can I improve working capital ratio?

Here are ways to improve your working capital ratio:

- Speed up invoicing: send invoices immediately to reduce payment turnaround time

- Negotiate payment terms: ask suppliers for longer payment windows to slow cash outflows

- Offer early payment discounts: encourage customers to pay sooner with small incentives. As a Yale School of Management paper notes, a common early payment discount (2% off if paid within 10 days, otherwise due in 30 days) has an effective annual rate of over 36%, making it a powerful tool

- Cut non-essential spending: reduce overheads to boost your asset position

What happens if my working capital ratio is too low?

A low working capital ratio means your business may struggle to cover short-term debts. If this continues, it could lead to insolvency.

If your ratio falls below 1.0, consider speeding up collections, negotiating better supplier terms, or reducing non-essential expenses.

What is a working capital loan?

A working capital loan is short-term financing used to cover day-to-day operating expenses when your business faces a cash shortfall.

Consider this option after trying other strategies to improve working capital first. Before taking on new debt, seek advice from a financial adviser.

Is working capital the same as liquidity?

No, they measure different things.

- Liquidity shows how easily you can convert assets to cash to cover upcoming costs

- Working capital shows how much remains after covering those costs

Both metrics help you understand short-term financial health, but liquidity focuses on access to cash while working capital focuses on your overall surplus or shortfall.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Start using Xero for free

Access Xero features for 30 days, then decide which plan best suits your business.