Basis of accounting

Learn what a basis of accounting is, how cash and accrual differ, and which one fits your Canadian business.

Published Thursday 23 July 2026

Table of contents

Key takeaways

Basis of accounting determines the point at which you recognize transactions.

- Your basis of accounting is the method that decides when you record a transaction in your books.

- Cash basis records money when it changes hands, while accrual basis records revenue when it's earned and expenses when they're incurred.

- Accrual basis gives a more accurate picture of profit over time and is required under generally accepted accounting principles (GAAP).

- In Canada, most self-employment income must be reported on the accrual method, though farmers, fishers, and self-employed commission agents can use either method.

What is a basis of accounting?

Your basis of accounting is the method that decides when you record a transaction in your books. It sets the timing for when income and expenses show up in your financial records.

That timing shapes how your profit and cash position look on paper. The two main methods are cash basis and accrual basis, and the one you pick affects everything from your day-to-day bookkeeping to how you report to the Canada Revenue Agency (CRA).

Cash basis vs accrual basis accounting

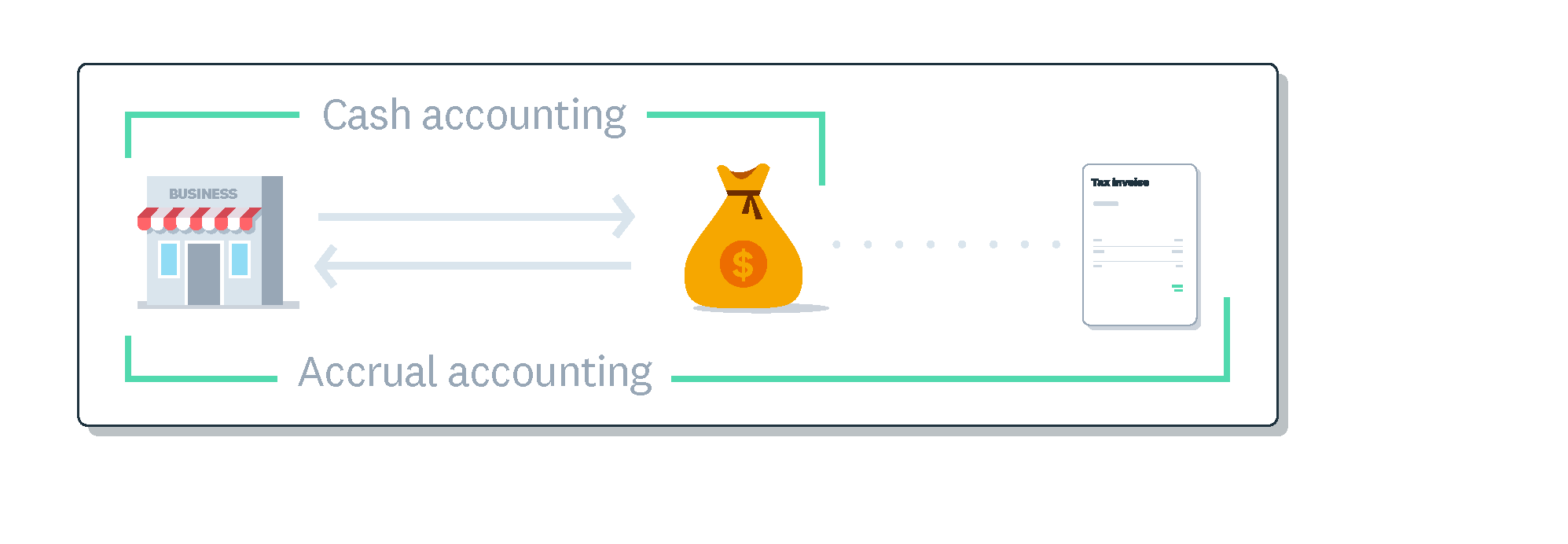

The core difference between the two methods comes down to timing. Cash basis follows the money, while accrual basis follows the activity behind it.

Here's how each method handles the same transaction:

- Cash basis: records income and expenses when money actually changes hands

- Accrual basis: records revenue when you earn it and expenses when you incur them, regardless of when cash moves

Say you invoice a client in March but they pay in April. On cash basis, you record the income in April when the payment lands. On accrual basis, you record it in March when you earned it. The sections below break down each method and when it works best.

What is cash basis accounting?

Cash basis accounting records income and expenses only when money enters or leaves your bank account. It mirrors your bank activity, which makes it simple to follow.

Because it tracks real cash movement, this method suits businesses that want a clear, short-term view of their liquidity. It's often a good fit in these situations:

- You run a small business with straightforward finances

- You want bookkeeping that closely matches your bank statements

- You need a quick read on the cash you have on hand

The trade-off is accuracy over time. Cash basis ignores money owed to you (receivables) and money you owe (payables), so it can distort your true profit. To learn the fundamentals, read our glossary term on cash basis accounting.

What is accrual basis accounting?

Accrual basis accounting records revenue when you earn it and expenses when you incur them, even if the cash hasn't moved yet. It follows two core ideas: the revenue recognition principle and the matching principle.

The revenue recognition principle records income when it's earned, and the matching principle pairs expenses with the revenue they helped generate. Together they give a longer-term, more accurate picture of profitability, which is why accrual basis is required under GAAP. It pairs well with double-entry bookkeeping.

The method asks more of you in return. Keep these trade-offs in mind:

- Track more detail: you'll record receivables and payables, not just cash

- Maintain more records: the added accuracy needs more bookkeeping

- Watch your cash: strong profit on paper can mask a short-term cash shortfall

To go deeper on the concept, see our glossary term on accrual accounting.

What is the hybrid (modified) basis of accounting?

The hybrid basis, also called the modified basis, mixes cash and accrual methods for different types of transactions. You might record some items on cash basis and others on accrual basis within the same set of books.

This approach can get legally complex, and the rules around it aren't always simple to apply. Use it only with an accountant or tax professional who can confirm it's set up correctly for your situation.

Which basis of accounting should you choose?

The right method depends on how complex your business is and what you need to see in your numbers. Your choice also has to work within CRA rules, which we cover in the next section.

Weigh these points as you decide:

- Choose cash basis if your finances are simple and you want a clear view of available cash

- Choose accrual basis if you carry receivables or payables and need an accurate profit picture

- Consider your growth plans, since a scaling business often outgrows cash basis

Whichever you pick, staying on top of the money coming in and going out matters. Our guide to managing cash flow and our small business accounting guide can help you build good habits early.

How your basis of accounting affects tax filing in Canada

The method you use shapes how you report income to the CRA, and the rules aren't the same for everyone. Your business type decides which methods you're allowed to use.

According to CRA guidance on accounting methods, farmers, fishers, and self-employed commission agents can use either the cash method or the accrual method. All other self-employment income must be reported using the accrual method.

Switching methods comes with its own steps:

- Moving from accrual to cash: use the cash method on your next return with a statement of adjustments

- Moving from cash to accrual: get written permission from your tax services office before your filing date

One more point holds true even if you use the cash method: you must still use the accrual method for goods and services tax, harmonized sales tax, and Quebec sales tax (GST/HST/QST) purposes.

Simplify your accounting with Xero

Xero brings your finances into one place and handles routine tasks like bank reconciliation, so you spend less time on manual admin. Whether you track your books on cash or accrual basis, you get real-time insight into how your business is doing.

See how it fits your business and get your first month free.

FAQs on basis of accounting

Here are answers to some frequently asked questions about basis of accounting to help you decide what's right for your business.

What's the difference between cash and accrual basis accounting?

Cash basis records income and expenses when money changes hands. Accrual basis records revenue when it's earned and expenses when they're incurred, regardless of when cash moves.

Which basis should a small business use?

Cash basis suits simpler businesses that want a clear view of available cash. Accrual basis suits businesses with receivables or payables that need an accurate profit picture over time.

Can you switch your basis of accounting?

Yes, but the CRA sets the process. To move from the cash method to the accrual method, you need written permission from your tax services office before your filing date.

What is the hybrid or modified basis of accounting?

It's a method that combines cash and accrual for different types of transactions. Because it can get legally complex, use it only with an accountant or tax professional.

Which method does the CRA require?

The CRA requires the accrual method for most self-employment income. Farmers, fishers, and self-employed commission agents can use either the cash or accrual method.

Related terms

Learn more about basis of accounting

Handy resources

Advisor directory

You can search for experts in our advisor directory

How to do bookkeeping

Learn about data entry, bank rec, reporting and tax prep in our guide to doing bookkeeping.

Online accounting with Xero

Automate your accounting in the cloud

Disclaimer

This glossary is for small business owners. The definitions are written with their requirements in mind. More detailed definitions can be found in accounting textbooks or from an accounting professional. Xero does not provide accounting, tax, business or legal advice.