NOPAT: definition, formula and how to calculate it

Learn how NOPAT shows true operating profit after tax so you can assess performance and plan with confidence.

Written by Kari Brummond—Content Writer, Accountant, IRS Enrolled Agent. Read Kari's full bio

Published Friday 20 February 2026

Table of contents

Key takeaways

- Calculate NOPAT using the formula: Operating Profit × (1 − Tax Rate) to measure your business's true operational performance after taxes but before interest expenses.

- Use NOPAT to compare businesses fairly across different debt levels and capital structures, as it reveals core operational profitability independent of financing decisions.

- Apply NOPAT to calculate Economic Value Added (EVA) by subtracting your cost of capital from NOPAT, which shows how much value your invested capital actually generates.

- Track your effective tax rate by dividing income tax paid by operating profit, as this percentage directly impacts your NOPAT calculation and business performance analysis.

What is NOPAT?

Net Operating Profit After Tax (NOPAT) measures how much profit your business earns from its core operations, after tax but before interest. Unlike net income, NOPAT excludes non-operating income (such as investment gains) and interest expenses on debt.

NOPAT focuses purely on operational performance. Here's what it includes and excludes:

- Includes: revenue and expenses from core business operations

- Includes: tax obligations on operating income

- Excludes: interest expenses on loans, credit cards, or other debts

- Excludes: non-operating income such as investment gains or rental income

This focus makes NOPAT useful for calculating the return on invested capital (ROIC) in a business, a key metric for which investors typically set the minimum ROIC between 10%–15%.

Why is NOPAT important?

NOPAT reveals how profitably a business operates, regardless of its debt level. This makes it valuable for three key purposes:

- Comparing businesses: evaluate companies across different regions, industries, or capital structures on equal footing

- Assessing operational efficiency: isolate core business performance from financing decisions

- Calculating returns: determine how much value invested capital generates

Reveals true business performance

NOPAT isolates operational performance by excluding financing costs while accounting for taxes. This shows how the business performs independent of its debt obligations.

This clear view is especially useful when evaluating businesses with complex financial structures or multiple investors. By focusing on operational profits, you can identify areas to improve and make informed decisions about long-term growth.

Helps to standardise comparisons

NOPAT helps you compare companies with different debt levels or tax situations on equal terms. A business with high debt may show low net profits, but NOPAT reveals the health of its core operations. For example, a company with a heavy debt load could report a net income of $0, but after removing interest expenses, it may actually have a significant after-tax operating profit.

Example: You're comparing two businesses to buy:

- Company A: $100,000 net profit

- Company B: $80,000 net profit, but high debt

If you exclude Company B's interest payments, its operational profit jumps to $120,000. NOPAT highlights this potential by showing what the business could earn if restructured or debt-free.

NOPAT also helps when comparing businesses in different tax jurisdictions, showing exactly how local tax rates affect operational profits.

Improved decision-making

NOPAT helps calculate Economic Value Added (EVA), which shows how well invested capital is performing. EVA accounts for both your debt and shareholder equity.

EVA formula: NOPAT − (Total Invested Capital × Cost of Capital)

Example calculation:

- NOPAT: $50,000

- Loans: $100,000 at 6% interest

- Cash invested: $100,000

- Total invested capital: $200,000 at 3% average cost

- EVA: $50,000 − $6,000 = $44,000

This means your $200,000 invested in the business generates $44,000 in value annually. EVA is especially useful for businesses with multiple shareholders, helping guide decisions about future investments or loans.

For more detail, see these EVA calculation examples.

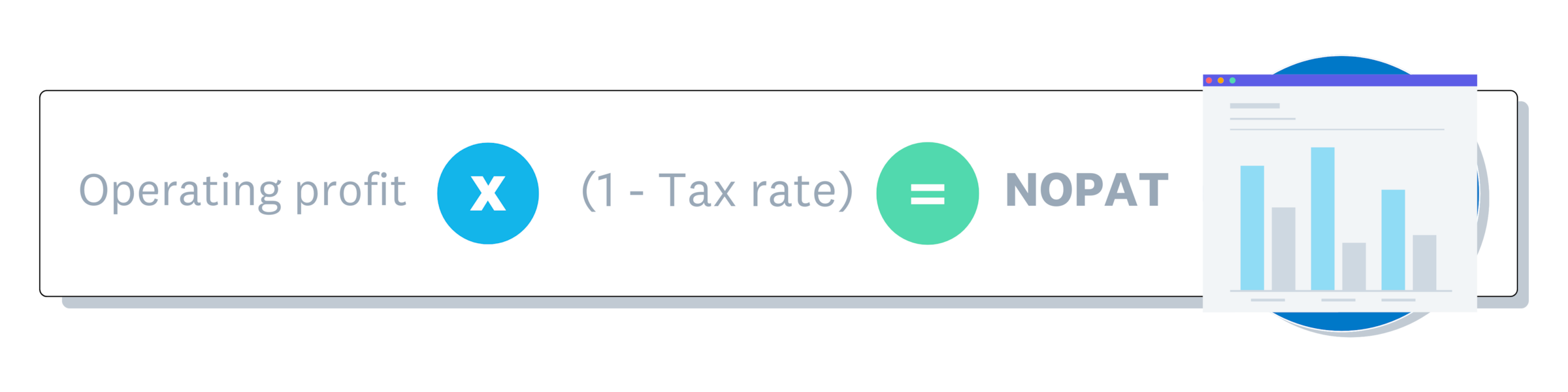

NOPAT formula explained

The NOPAT formula calculates after-tax operating profit in one step:

NOPAT = Operating Profit × (1 − Tax Rate)

Breaking it down:

- Operating profit: revenue minus operating expenses (including depreciation and amortisation), before taxes or interest

- Tax rate: your effective tax rate as a decimal

- (1 − Tax rate): the portion of profit you keep after taxes

Example: With $100,000 operating profit and a 20% tax rate:

$100,000 × (1 − 0.20) = $100,000 × 0.80 = $80,000 NOPAT

Note: Operating profit differs slightly from EBIT (Earnings Before Interest and Tax). EBIT includes all income sources, while operating profit includes only income from core business activities.

How to calculate NOPAT

Apply the formula using your operating profit and tax rate. Here's how to work through each step.

1. Determine operating profit

Operating profit is your earnings from core business activities before taxes and interest. Calculate it by subtracting operating expenses from gross profit.

Operating Profit = Gross Profit − Operating Expenses

Gross profit equals revenue minus cost of goods sold. Operating expenses include wages, rent, utilities, and depreciation.

2. Find the tax rate

Your effective tax rate is the actual percentage of operating profit paid in taxes.

Effective Tax Rate = Income Tax Paid ÷ Operating Profit

Example: $20,000 tax on $100,000 operating profit = 20% effective rate.

If you expect higher earnings this year, recalculate for potential rate changes in higher tax brackets.

3. Apply the formula

Apply the formula using your operating profit and tax rate.

Example calculation:

- Operating profit: $50,000

- Tax rate: 25%

- Calculation: $50,000 × (1 − 0.25) = $50,000 × 0.75 = $37,500

Your business's core operations earn $37,500 per year after tax, before interest.

NOPAT vs net income

NOPAT and net income differ in what they include. Net income captures everything; NOPAT focuses only on core operations.

Net income includes:

- all revenue sources (operating and non-operating)

- all expenses (operating, interest, depreciation, amortisation)

- all tax obligations

NOPAT excludes:

- interest expenses on debt

- non-operating income (rental income, investment gains)

- non-operating expenses

Example: A bakery shows $100,000 in net income. It earns $12,000 from renting parking space to a food truck and pays $8,000 in loan interest (learn about calculating interest payments). To calculate NOPAT, exclude both: $100,000 − $12,000 + $8,000 = $96,000 in NOPAT.

If a business has no debt and no non-operating income, NOPAT and net income are the same.

NOPAT vs EBIT

While they sound similar, NOPAT and EBIT (Earnings Before Interest and Tax) are not the same. The main difference is that EBIT is a pre-tax measure, while NOPAT is post-tax.

EBIT shows a company's total earnings before it pays interest or tax. It can sometimes include income from activities outside of core operations, like investment gains. NOPAT starts with operating profit and subtracts taxes to show you what the core business earns after its tax bill.

- Use EBIT when you want to compare companies before the effects of taxes or see their total earning power.

- Use NOPAT when you need to evaluate the efficiency of core operations or calculate return on invested capital.

NOPAT vs EBITDA

NOPAT and EBITDA (Earnings Before Interest, Tax, Depreciation, and Amortisation) both measure profitability, but they do it in different ways. EBITDA is often used as a proxy for cash flow because it adds back non-cash expenses like depreciation and amortisation.

NOPAT, however, includes these expenses. It gives you a truer sense of operational profit because it accounts for the cost of using assets (depreciation) and the company's tax burden. EBITDA is a pre-tax measure, while NOPAT is post-tax.

- Use EBITDA for analysing a company's ability to generate cash.

- Use NOPAT for measuring true operational profit and calculating returns on investment.

Operating profit vs NOPAT

Operating profit is pre-tax; NOPAT is post-tax. Both measure earnings from core operations before interest, but operating profit excludes taxes while NOPAT includes them.

To convert between them:

- NOPAT to operating profit: add taxes back

- Operating profit to NOPAT: subtract taxes

Example: If NOPAT is $80,000 and taxes are $16,000, operating profit is $96,000.

Use Xero to simplify NOPAT tracking

Tracking the numbers you need for NOPAT and other financial metrics is easier with the right tools. Xero helps you bring it all together by automating bookkeeping and generating financial reports with just a few taps.

With Xero, you can:

- Track income and expenses automatically through bank feeds

- Generate profit reports to find your operating profit quickly

- Monitor tax obligations to calculate your effective rate

Ready to simplify your financial tracking? Get one month free and see how Xero can help you stay on top of your numbers.

FAQs on NOPAT

Common questions about NOPAT answered.

Is NOPAT the same as free cash flow?

No. NOPAT is an accrual-based profit metric, while free cash flow measures the actual cash a business generates after accounting for capital expenditures and changes in working capital.

Why is NOPAT used in DCF analysis?

NOPAT provides clean operational earnings without financing effects, making it the starting point for calculating unlevered free cash flow in discounted cash flow (DCF) valuations.

When should I use NOPAT instead of net income?

Use NOPAT when comparing companies with different debt levels, evaluating operational efficiency, or calculating return on invested capital independent of financing decisions.

Can NOPAT be negative?

Yes. Negative NOPAT occurs when operating losses exceed any tax benefits, indicating the core business is losing money after considering taxes.

How often should I calculate NOPAT?

Calculate NOPAT quarterly or annually to track operational performance over time. Compare results across periods or against industry benchmarks.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Start using Xero for free

Access Xero features for 30 days, then decide which plan best suits your business.