Gross profit margin: formula, example and how to improve

Learn what gross profit margin is, how to calculate it, and practical ways to improve it for your business.

Written by Lena Hanna—Trusted CPA Guidance on Accounting and Tax. Read Lena's full bio

Published Wednesday 27 May 2026

Table of contents

Key takeaways

- Gross profit margin is the percentage of revenue your business keeps after paying direct costs. Calculate it by subtracting cost of goods sold (COGS) from revenue, dividing by revenue, and multiplying by 100.

- A healthy gross profit margin varies by industry. Professional services often exceed 50%, while retail grocery businesses may sit below 30%.

- Review your gross profit margin monthly to catch rising costs or pricing pressure early. Declining trends signal the need to adjust prices or renegotiate supplier contracts.

- Improve your margin by raising prices based on the value you deliver and reducing COGS through supplier negotiations, waste reduction, and streamlined processes.

What is gross profit margin?

Gross profit margin is the percentage of revenue your business keeps after paying direct costs. It measures how efficiently you turn each dollar of sales into profit before covering operating expenses like rent, wages, and marketing.

Calculating your direct costs accurately matters. There are special rules for NZ retailers with a turnover of $1 million or less when valuing trading stock.

Tracking gross profit margin helps you make better business decisions. Here's what it reveals:

- How much revenue you retain to cover operating expenses and generate net profit.

- How well you control production and service delivery costs.

- Which areas of your business are most profitable and where problems may sit.

- Whether you have enough margin to invest in growth.

Higher gross profit margins give you more capacity to cover fixed costs and build a buffer against unexpected expenses.

Gross profit margin vs gross profit

Gross profit is a dollar amount. Gross profit margin is a percentage. Both measure what stays after direct costs, but they present the information differently.

Gross profit tells you how many dollars remain after subtracting cost of goods sold (COGS) from revenue. Gross profit margin expresses that same figure as a percentage of revenue. The term "gross margin" means the same thing as gross profit margin.

For example, if your business earns $100,000 in revenue and COGS is $40,000:

- Gross profit: $100,000 - $40,000 = $60,000.

- Gross profit margin: ($60,000 / $100,000) x 100 = 60%.

Use gross profit to see the dollar value available. Use gross profit margin to compare performance across periods, products, or competitors of different sizes.

Gross profit margin vs markup

Gross profit margin and markup both relate costs to revenue, but they use different base figures. Confusing the 2 can lead to pricing errors that eat into your profits.

Gross profit margin expresses profit as a percentage of revenue (the selling price). Markup expresses profit as a percentage of cost (what you paid). Here are the formulas side by side:

- Gross profit margin = (Revenue - COGS) / Revenue x 100.

- Markup = (Revenue - COGS) / COGS x 100.

For example, you sell a product for $80 and it costs $50 to produce:

- Gross profit margin: ($80 - $50) / $80 x 100 = 37.5%.

- Markup: ($80 - $50) / $50 x 100 = 60%.

The same transaction produces a 37.5% margin but a 60% markup. When setting prices, know which metric you're using. A 50% markup does not equal a 50% gross profit margin.

How to calculate gross profit margin

Calculating gross profit margin takes 2 steps and 1 simple formula. Start by gathering your revenue and cost of goods sold figures for the same time period.

1. Understand the formula

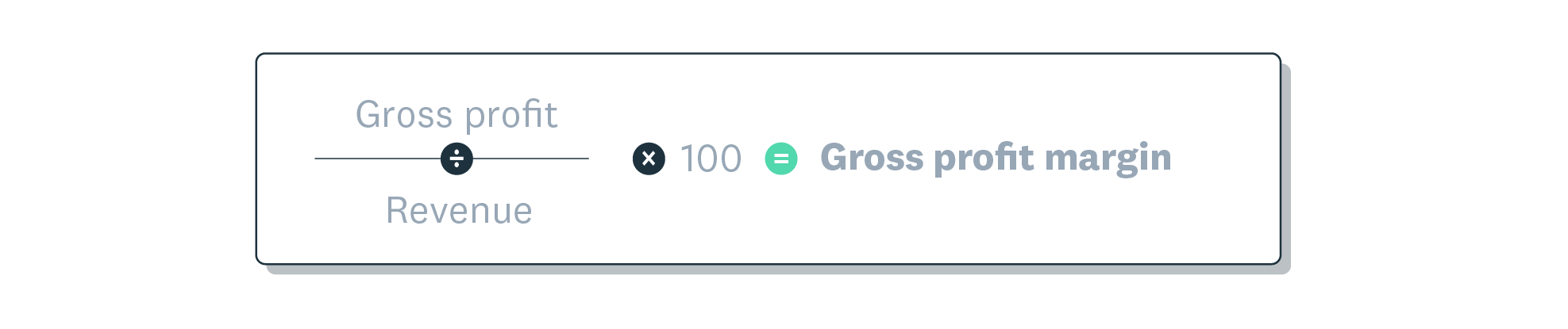

Use this formula to calculate your gross profit margin:

Gross profit margin = (gross profit / revenue) x 100

Where:

- Gross profit = revenue minus cost of goods sold (COGS).

- Revenue = total net sales income (after returns and discounts).

- The result is a percentage showing how much of each dollar you keep.

2. Identify your cost of goods sold

COGS includes every direct cost tied to producing your goods or delivering your services. What falls under COGS depends on your business type.

For product-based businesses, COGS typically includes:

- Raw materials and components.

- Direct labour (manufacturing or assembly).

- Packaging and freight to your warehouse.

- Factory overheads directly tied to production.

For service-based businesses, COGS typically includes:

- Direct labour costs for delivering the service.

- Materials consumed during service delivery.

- Subcontractor fees.

- Software or tools used exclusively for client work.

Exclude operating expenses like rent, marketing, and office salaries. These sit below gross profit on your profit and loss report.

3. Run the calculation

Follow these 2 steps to calculate your gross profit margin:

- Calculate your gross profit: subtract your COGS from your total net revenue. The result is your gross profit in dollars.

- Calculate your gross profit margin: divide your gross profit by your total net revenue, then multiply by 100. The result is your gross profit margin percentage.

4. Work through an example

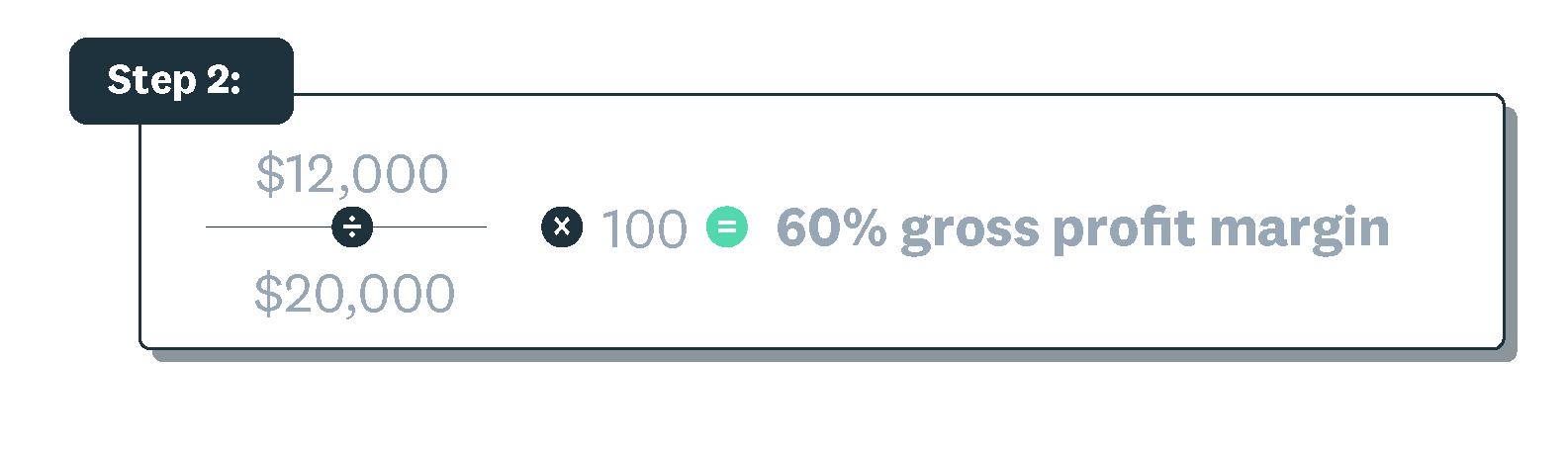

Here's a worked example for a NZ cleaning business:

Your cleaning business earns $20,000 in net revenue for the month. Your direct costs (cleaning supplies, direct labour, equipment maintenance) total $8,000.

- Gross profit: $20,000 - $8,000 = $12,000.

- Gross profit margin: ($12,000 / $20,000) x 100 = 60%.

A 60% gross profit margin means you keep 60 cents of every dollar earned after direct costs. The remaining 40 cents covers operating expenses, tax, and net profit.

Common gross profit margin mistakes

Small errors in your gross profit margin calculation can lead to poor pricing decisions and inaccurate financial reporting. Here are 5 common mistakes to avoid.

- Leaving costs out of COGS: forgetting to include freight, packaging, or direct labour understates your true costs and inflates your margin.

- Mixing up revenue types: use net revenue (after returns, discounts, and allowances), not gross revenue. Using gross revenue overstates your margin.

- Including operating expenses in COGS: rent, marketing, and office salaries are operating expenses. Adding them to COGS distorts your gross profit margin.

- Mismatching time periods: your revenue and COGS must cover the same period. Comparing 1 month of revenue to a quarter of costs produces a meaningless figure.

- Rounding too early: round only at the final percentage step. Rounding dollar figures mid-calculation compounds errors, especially at higher volumes.

Eligible NZ businesses with sales under $1.3 million can simplify stock valuation. They can use the same closing value of trading stock as their opening value.

What is a good gross profit margin?

A "good" gross profit margin depends on your industry, business model, and operating costs. Your margin needs to cover operating expenses, taxes, and leave enough for reinvestment and net profit.

Industry benchmarks

Gross profit margins vary widely across industries. Here are typical ranges for common NZ small business sectors:

- Professional services (consulting, accounting, legal): 50% to 70%.

- Software and digital services: 60% to 80%.

- Construction and trades: 25% to 45%.

- Hospitality and food service: 25% to 40%.

- Retail (general merchandise): 30% to 50%.

- Retail (grocery and food): 20% to 30%.

Higher margins typically occur in industries with strong pricing power, low material costs, or premium positioning. Lower margins are common where competition is fierce or material costs are high.

Benchmarking your business

Compare your gross profit margin with similar-sized businesses in your industry and region. This gives you a clearer picture than comparing against unrelated sectors. Your accountant or bookkeeper can help you find benchmarks for NZ small businesses in your industry.

When to reassess your margin

Review your gross profit margin when market conditions shift. Rising supplier costs, changes in customer demand, or new competitors entering your market all affect your margin. Monthly reviews help you spot problems early and act before they erode your profitability.

Real-world gross profit margin examples

Looking at real company margins helps put the benchmarks into context. Here are 3 examples from well-known companies operating in the AU/NZ market, based on their published financial reports.

- Woolworths Group (grocery retail): approximately 27% gross profit margin. Grocery retail operates on thin margins due to high COGS and intense price competition.

- JB Hi-Fi (electronics retail): approximately 22% gross profit margin. Electronics retail has slim margins because product costs consume most of the revenue.

- Xero (cloud software): approximately 87% gross profit margin. Software businesses typically have high margins because the cost of delivering each additional subscription is low.

These figures show why comparing your margin against your own industry matters more than chasing an absolute number. A 25% margin in grocery retail signals strong performance, while the same figure in software may signal a problem.

Analysing gross profit margin for business insights

Your gross profit margin is more than a single number. Analysing it over time and across products reveals which parts of your business generate the most profit and where you may be losing money.

Interpreting trends

Track your gross profit margin monthly to spot patterns. Here's what different trends may signal:

- Rising margin with stable revenue: your cost control is improving or your supplier costs have dropped.

- Falling margin with rising revenue: your costs are growing faster than your sales, possibly due to supplier price increases or inefficient scaling.

- High margin with low sales volume: your prices may be too high, discouraging customers.

- Low margin with high sales volume: you may be competing on price when you could charge more.

Factors that affect your margin

Several external forces can shift your gross profit margin. Stay alert to these common factors:

- Supplier cost increases: rising raw material or wholesale prices directly reduce your margin if you don't adjust your selling prices.

- Changes in customer demand: shifts in what customers buy can change your product mix and overall margin.

- Seasonal patterns: many NZ businesses see margin fluctuations tied to seasonal demand or holiday trading periods.

- Exchange rate movements: if you import materials, a weaker NZ dollar increases your COGS.

Spotting a declining trend early gives you time to act. Adjust prices, renegotiate supplier contracts, or shift your product mix before your bottom line suffers.

How to improve gross profit margin

You can improve your gross profit margin in 2 main ways: increase your prices or reduce your cost of goods sold. Most businesses benefit from combining both strategies.

Adjust your prices

Raising prices can improve your margin if customers see the value. Consider these pricing strategies:

- Value-based pricing: set prices based on the outcomes you deliver, not just what it costs you. Customers pay for results.

- Regular price reviews: assess your pricing quarterly to reflect changes in supplier costs, demand, and competitor pricing.

- Bundling: combine products or services into packages that increase the average transaction value while reducing per-unit costs.

- Communicate increases clearly: explain price changes by highlighting the value customers receive. Transparency builds loyalty.

Reduce your cost of goods sold

Lowering your COGS directly lifts your gross profit margin. Focus on these cost reduction tactics:

- Negotiate with suppliers: request volume discounts, longer payment terms, or explore alternative suppliers offering better rates.

- Reduce waste: audit your production or service delivery process to identify materials, time, or labour going to waste.

- Streamline processes: remove unnecessary steps in your workflow. Automation and better accounting tools can cut direct labour costs.

- Review your product mix: focus on higher-margin products or services and consider phasing out low-margin lines that drain resources.

Track your gross profit margin with Xero

Xero Accounting Software can help you monitor your gross profit margin in real time. The profit and loss report surfaces your gross profit automatically, so you can see how your margin changes month to month without manual calculations.

With real-time bank reconciliation and customisable reporting, Xero gives you a clear view of your direct costs and revenue as transactions happen. You can spot margin shifts early and take action before they affect your bottom line.

Start tracking your gross profit margin today. Get one month free.

FAQs on gross profit margin

Here are answers to frequently asked questions about gross profit margin.

What's the difference between gross profit margin and net profit margin?

Gross profit margin measures profit after direct costs (COGS) only. Net profit margin accounts for all expenses, including operating costs, taxes, and interest. Gross profit margin is always higher because it excludes those additional costs.

Can a business survive with a low gross profit margin?

Yes, some businesses operate successfully with low margins by achieving high sales volumes. Grocery retailers are a common example. You need tight cost control and efficient operations to stay profitable on thin margins.

How often should I calculate gross profit margin?

Calculate your gross profit margin monthly. This frequency lets you spot trends and address issues before they compound. Review it quarterly alongside other profitability ratios for a fuller picture of business performance.

What if my gross profit margin is negative?

A negative gross profit margin means your direct costs exceed your revenue. This signals a serious pricing or cost problem that needs immediate attention. Review your pricing strategy and look for ways to reduce COGS urgently.

Is labour included in cost of goods sold?

COGS includes direct labour. This covers wages for employees who produce goods or deliver services directly to customers. Indirect labour, such as office administration and management salaries, falls under operating expenses and sits below the gross profit line.

What are the limitations of gross profit margin?

Gross profit margin only accounts for direct costs. It ignores operating expenses, taxes, and interest, so a high gross margin doesn't guarantee overall profitability. It also varies widely by industry, making cross-industry comparisons unreliable without context.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.