What is revenue in accounting? Definition and examples

Learn what revenue is, why it matters, and how to use it to price, forecast, and grow.

Written by Shaun Quarton—Accounting & Finance Content Writer and Growth Marketer. Read Shaun's full bio

Published Friday 13 February 2026

Table of contents

Key takeaways

- Calculate your net revenue by subtracting discounts, returns, and allowances from gross sales to get a more accurate picture of your actual earnings than basic revenue calculations provide.

- Track both revenue and profit separately since high revenue doesn't guarantee business success if your expenses exceed your earnings, which could still leave you operating at a loss.

- Categorise your revenue by product lines, sales channels, and customer segments to identify which areas drive the most income and make more informed business decisions.

- Update your revenue records daily and reconcile them with bank statements monthly to maintain accuracy, spot discrepancies early, and avoid cash flow problems or tax issues.

What is revenue in accounting?

Revenue is the total money your business earns from selling products or services. It's also called sales or turnover and sits at the top of your income statement, which is why it's often called the "top line."

For example, a bakery's revenue comes from selling bread and pastries, while a freelancer earns revenue by providing services. Revenue is the starting point for calculating profit.

Revenue vs profit: Key differences

Revenue is the total money coming into your business, while profit is what remains after you subtract all expenses. Revenue sits at the top of your income statement (the "top line"), and profit sits at the bottom (the "bottom line").

Here's how they compare:

Revenue:

- Calculation: total sales (units sold × price)

- Focus: measures income generated before any deductions

- Significance: shows sales performance and market demand

Profit:

- Calculation: revenue minus all costs

- Focus: measures income after deducting all expenses

- Significance: shows financial health and long-term sustainability

Learn more about profit and calculating profits.

High revenue doesn't guarantee success. If your expenses exceed your earnings, you could still operate at a loss.

Knowing both metrics helps you:

- Set realistic goals: base targets on actual profit, not just sales figures

- Price effectively: ensure your prices cover costs and generate profit

- Build sustainability: focus on long-term growth, not just short-term revenue

Revenue vs income: Key differences

Revenue covers only money earned from your core business activities, while income is a broader term that includes revenue plus other earnings like investment returns, government subsidies, or one-time gains. While modern accounting frameworks sometimes treat revenue and gains similarly, keeping them separate matters for practical business reporting.

Here's how they differ:

Revenue:

- Scope: limited to sales of goods or services from primary operations

- Focus: shows core business performance and pricing effectiveness

- Indicator: reflects market demand; declining revenue may signal strategic issues

Income:

- Scope: includes revenue plus investments, subsidies, and other earnings

- Focus: shows overall financial health beyond daily sales

- Indicator: reflects total earnings and resource management efficiency

Strong revenue signals healthy sales, but income reveals your true financial stability.

Here's how knowing both helps you:

- Make smarter decisions: identify where money comes from and optimise earnings

- Assess true health: determine whether you're profitable after all costs

- Plan for growth: balance both metrics to build sustainable success

Types of business revenue

Businesses generate revenue through different channels, which fall into two main categories: operating revenue and non-operating revenue.

Operating revenue

Operating revenue is income from your primary business activities. It's the foundation of your financial performance and often called gross revenue.

Common types include:

- Sales revenue: income from selling goods, like a bakery selling bread and pastries

- Service revenue: income from providing services, like consulting or repairs

- Subscription revenue: recurring income from memberships or subscriptions, like gyms or streaming services

Tip: Sales revenue often covers all main income activities. Service revenue is useful when you want to track service income separately, especially if you sell both goods and services.

Non-operating revenue

Non-operating revenue is income from activities outside your core business operations. These earnings are often irregular and not tied to day-to-day performance.

Examples include:

- Interest income: earnings from bank deposits or investments

- Dividend income: returns from shares in other companies

- Rental income: payments from leasing property or equipment

- Gain on asset sales: proceeds from selling old equipment or property

- Licensing fees: payments for others using your patents or trademarks

- Franchise fees: income from franchisees operating under your brand

- Advertising revenue: payments for displaying ads on your website or property

How to calculate revenue

Follow these steps to calculate and track your revenue:

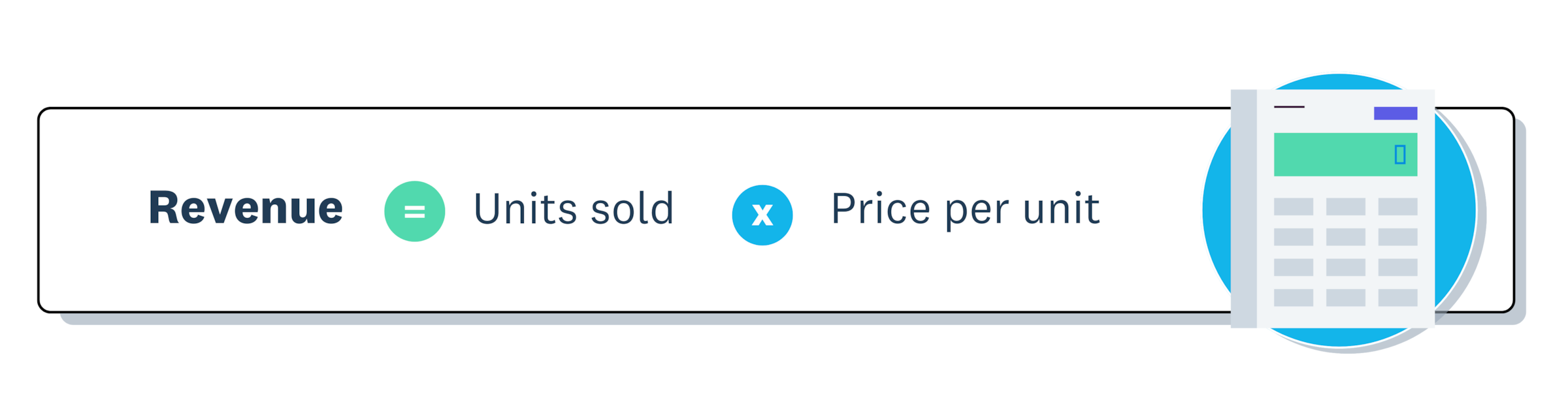

Step 1: Use the basic revenue formula

Revenue = Units sold × Price per unit

For example, if a bakery sells 100 loaves of bread at $5 each:

100 × $5 = $500 revenue

Step 2: Adjust for different business models

Revenue calculations vary by business type. Here's how to adjust:

Service-based businesses:

Revenue = Hourly rate × Hours worked

Subscription-based businesses:

Revenue = Number of subscribers × Subscription price

Ecommerce businesses:

Track each transaction individually, as prices may vary per sale.

Accounting software like Xero simplifies tracking across all business models.

Step 3: Calculate net revenue

Net revenue provides a more accurate picture of your earnings after returns, discounts, and allowances. The formula is:

Net revenue = (Units sold × Price per unit) - Discounts - Returns

This gives a clearer understanding of your actual income, as it accounts for any adjustments to your revenue.

Step 4: Track your revenue

Consistent tracking keeps your financial records accurate and supports better decisions. Choose a method that fits your business:

- Spreadsheets: best for very small businesses, but prone to errors and time-consuming

- Point of sale (POS) systems: ideal for physical stores, with automatic sales data integration

- Accounting software: best for automation and advanced reporting (Xero, QuickBooks, and similar)

Whatever method you choose, record every sale correctly and consistently. Automate where possible to reduce errors and save time.

What is revenue recognition?

Revenue recognition is the accounting principle that determines when you record revenue in your books.

Under accrual accounting, you record revenue when it's earned, even if payment comes later. For example, a bakery delivers a bulk order to a cafe in July but doesn't receive payment until August. The revenue is recorded in July when the goods are delivered.

Under cash accounting, you record revenue only when payment is received. Some small businesses, like sole traders, use this simpler method. For instance, in the US, businesses can typically use the cash method for tax purposes if their annual gross receipts average $25 million or less over the last three years.

You should recognise revenue according to the International Financial Reporting Standards (IFRS). The key standard for this is IFRS 15, which has been effective since January 2018. Here's more about cash vs accrual accounting.

Why tracking revenue is important for your small business

Tracking revenue shows how much money flows into your business before expenses. It reveals trends, guides important decisions, and supports long-term growth.

Regular tracking helps you measure performance, forecast earnings, and make informed financial decisions.

Drive business growth

Steady revenue growth supports lasting success by giving you resources to invest in new projects, scale your operations, and attract investors.

For example, a bakery with a steady income might use surplus funds to open a second location, upgrade its equipment, or add new product lines.

Measure performance

Tracking revenue allows you to monitor progress towards financial goals. Ask yourself:

- Are you meeting your revenue targets?

- Where can you improve?

- Which areas contributed most?

Benchmarking against the market can also provide valuable insights. Explore Xero Small Business Insights to learn more.

Gain insights and identify trends

Revenue data helps businesses make smarter inventory, marketing, and product development decisions by identifying key patterns:

- Are sales increasing or decreasing?

- Which products are performing best?

- Are seasonal factors affecting your revenue?

Make informed business decisions

Decisions based on data lead to better results. Revenue tracking helps you determine:

- Should you adjust your pricing strategy?

- Is it time to invest in new equipment?

- Are you ready to expand into new markets?

Revenue doesn't equal profitability. Learn more about increasing revenue.

Best practices for effective revenue tracking

Accurate revenue tracking keeps your financial statements reliable. It also helps you avoid poor decisions, cash flow problems, and tax issues. Follow these best practices:

Maintain accurate records

- Daily: Update records to stay on top of transactions

- Monthly: Reconcile revenue with bank statements to spot discrepancies early

- Always: Keep receipts and supporting documents for tax and audit purposes

For example, the IRS advises keeping records of employment for at least four years.

Categorise your revenue

Break down revenue by product lines, sales channels (online, in-store), and customer segments. This helps you understand where your revenue is coming from and enables more effective decision-making.

Use tools for automation

Invest in accounting software to streamline tracking and reduce human error. This saves time and ensures more accurate financial insights.

Review data regularly

Set aside time each month to review your revenue data, spot trends, and identify areas for improvement.

Unlock your business potential with Xero

Tracking revenue shows you where your money comes from, helps you plan your business future, and supports decisions that drive success.

With Xero, you can automate tracking, get real-time insights, and streamline your accounting, all in one platform.

Get started with Xero and get one month free

FAQs on revenue

Here are answers to common questions about revenue for small businesses.

How often should I track my revenue?

Track revenue at least weekly to spot trends early, and reconcile with bank statements monthly. More frequent tracking gives you better visibility into cash flow patterns.

Can I have high revenue but still lose money?

Yes. If your expenses exceed your revenue, you'll operate at a loss regardless of how much you sell. That's why tracking both revenue and profit matters.

What's the difference between gross revenue and net revenue?

Gross revenue is total sales before any deductions. Net revenue is what remains after subtracting returns, discounts, and allowances.

Do I need special software to track revenue?

Spreadsheets work for very small operations. But accounting software like Xero saves time, reduces errors, and provides real-time insights as your business grows.

What should I do if my revenue is declining?

Review your pricing and analyse which products or services are underperforming. Also check for seasonal patterns. Declining revenue often signals a need to adjust your strategy or marketing.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Start using Xero for free

Access Xero features for 30 days, then decide which plan best suits your business.