Financial statement guide: types and how to read them

Discover how financial statements give you clarity on cash, profit, and growth so you can act with confidence.

Written by Lena Hanna—Trusted CPA Guidance on Accounting and Tax. Read Lena's full bio

Published Wednesday 1 April 2026

Table of contents

Key takeaways

- Review your financial statements monthly for cash flow, quarterly for all statements to spot trends, and annually for comprehensive analysis to avoid the common mistake of waiting until tax time when problems go unnoticed.

- Focus on key metrics like gross profit margin and current ratio rather than just revenue numbers, as high sales don't guarantee success without understanding your expenses and ability to pay debts.

- Understand that profit on your income statement doesn't equal cash in the bank by reviewing your cash flow statement alongside your profit and loss to see how money actually moves through your business.

- Use all three core financial statements together since each provides a different view: the income statement shows profitability, the balance sheet shows what you own and owe, and the cash flow statement explains changes in your bank balance.

What are financial statements?

Financial statements are standardised reports that summarise your business's financial activity, with their format governed by regulations like IFRS 18, the new IFRS Accounting Standard for primary financial statements. They show what you own, what you owe, how much you've earned, and how cash moves through your business.

Most small businesses use three to four main financial statements:

- Income statement: Shows revenue, expenses, and profit over a period.

- Balance sheet: Shows assets, liabilities, and equity at a specific date.

- Cash flow statement: Shows how cash enters and leaves your business.

- Statement of changes in equity: Shows how owner investment changes over time.

Types of financial statements

Each financial statement gives you a different view of your business finances. Here are the main ones you'll work with.

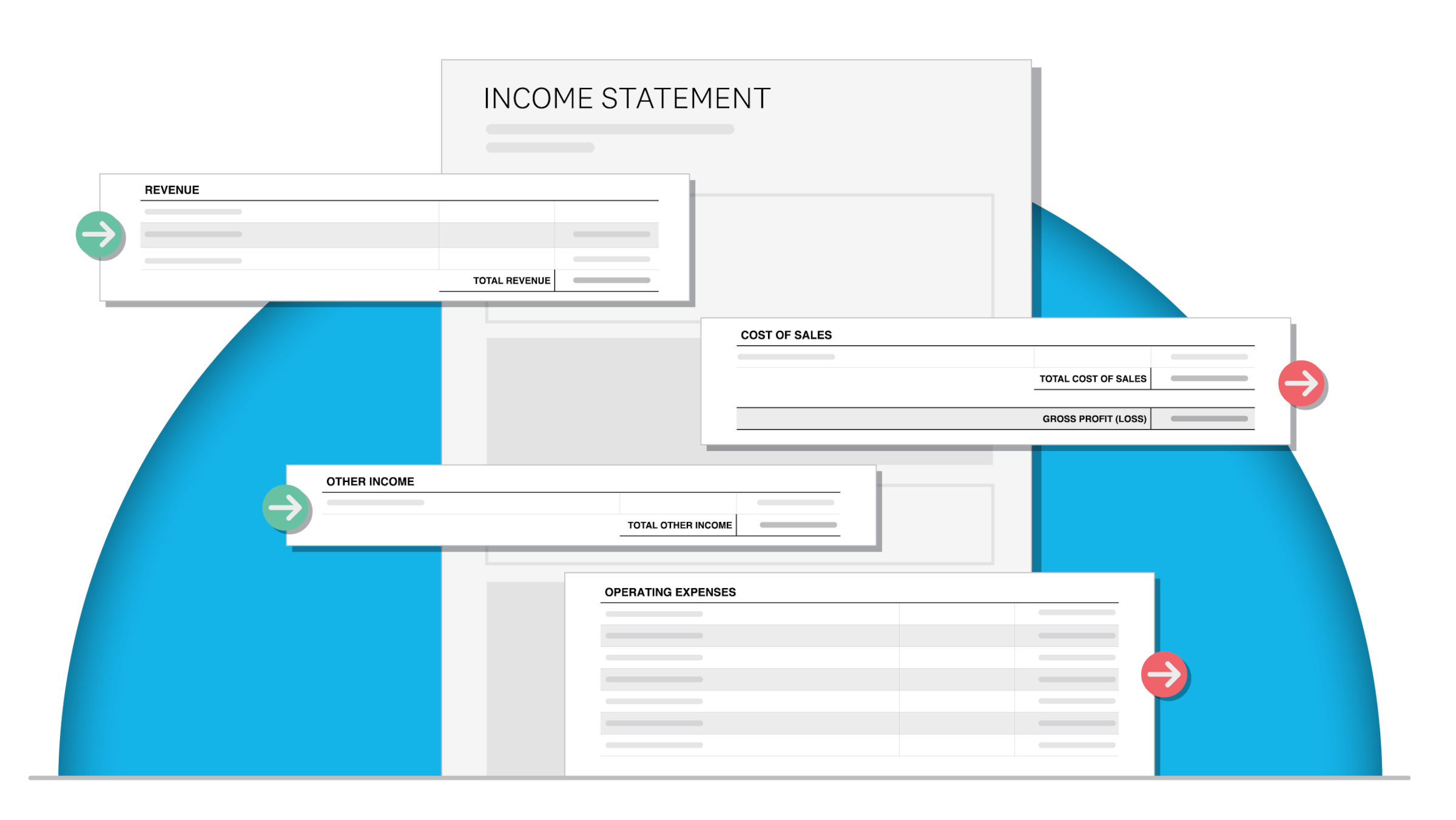

Income statement (profit and loss statement)

An income statement shows whether your business made or lost money over a specific period. It's also called a profit and loss statement or P&L.

Your income statement includes:

- Revenue: Represents money earned from sales or services.

- Expenses: Cover the costs of running your business.

- Net profit or loss: Shows what's left after subtracting expenses from revenue.

Balance sheet

A balance sheet shows what your business owns and owes at a single point in time. Think of it as a financial snapshot.

Your balance sheet includes:

- Assets: Include cash, inventory, equipment, and money owed to you.

- Liabilities: Include debts, loans, and money you owe others.

- Equity: Represents the owner's stake in the business after subtracting liabilities from assets.

Cash flow statement

A cash flow statement, a report formally defined by standards like IAS 7 Cash Flow Statements, tracks how cash moves in and out of your business. It explains why your bank balance changed, even if your income statement shows a profit.

Your cash flow statement includes:

- Operating activities: Track cash from day-to-day business operations.

- Investing activities: Track cash spent on or received from assets.

- Financing activities: Track cash from loans, investments, or owner withdrawals.

Statement of changes in equity

This report details the changes in your company's equity over time. It shows how profits, owner contributions, and withdrawals have affected your stake in the business.

Why financial statements matter for your business

Financial statements help you make informed decisions about your business. Without them, you're guessing at your financial health instead of knowing it, which is risky when data shows only about half of these businesses see their fifth anniversary, according to IFAC research on SME survival rates.

Here's why financial statements matter for your small business:

- Assess profitability: See whether you're making or losing money each month.

- Manage cash flow: Understand why cash is tight even when sales look strong.

- Secure funding: Provide lenders and investors with the documentation they need.

- Meet tax requirements: Prepare accurate returns and avoid penalties.

- Track progress: Measure performance against your goals over time.

- Spot problems early: Identify issues before they become serious.

How to read your financial statements

Reading financial statements means understanding what the numbers tell you about your business health. You don't need an accounting degree to interpret the key figures.

Focus on these areas when reviewing your statements:

- Trends over time: Compare this month to last month, or this year to last year.

- Key ratios: Calculate simple metrics that reveal your financial position.

- Warning signs: Look for patterns that suggest problems ahead.

Key metrics in your income statement

- Gross profit margin: Measures how much you keep after direct costs. Calculate by dividing gross profit by revenue. A higher percentage means better efficiency.

- Net profit margin: Shows what percentage of revenue becomes actual profit. Calculate by dividing net profit by revenue. Compare this to industry benchmarks for your business type.

- Revenue growth: Tracks whether sales are increasing or decreasing. Compare current period revenue to the same period last year.

Understanding your balance sheet position

- Current ratio: Measures your ability to pay short-term debts. Divide current assets by current liabilities. A ratio above 1.0 means you can cover immediate obligations.

- Debt-to-equity ratio: Shows how much you rely on borrowed money. Divide total liabilities by total equity. Lower ratios generally indicate less financial risk.

Interpreting cash flow patterns

Review where your cash is coming from and where it's going. Positive cash flow from operations is a strong sign that your core business is healthy and sustainable.

-calculation-2.1708626946541.png)

How often to review your financial statements

How often you review financial statements depends on your business needs. Here's a practical schedule for most small businesses:

- Monthly: Review your cash flow statement to stay on top of liquidity and avoid surprises.

- Quarterly: Review all three main statements to spot trends and adjust your strategy.

- Annually: Conduct a comprehensive review for tax preparation, investor reporting, and business planning. This aligns with international standards requiring statements to be presented at least annually.

If your business has tight margins or rapid growth, consider reviewing statements more frequently.

Common financial statement mistakes to avoid

Small business owners often misread or overlook important information in their financial statements. Here are the most common mistakes and how to avoid them:

- Confusing profit with cash: your income statement may show a profit, but that doesn't mean cash is in your bank account. Review your cash flow statement alongside your P&L.

- Ignoring the balance sheet: many owners focus only on profit and loss. Your balance sheet shows whether you can pay your debts and how much equity you've built.

- Not reconciling regularly: outdated or inaccurate data leads to poor decisions. Reconcile your bank accounts at least monthly to keep your statements accurate.

- Focusing only on revenue: high sales don't guarantee success. Watch your expenses and margins to understand true profitability.

- Waiting until tax time: reviewing statements only once a year means problems go unnoticed. Regular reviews help you catch issues early.

How Xero creates your financial statements automatically

Xero generates your financial statements automatically as you run your business. Here's how it works:

- Connect your bank accounts: Transactions import automatically from your linked accounts, reducing manual data entry.

- Categorise transactions: Assign each transaction to the correct account. Xero learns your patterns and suggests categories over time.

- Reconcile regularly: Match imported transactions to your records. This ensures your statements reflect accurate, up-to-date information.

- Generate reports instantly: Access your income statement, balance sheet, and cash flow statement in real time from your dashboard.

With real-time reporting, you always know where your business stands financially. You get automated income statements and live cash flow tracking without manual data entry.

FAQs on financial statements

Here are answers to common questions about financial statements and how they work for small businesses.

What's the difference between 3, 4, and 5 financial statements?

The three core financial statements are the income statement, balance sheet, and cash flow statement. A fourth statement, the statement of changes in equity, is sometimes required for larger businesses. A fifth, the notes to financial statements, provides additional context but isn't always considered a standalone statement.

Are financial statements the same as a tax return?

No. Financial statements summarise your business's financial activity, while a tax return reports taxable income to the government. Your financial statements help you prepare your tax return, but they serve different purposes.

Can I create financial statements without an accountant?

Yes. Accounting software like Xero generates financial statements automatically from your transaction data. You may still want an accountant to review your statements or help with complex situations, as one global survey found the vast majority of small and mid-sized practices offer some form of advisory or consulting services.

Do I need all types of financial statements for my small business?

Most small businesses need at least an income statement and balance sheet. A cash flow statement becomes important as your business grows or if you're seeking funding. Requirements vary by business structure and location.

How do financial statements differ from management reports?

Financial statements follow standardised formats for external reporting to banks, investors, and tax authorities. Management reports are flexible internal documents you can customise to track specific metrics that matter to your business.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Start using Xero for free

Access Xero features for 30 days, then decide which plan best suits your business.