Cost of sales: what it is, how to calculate and cut

Learn how cost of sales guides pricing and profit, and see simple steps to calculate it.

Written by Lena Hanna—Trusted CPA Guidance on Accounting and Tax. Read Lena's full bio

Published Friday 13 February 2026

Table of contents

Key takeaways

- Calculate your cost of sales by including only direct costs that wouldn't exist without making a sale, such as materials, direct labour, and production expenses, while excluding indirect costs like rent, marketing, and administrative salaries.

- Apply the appropriate formula for your business type: service businesses total direct delivery costs, retailers use beginning inventory plus purchases minus ending inventory, and manufacturers combine raw materials, production labour, and manufacturing overhead.

- Review your cost of sales regularly to identify rising expenses before they squeeze your profit margins, and use this information to set profitable prices that cover all direct costs plus your desired markup.

- Reduce your cost of sales by negotiating better supplier terms, comparing suppliers quarterly, improving production efficiency, and optimising inventory management to boost profitability without raising prices.

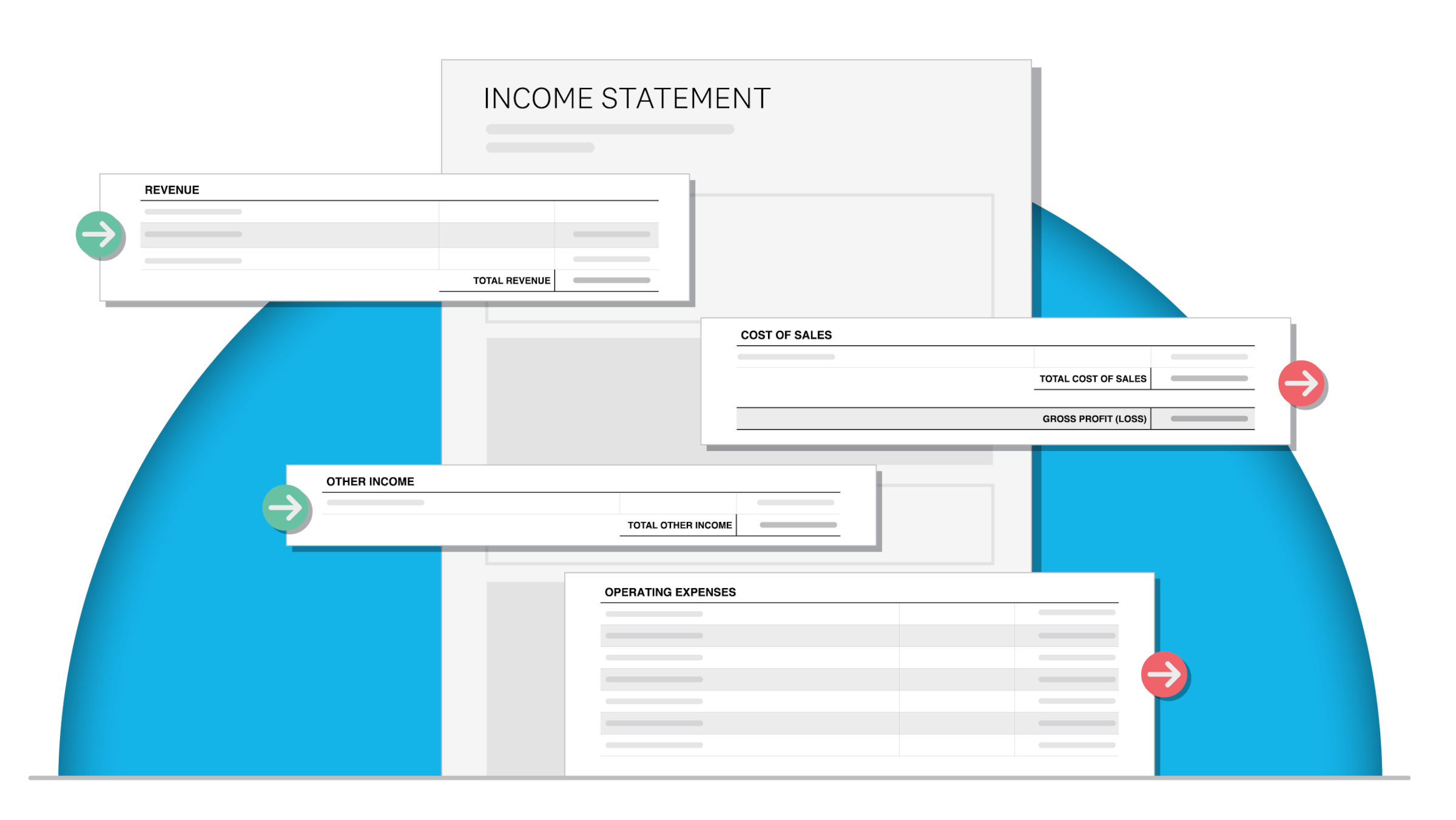

What is cost of sales?

Cost of sales is the total expense of delivering a product or service to your customer. It includes direct costs like materials, labour, and production, but excludes indirect expenses like rent or marketing.

Understanding your cost of sales helps you set profitable prices and choose the right suppliers. You might also call this figure cost of goods sold (COGS), though the terms have subtle differences.

For most small businesses, cost of sales equals direct costs: the expenses tied directly to the goods or services you sell. Don't confuse these with indirect costs, which are general business expenses unrelated to production or service delivery.

What counts as cost of sales varies by business type:

- Retailers: stock, packaging, and shipping

- Service providers: software subscriptions, subcontractors, and direct labour

What to include in cost of sales

Knowing what to include in your cost of sales calculation ensures accurate pricing and profitability tracking. You should only include direct costs, which are expenses that would not exist if you did not make a sale.

Include these costs:

- Direct materials and supplies

- Direct labour (staff who produce goods or deliver services)

- Manufacturing or production costs

- Packaging materials

- Freight and shipping (if tied to product delivery)

- Sales commissions (if paid per sale)

- Subcontractor fees (for service businesses)

Exclude these costs:

- Rent and utilities (unless a dedicated production facility)

- Marketing and advertising

- Administrative salaries

- Office supplies

- Insurance and legal fees

When in doubt, ask: "Would this cost exist if I made no sales?" If yes, it's likely an operating expense. If no, it's probably a cost of sale.

Why is cost of sales important?

Cost of sales directly affects your profitability. It sets the baseline for pricing: you must charge above this figure to make a profit on each sale.

Understanding your cost of sales helps you:

- Set profitable prices: Know your minimum price point before adding margin

- Spot margin pressure: Identify rising costs before they erode profits

- Plan for growth: Anticipate new expenses like warehouse space or additional staff

You can usually calculate labour costs straightforwardly, but other expenses can surprise you. An ecommerce business working from home may enjoy strong margins initially, but those margins shrink when you need to pay for warehouse space or a dedicated workspace.

Your cost of sales includes both fixed costs and variable costs that directly relate to delivering your product or service.

- Fixed costs: expenses that stay consistent regardless of production volume, like employee salaries

- Variable costs: expenses that fluctuate with production, like shipping fees or raw materials

Include both cost types in your calculation for an accurate picture. Calculate your cost of sales regularly to catch rising expenses, like delivery fees, before they squeeze your margins. This helps you decide when to raise prices or find alternative suppliers.

How to calculate cost of sales

The cost of sales formula varies depending on your business type. Each formula captures the direct costs specific to how you deliver value to customers.

Below are calculation methods for three common business types: service businesses, retailers, and manufacturers.

Cost of sales for service businesses

Service businesses calculate cost of sales by totalling the direct costs of delivering their services.

Include these costs in your calculation:

- Employees who deliver services directly to clients

- Workspace costs for service delivery

- Travel expenses (if required for client work)

- Equipment costs (if used for service delivery)

Exclude these costs from your calculation:

- Back-office staff (admin, HR, finance)

- General office expenses not tied to service delivery

A freelancer working from home on a laptop may only need to include their direct labour time and any software subscriptions required for client work.

Cost of sales for retailers

Retailers calculate cost of sales using an inventory-based formula: beginning inventory plus purchases minus ending inventory.

Include these costs in your calculation:

- Stock or inventory purchases

- Packaging materials

- Shipping costs (for ecommerce)

- Transaction fees (payment processing)

This formula tracks the actual cost of goods sold during a specific period, accounting for inventory you had at the start, what you bought, and what remains unsold.

Cost of sales for manufacturers

Manufacturers calculate cost of sales by combining raw materials, production labour, and manufacturing overhead, with some large manufacturers reporting a cost of sales at 65% of revenue due to high raw material intensity and labour costs.

Include these costs in your calculation:

- Direct production labour

- Manufacturing equipment costs

- Factory utilities tied to production

You may optionally include these costs, depending on your accounting approach:

- Warehousing costs

- Freight and logistics

Some manufacturers treat warehousing and freight as operating expenses rather than cost of sales. Choose one approach and apply it consistently for accurate period-over-period comparisons.

Cost of sales examples

Some expenses fall into a grey area between cost of sales and operating expenses. The key principle: be consistent with your classification.

Common grey-area expenses include:

- Sales commissions: you can classify these as cost of sales (tied to each sale) or operating expense (general sales cost)

- Equipment repairs: you can classify these as cost of sales (if the equipment directly produces your product) or operating expense (general maintenance)

Pick one approach for each expense type and stick with it. Inconsistent classification creates unreliable figures and makes it harder to track profitability over time.

Retail business example

Here's how a homeware store owner calculates cost of sales to set a profitable price for handmade pottery cups.

Cost breakdown per cup:

- Supplier cost: £5

- Shipping from supplier: £2

- Staff labour (shelving and sales assistance): £3

Total cost of sales: £10 per cup

To achieve a specific profit margin, you could set a retail price of £15 per cup. This represents a 50% markup on the £10 cost. Note that a 50% markup = 33% margin. This covers the £10 cost of sales and leaves £5 profit per unit.

Cost of sales vs. expenses

Cost of sales covers expenses directly tied to delivering your product or service. Business expenses (or operating expenses) are the costs of running your business that aren't linked to individual sales.

Here's how to tell the difference between these two expense types:

- PR agency fees: classify as a business expense because it promotes your brand but isn't required to complete a sale

- Delivery fees: classify as a cost of sale because without shipping, online orders wouldn't reach customers

Track both figures to make smarter financial decisions. When sales drop, look at reducing business expenses. When profit margins shrink, focus on lowering your cost of sales.

Cost of sales vs. cost of goods sold

Cost of sales and cost of goods sold (COGS) are often used interchangeably, but they have subtle differences defined by International Accounting Standards like IAS 2 Inventories.

Cost of goods sold (COGS): focuses on the direct costs of producing or purchasing physical goods. Manufacturers and product-based businesses typically use this term.

Cost of sales: covers all direct costs of delivering value to customers, including service delivery costs like labour and software. Service businesses often prefer this term.

Use the following guidance to choose the right term for your business:

- Use COGS if you manufacture or sell physical products

- Use cost of sales if you provide services or want to capture distribution costs alongside production costs

In practice, many businesses and accountants use the terms interchangeably. What matters most is that you define your calculation clearly and apply it consistently.

How to reduce your cost of sales

Reducing your cost of sales improves profitability without requiring you to raise prices. Here are six ways to lower your direct costs:

- Negotiate better supplier terms: Ask for volume discounts, extended payment terms, or loyalty pricing from existing suppliers.

- Compare suppliers regularly: Shop around for raw materials and stock. Even small savings per unit add up over time.

- Improve production efficiency: Invest in technology, equipment upgrades, or staff training to produce more with less waste.

- Optimise inventory management: Avoid overstocking (which ties up cash) and understocking (which means missed sales). Inventory software helps you find the right balance.

- Outsource selectively: Contract specialists for specific tasks instead of hiring full-time staff when the workload doesn't justify a permanent role.

- Review direct costs quarterly: Audit your cost of sales regularly to catch creeping expenses before they erode your margins.

Track your cost of sales over time to measure the impact of these changes on your profitability.

Track your cost of sales with Xero

Your costs change constantly. Without a simple way to track them, expenses can spiral before you notice.

Xero gives you a live view of your income and outgoings, so you always know where your money goes. With Xero's job costing features, you can:

- Track costs by project, product, or service

- Monitor profit margins in real time

- Spot rising expenses before they affect your bottom line

Xero's analytics and reporting tools let you dig deeper with cash flow projections, income and expenditure reports, and financial statements that keep you in control.

Get one month free and see how Xero simplifies cost tracking for your business.

FAQs on cost of sales

Here are answers to common questions about calculating and managing your cost of sales.

Is cost of sales an expense or income?

Cost of sales is an expense. It appears on your income statement (profit and loss) and reduces your gross profit. You calculate gross profit by subtracting cost of sales from your revenue.

What is a good cost of sales percentage?

A good cost of sales percentage depends on your industry, as benchmarks vary widely across industries; for example, a software company's might be 15–25% while a restaurant's could be 30–35%. Retailers typically aim for 25–50% of revenue, while service businesses often target 15–30%. Manufacturing businesses may see 40–60%.

Compare your percentage to industry benchmarks and track it over time. A rising percentage signals margin pressure; a falling percentage indicates improved efficiency.

How often should I calculate cost of sales?

Calculate your cost of sales at least monthly to catch rising costs early. Many businesses review it quarterly for strategic decisions and annually for tax reporting.

If your costs fluctuate significantly (due to seasonal demand or volatile supplier prices), consider weekly or fortnightly reviews.

Can cost of sales include employee salaries?

Yes, but only for employees directly involved in producing goods or delivering services. Include wages for production staff, service delivery teams, and direct labour.

Exclude salaries for administrative staff, management, sales teams (unless commission-based), and back-office functions. These are operating expenses, not cost of sales.

What's the difference between cost of sales and operating expenses?

Cost of sales includes direct costs tied to producing or delivering what you sell. Operating expenses cover the costs of running your business regardless of sales volume.

For example, raw materials are a cost of sale (you don't need materials if you make no sales). Office rent is an operating expense (you pay it regardless of your sales volume).

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Start using Xero for free

Access Xero features for 30 days, then decide which plan best suits your business.