Fringe benefits tax: What it is and how it works in Australia

Learn how fringe benefits tax affects costs, payroll and retention, and how to stay compliant while saving time.

Written by Lena Hanna—Trusted CPA Guidance on Accounting and Tax. Read Lena's full bio

Published Wednesday 26 November 2025

Table of contents

Key takeaways

• Register for fringe benefits tax with the ATO as soon as you know you have a liability, even if your benefits are exempt, to avoid audits and manage obligations more effectively throughout the FBT year (1 April to 31 March).

• Calculate FBT by identifying taxable benefits, determining their value using appropriate methods, grossing up the amount (×2.0802 for GST-creditable benefits or ×1.8868 for non-creditable), then applying the 47% FBT rate to determine what you owe.

• Utilise key exemptions to reduce your FBT liability, including the minor benefits exemption for irregular benefits under $300, work-related items exemption for business equipment like laptops, and electric vehicle exemption for zero-emission cars below the luxury tax threshold.

• Maintain detailed records including logbooks, receipts and agreements for all benefits provided, keeping documentation for five years and using official ATO calculators to ensure accurate valuations and compliance.

Do you need to register for fringe benefits tax?

If your business provides fringe benefits to employees, you’ll likely need to register for fringe benefits tax with the Australian Taxation Office (ATO). You must register as soon as you know you have a fringe benefits tax liability.

If your benefits are exempt, you can still register. Registering lets you lodge a nil fringe benefits tax return and helps you avoid audits for previous years.

You can register for fringe benefits tax at any time of the year. Register online, through a registered tax agent, or by phone. Staying registered makes it easier to manage your obligations each fringe benefits tax year, which runs from 1 April to 31 March.

Why is fringe benefits tax important for small businesses?

Staying compliant with fringe benefits tax helps you avoid extra costs and gives you a clear view of employee benefit expenses.

Why it pays to stay compliant with fringe benefits tax

- avoid extra tax bills by understanding how benefits increase employment costs

- meet deadlines to avoid fines for late registration, filing or payment

- know which business expenses, such as team dinners, may trigger fringe benefits tax

Common fringe benefits tax challenges for small businesses

- check what counts as a fringe benefit, as definitions can vary

- use the right valuation method for each benefit type

- remember that the fringe benefits tax year runs from April to March, not the standard financial year

How to calculate and file your fringe benefits tax in Australia

You can calculate your fringe benefits tax in five steps. Keeping accurate records helps you stay compliant and reduces your audit risk.

1. Identify your taxable fringe benefits

Check if your employee benefits fall into these Australian Taxation Office categories to identify taxable fringe benefits:

- provide a vehicle for business and personal use, including parking costs

- pay for staff meals, accommodation, holidays or parties (not client entertainment)

- offer loans to employees at below-market interest rates

- provide rent-free or subsidised accommodation

- reimburse employees' private expenses, such as medical insurance or school fees

- give goods such as electronics, shares or other physical property

See the full list of fringe benefit categories on the Australian Taxation Office website

For example, if you provide an employee with a Toyota Hilux (worth $50,000 plus GST) for work during the week and personal use on weekends, the private use makes it a car fringe benefit and triggers fringe benefits tax.

2. Work out the taxable value of the benefit

The way you calculate the taxable value depends on the type of benefit. Choose the method that best suits your records and gives the most accurate result.

Car fringe benefits - Choose from two valuation methods:

- use the statutory formula method: base value × 20% × (private use days ÷ 365)

- use the operating cost method: actual costs × private use percentage

Read more about the statutory formula method on the Australian Taxation Office website

Loan fringe benefits:

- compare the interest charged with the Australian Taxation Office benchmark rate

Entertainment and expense payments:

- use the actual cost method: full amount spent on employee benefits

- use the 50/50 split method: half of total entertainment costs (entertainment benefits only)

In our example, an employee is provided with a Toyota Hilux valued at $50,000 (+ GST.)

If the vehicle is solely for personal use, the FBT is calculated as:

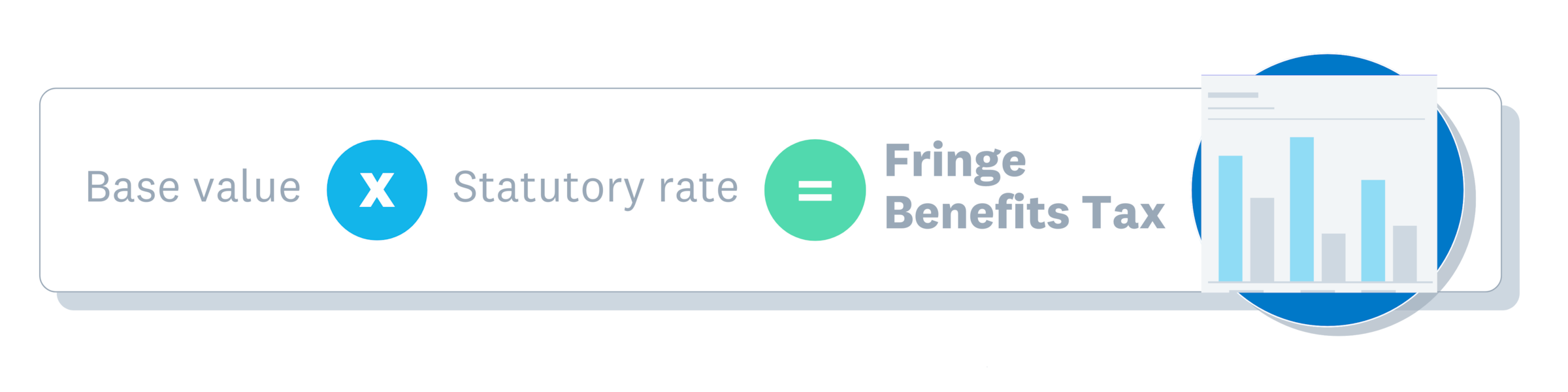

Base value × statutory rate = taxable value

$50,000 × 20% = $10,000 taxable value

But if the car is for business during the week and only available for personal use on weekends – 104 out of 365 days – the calculation reflects that period of availability:

Base value × statutory rate × (days available ÷ 365) = $2,849 taxable value $50,000 × 20% × (104 ÷ 365) = $2,849 taxable value

If you need more help, use the Australian Taxation Office car fringe benefits calculator. You can also view the Australian Taxation Office guide to fringe benefits tax rates and thresholds.

3. 'Gross up' the taxable value to account for income tax

Grossing up converts benefit values into equivalent pre-tax salary amounts. This ensures FBT reflects what an employee would need to earn to buy the same benefit with after-tax dollars.

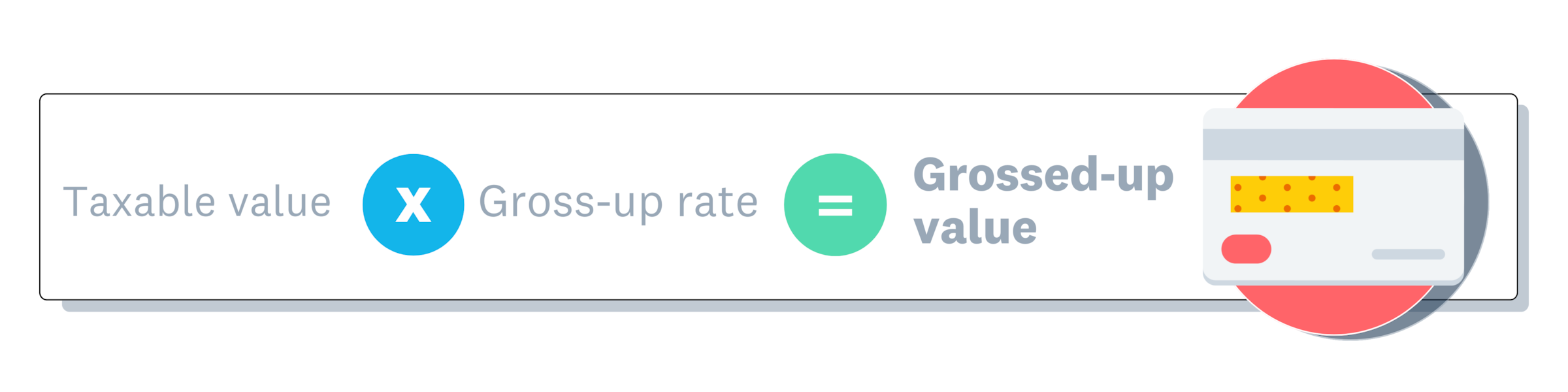

The formula to calculate the grossed-up value is:

Taxable value × gross-up rate = grossed up value

There are two types of gross-up rates. The one you use depends on whether your business can claim a GST credit for the benefit:

- Type 1 gross-up rate (× 2.0802) – use this when your business can claim a GST credit (on company cars, entertainment expenses, and so on)

- Type 2 gross-up rate (× 1.8868) – use this when you can't claim a GST credit (such as for employee loans)

The taxable value of the Toyota Hilux provided for personal use was $10,000. Because cars include GST and the employer can claim a credit, the Type 1 gross-up rate applies:

$10,000 × 2.0802 = $20,802 grossed up value

4. Calculate the payable FBT

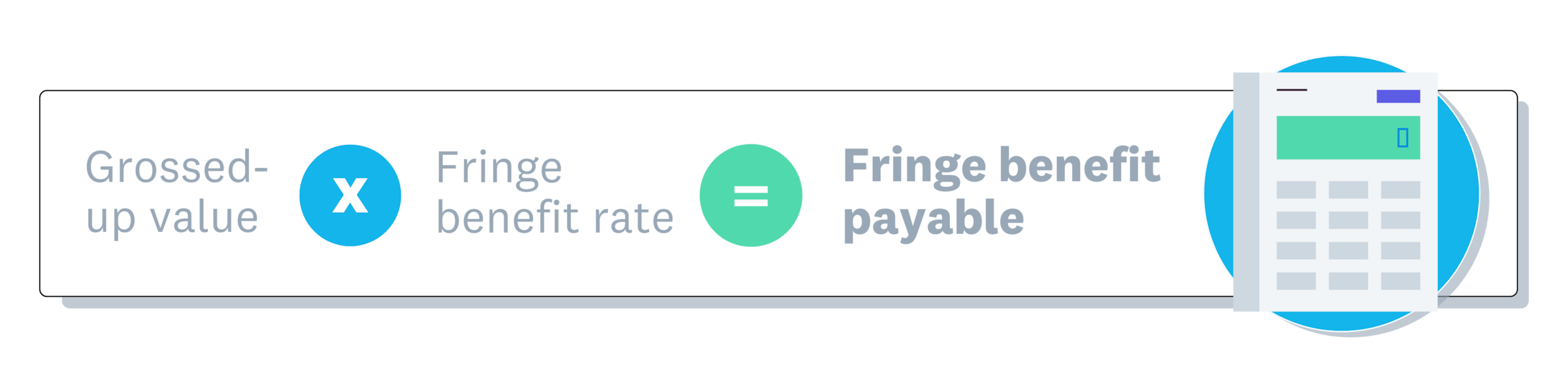

Now apply the fringe benefits tax rate to calculate the amount you owe. For the 2024–25 financial year, the rate is 47%. Check the current fringe benefits tax rates on the Australian Taxation Office website.

The formula is:

Grossed-up value × FBT rate = FBT payable

In our earlier example, the grossed-up value of the Toyota Hilux car benefit was $20,802. Apply the FBT rate:

$20,802 × 47% = $9,777

The employer must pay $9,777 in FBT for providing the vehicle to the employee for personal use.

5. Report your FBT and pay it to the ATO

If your business provides taxable fringe benefits, you must lodge an FBT return with the ATO.

- The fringe benefits tax year runs from 1 April to 31 March, which is different from the financial year.

- Your fringe benefits tax return is due by 21 May each year. You can get an extension if you lodge through a registered tax agent.

If an employee receives fringe benefits with a total taxable value of more than $2,000 in a fringe benefits tax year, you must include a reportable fringe benefits amount (RFBA) on their income statement or payment summary. Read more about reportable fringe benefits amounts on the Australian Taxation Office website.

FBT exemptions for small businesses

You can reduce your fringe benefits tax by using exemptions and still offer valuable employee benefits. Three key exemptions can lower your bill:

- claim the minor benefits exemption for infrequent, irregular benefits with a notional taxable value of less than $300

- use the work-related items exemption for items mainly used for work, such as laptops, phones, safety equipment or software

- apply the electric vehicle exemption for zero-emission vehicles below the luxury car tax threshold, which can save you up to $9,000 a year on a $50,000 model

Read more about fringe benefits tax exemptions on the Australian Taxation Office website

Ways to comply with ATO FBT rules

The Australian Taxation Office uses audits and data-matching to find fringe benefits tax errors. Following best practices helps you avoid penalties and audit triggers.

Essential compliance practices:

- keep detailed records, such as logbooks, receipts and agreements, for all benefits you provide; you must keep these for five years from the date of your fringe benefits tax return

- use official calculators, such as Australian Taxation Office tools, to simplify valuations and reduce errors

- meet filing deadlines by lodging by 21 May or using a registered tax agent for extensions

- stay up to date, as fringe benefits tax rates and rules change regularly; check Australian Taxation Office updates often

What triggers ATO attention:

- report consistently each year

- avoid large changes in benefit values without explanation

- keep complete documentation for all benefits

Speak with a tax professional if you need help meeting fringe benefits tax rules. You can find one in the Xero advisor directory.

Simplify fringe benefits tax and save time with Xero

You can get your fringe benefits tax right the first time.

Xero accounting software helps you streamline your fringe benefits tax calculations and reporting by tracking payroll, expenses and employee benefits in one place – no spreadsheets required. Stay compliant and find ways to manage your costs more effectively.

See how Xero accounting software simplifies payroll and fringe benefits tax reporting

Frequently asked questions about fringe benefits tax

Here are some common questions small businesses have about FBT.

What's the difference between FBT and income tax?

Fringe benefits tax (FBT) is paid by employers on non-cash benefits provided to employees, while income tax is paid by employees on their wages or salary. They are two separate taxes.

Do I have to pay FBT on a staff Christmas party?

It depends. A Christmas party is considered entertainment, but it may be exempt from FBT if it qualifies as a minor benefit. However, the exemption may not apply to meal entertainment provisions if you use the 50/50 split method for valuation. This means the cost per employee is less than $300 and it's an infrequent event. If the cost is $300 or more, FBT will likely apply.

How can I reduce my FBT liability?

You can reduce your FBT by providing benefits that are exempt, such as work-related items like laptops. You can also ask employees to contribute towards the cost of a benefit, which reduces its taxable value. Speaking with a tax professional can help you find the best strategies for your business.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Start using Xero for free

Access Xero features for 30 days, then decide which plan best suits your business.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Start using Xero for free

Access Xero features for 30 days, then decide which plan best suits your business.