What is cash flow?

Learn what cash flow is, why it matters and how to manage it in your small business.

Published Thursday 9 July 2026

Table of contents

Key takeaways

- Cash flow is the movement of money in and out of your business over a set period, and it determines whether you can pay your bills on time.

- A profitable business can still run out of cash if the timing of payments and receipts doesn't align.

- There are 3 types of cash flow: operating, investing and financing, and each tells you something different about your financial health.

- Monitoring your cash flow regularly with forecasts and cash flow statements helps you spot problems early and plan ahead.

What is cash flow?

Cash flow is the movement of money into and out of your business over a specific period. It covers every dollar that comes in from sales, loans or investments, and every dollar that goes out through expenses, wages and supplier payments. Understanding cash flow management is essential for keeping your business financially healthy.

When more money flows in than out, you have positive cash flow. That means you've got enough to cover your costs and potentially invest back into the business. When more money flows out than in, you have negative cash flow, which can make it difficult to meet your obligations.

Cash flow is different from profit. Profit is an accounting measure that includes non-cash items like depreciation, while cash flow tracks the actual money available to you right now. A business can be profitable on paper but still struggle if cash isn't arriving when it's needed.

Why cash flow matters for small businesses

Cash flow is one of the most important indicators of your business's health. Without enough cash on hand, you can't pay suppliers, cover wages or take advantage of growth opportunities, even if your business is technically profitable.

For Australian small businesses, the stakes are especially clear. According to Xero Small Business Insights, small businesses across Australia experienced 6.7% sales growth and 3.4% jobs growth. That kind of growth requires cash to fund new inventory, hire staff and expand operations.

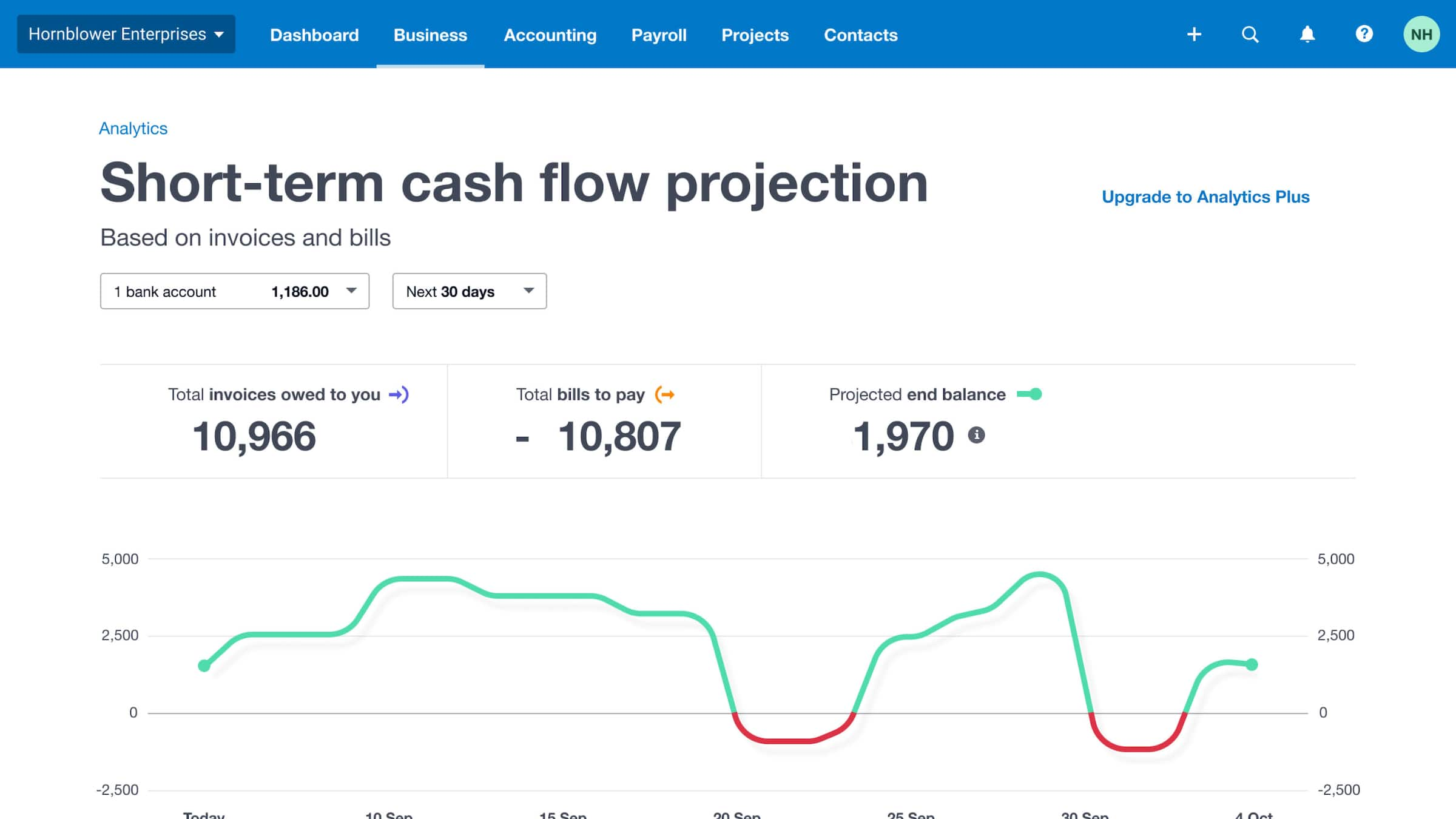

Small businesses can get a picture of future cash flow by accounting for upcoming bills and payments (example from Xero dashboard).

Strong cash flow also gives you a buffer for the unexpected. It helps you weather slow months, manage seasonal fluctuations and avoid relying on expensive short-term borrowing. When you know exactly where your cash stands, you can make confident decisions about when to invest, when to hold back and when to chase up overdue invoices.

What affects cash flow

Several factors influence how cash moves through your business. Understanding these drivers helps you anticipate shortfalls before they become a problem.

The 3 main areas that affect cash flow are:

- Operations: the day-to-day money coming in from sales and going out for expenses like rent, wages, stock and utilities

- Investments: cash spent on or received from buying and selling assets like equipment, vehicles or property

- Financing: money raised through loans, investor contributions or owner drawings, and repayments on those obligations

Payment timing is a major factor for Australian small businesses. Data from Xero Small Business Insights shows that small businesses wait an average of 23.9 days to be paid, and payments arrive 6.6 days late on average. Those delays can create serious cash flow gaps, even when your sales pipeline looks healthy.

Types of cash flow

Cash flow is typically broken down into 3 categories. Each one tells you something different about where your money is coming from and how it's being used.

Cash flow from operations (CFO)

Cash flow from operations (CFO) covers the money generated by your core business activities. It includes cash received from customers, minus the cash paid for everyday expenses like wages, rent, stock and utilities. CFO is the most important indicator of whether your business can sustain itself from its regular operations.

Cash flow from investing (CFI)

Cash flow from investing (CFI) relates to the purchase or sale of long-term assets. If you buy new equipment or a vehicle, that's a cash outflow. If you sell an asset, it's a cash inflow. A negative CFI often means you're investing in growth, which isn't necessarily a bad sign.

Cash flow from financing (CFF)

Cash flow from financing (CFF) tracks money moving between your business and its funders. This includes taking out loans, repaying debt, receiving capital from investors or making owner drawings. CFF shows how your business is being funded beyond its day-to-day operations.

How to calculate cash flow

The simplest way to calculate your cash flow is with the net cash flow formula. It gives you a clear picture of whether your business ended a period with more or less cash than it started with.

Net cash flow = total cash inflows – total cash outflows

For example, if your business received $50,000 in cash during a month and paid out $42,000, your net cash flow for that month is $8,000. A positive number means you brought in more than you spent. A negative number means you spent more than you received.

You can also calculate net cash flow by adding the 3 types together: CFO + CFI + CFF = net cash flow. This gives you a more detailed view of where the cash came from and where it went.

How to measure cash flow

Measuring cash flow regularly is one of the best ways to stay ahead of potential problems. Two key tools help you do this: cash flow forecasts and cash flow statements.

Cash flow forecasts

A cash flow forecast predicts how much cash you expect to receive and spend over a future period, usually weekly, monthly or quarterly. It helps you spot upcoming shortfalls so you can act before they become urgent.

To build a forecast, list your expected cash inflows (customer payments, loan proceeds, other income) and outflows (rent, wages, supplier payments, tax obligations like Business Activity Statements (BAS)) for each period. The difference tells you whether you'll have a surplus or a gap. Xero's cash flow forecasting tools can automate much of this by pulling data directly from your accounts.

Cash flow statements

A cash flow statement is a financial report that shows how much cash actually moved in and out of your business during a past period. It breaks the movement down into the 3 categories: operating, investing and financing activities.

Unlike a forecast, a cash flow statement looks backwards. It helps you understand what happened and why your cash position changed. Reviewing your cash flow statement alongside your profit and loss report gives you a fuller picture of your financial performance.

Cash flow vs profit

Cash flow and profit are related but they measure different things. Profit is the amount left after you subtract all expenses from your revenue, including non-cash items like depreciation and amortisation. Cash flow is the actual money moving in and out of your business.

It's possible to be profitable and still have negative cash flow. For example, if you've made a large sale but the customer hasn't paid yet, that revenue appears on your profit and loss report. But the cash isn't in your account, so you might not be able to cover this week's bills.

The reverse can also happen. A business might show a loss on paper while maintaining positive cash flow, perhaps because it received a large upfront payment or delayed certain expenses. That's why tracking both metrics gives you a more complete view of your financial position.

How cash flow differs from free cash flow, working capital and liquidity

Cash flow is often discussed alongside several related terms. Here's how they differ.

- Free cash flow: the cash left after your business has covered its operating expenses and capital expenditures. It shows how much cash is genuinely available for growth, debt repayment or distributions to owners.

- Working capital: the difference between your current assets (cash, accounts receivable, stock) and your current liabilities (accounts payable, short-term debt). It measures your ability to meet short-term obligations.

- Liquidity: how quickly you can convert assets into cash without losing significant value. A business with high liquidity can access cash fast when it's needed.

All 3 concepts relate to your financial health, but they each focus on a different angle. Cash flow tells you what's actually moving. Free cash flow tells you what's left over. Working capital and liquidity tell you how well positioned you are to handle short-term demands.

A quick note on the meaning of 'cash'

When accountants talk about cash flow, 'cash' doesn't just mean physical notes and coins. It includes cash equivalents: short-term, highly liquid assets that can be converted into a known amount of cash with minimal risk.

Examples of cash equivalents include bank deposits, term deposits with maturities of 3 months or less, and money market funds. Essentially, if you can access it quickly and its value is stable, it counts as cash for reporting purposes.

How to improve your cash flow

Improving cash flow doesn't always require earning more. Often, it's about tightening the timing between when money comes in and when it goes out.

Here are practical steps you can take to strengthen your cash flow.

- Invoice promptly: send invoices as soon as work is completed or goods are delivered. Setting clear invoice payment terms and sending invoices quickly means you can expect payment sooner.

- Offer online payment options: making it easy for customers to pay speeds up collections. Xero customers who use online invoice payments get paid up to twice as fast as those who don't.

- Follow up on overdue invoices: set up automated reminders to chase late payments before they become a bigger problem. Xero's invoice reminders can handle this for you.

- Negotiate payment terms with suppliers: ask for longer payment terms where possible, so you have more time to collect from your customers before your own bills are due.

- Monitor your cash flow regularly: review your cash position weekly or fortnightly, not just at the end of the month. Regular checks help you catch issues early.

- Build a cash reserve: set aside a portion of your income as a buffer for quiet periods or unexpected expenses.

- Use accounting software to track everything in real time: cloud accounting tools like Xero connect to your bank, automate reconciliation and give you a clear view of your cash position at any time.

Manage your cash flow with Xero

Staying on top of your cash flow is easier when your financial data is in one place. Xero connects to your bank, automates reconciliation and gives you real-time visibility into the money coming in and going out of your business.

With Xero, you can send invoices with online payment options, set up automated payment reminders and track your cash flow with forecasting tools. You'll spend less time on admin and more time making confident decisions about your business. Get one month free.

FAQs on cash flow

Here are answers to frequently asked questions about cash flow.

What is the difference between cash flow and profit?

Profit includes non-cash items like depreciation and accounts for revenue when it's earned, not when cash is received. Cash flow tracks the actual money entering and leaving your bank account during a specific period.

How do you calculate cash flow?

Use the net cash flow formula: total cash inflows minus total cash outflows. You can also add up cash flow from operations, investing and financing activities to get a more detailed breakdown.

What is free cash flow?

Free cash flow is the cash remaining after your business has paid its operating costs and capital expenditures. It represents the money genuinely available for growth, debt repayment or owner distributions.

Why is cash flow important for small businesses?

Cash flow determines whether you can pay suppliers, staff and other obligations on time. Without sufficient cash, even a profitable business can face serious difficulties meeting its day-to-day commitments.

How can you improve cash flow in your business?

Invoice as soon as work is completed, offer online payment options and follow up on overdue payments promptly. Regularly reviewing your cash position and negotiating favourable supplier terms also helps close timing gaps.

Handy resources

Advisor directory

You can search for experts in our advisor directory

Cash flow forecast template

Download our free template to help predict cash flow for your business

Business analytics with Xero

See future cash flow, check financial health and track metrics

Disclaimer

This glossary is for small business owners. The definitions are written with their requirements in mind. More detailed definitions can be found in accounting textbooks or from an accounting professional. Xero does not provide accounting, tax, business or legal advice.